,

634 tweets,

396 min read

Read on Twitter

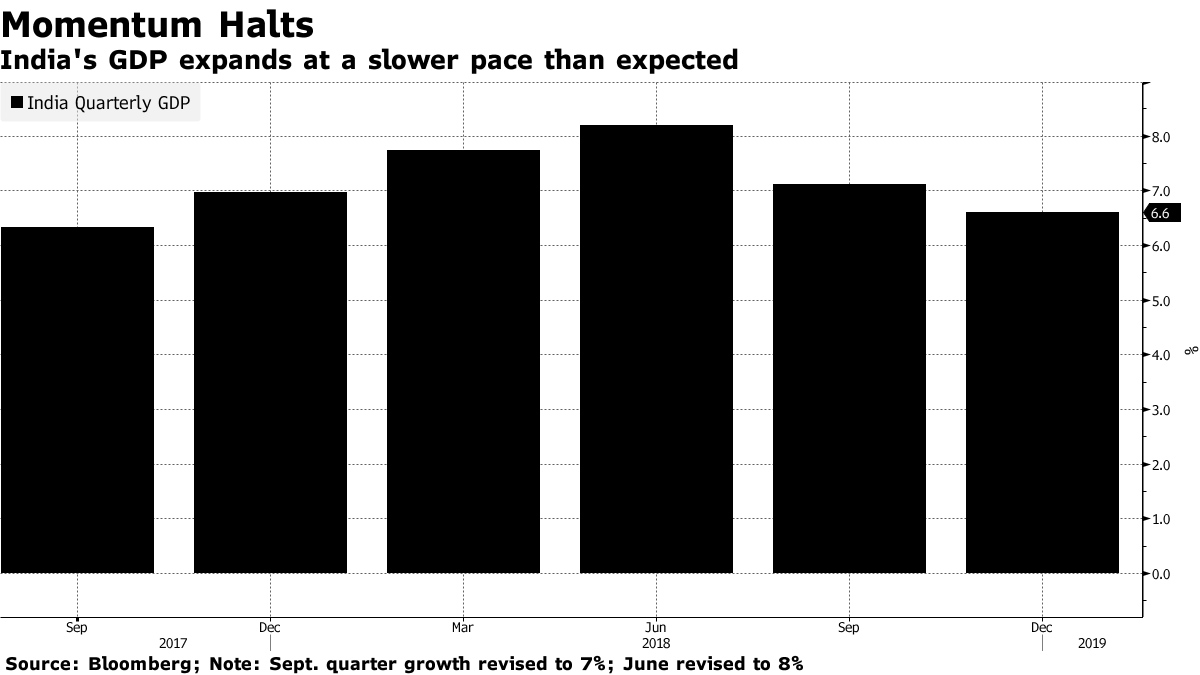

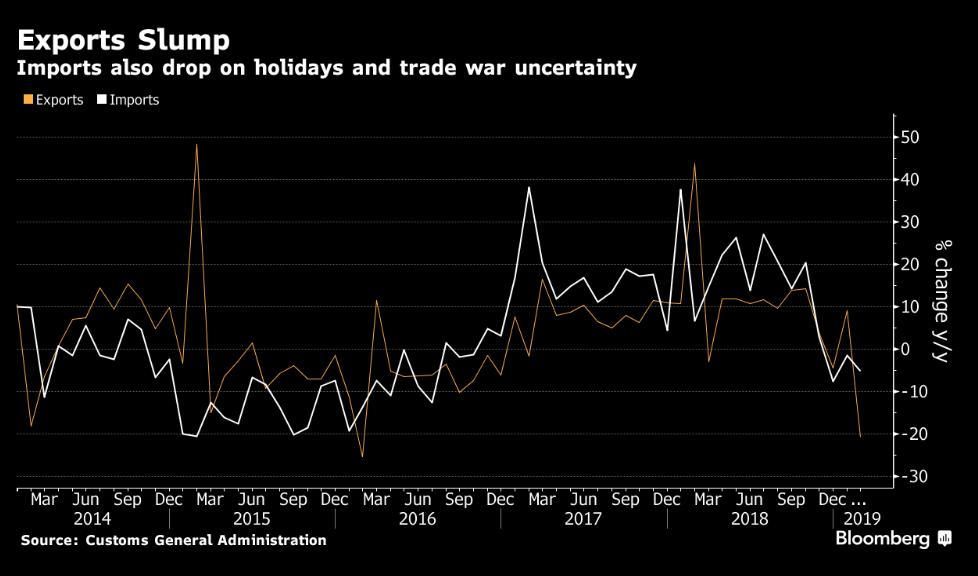

🇨🇳 #CHINA Q3 GDP Y/Y: 6.5% V 6.6%E (slowest growth since Q1 2009)

*NBS spokesman Mao Shengyong said that the international situation was bringing “downward pressure” on China.

*Link: bloom.bg/2RVX1ZA

*NBS spokesman Mao Shengyong said that the international situation was bringing “downward pressure” on China.

*Link: bloom.bg/2RVX1ZA

🇫🇷 🇪🇺 🇨🇳 French tire maker Michelin warned of declining sales in Europe and #China in the second half of the year, dragging down shares of its competitors in the U.S. and Europe - Bloomberg

*Statement: bit.ly/2EujhqH

*Statement: bit.ly/2EujhqH

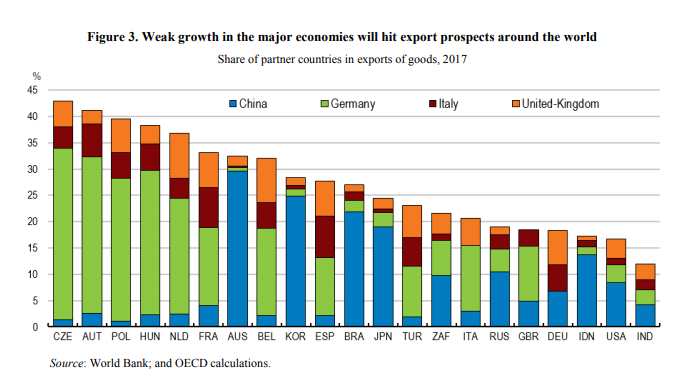

🇺🇸🇨🇳🇪🇺 In a volley of filings, the EU, #China and the U.S. this week escalated disputes over new U.S. metals tariffs, the European response to those levies, and Chinese intellectual property practices - Bloomberg

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

Most of economists still remain too much optimistic:

*The outlook for global growth in 2019 has dimmed for the 1st time, according to Reuters polls of economists who said the U.S.-#China #tradewar and tightening fin. conditions would trigger the next ⬇

reuters.com/article/us-glo…

*The outlook for global growth in 2019 has dimmed for the 1st time, according to Reuters polls of economists who said the U.S.-#China #tradewar and tightening fin. conditions would trigger the next ⬇

reuters.com/article/us-glo…

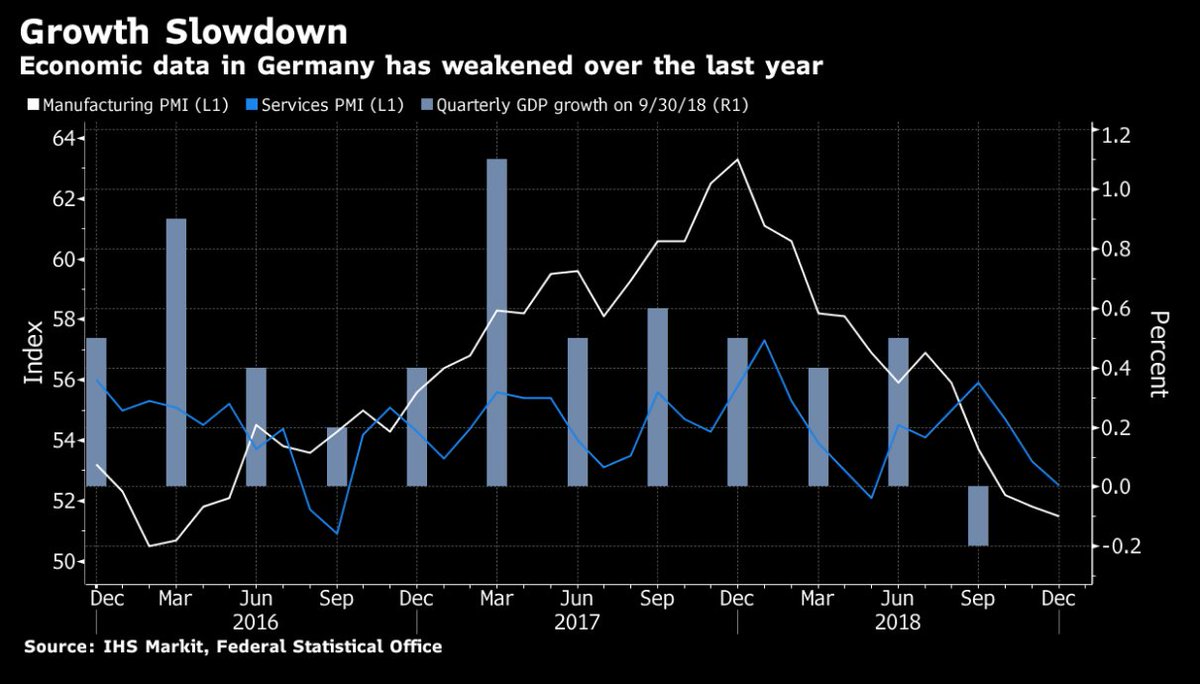

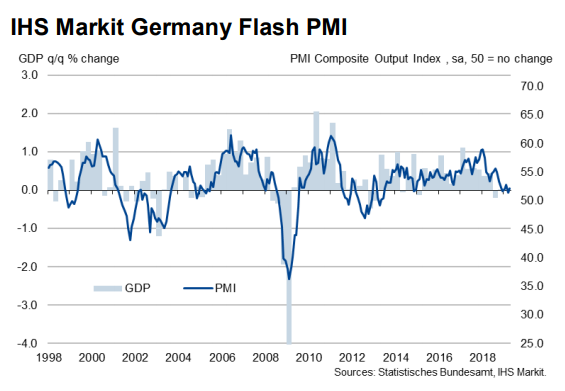

🇩🇪 #Germany | The Bundesbank said Monday that growth “may have come to a temporary halt,” which would be the first quarter without expansion in more than three years.

*Link: bundesbank.de/en/tasks/topic…

*Link: bundesbank.de/en/tasks/topic…

🇨🇳 Over the last few days, #China announced a lot of measures to support domestic activity which suggests that latest 🇺🇸 tariffs ($200b on Sept. 24) had significant impact.

See tweetstorm:

See tweetstorm:

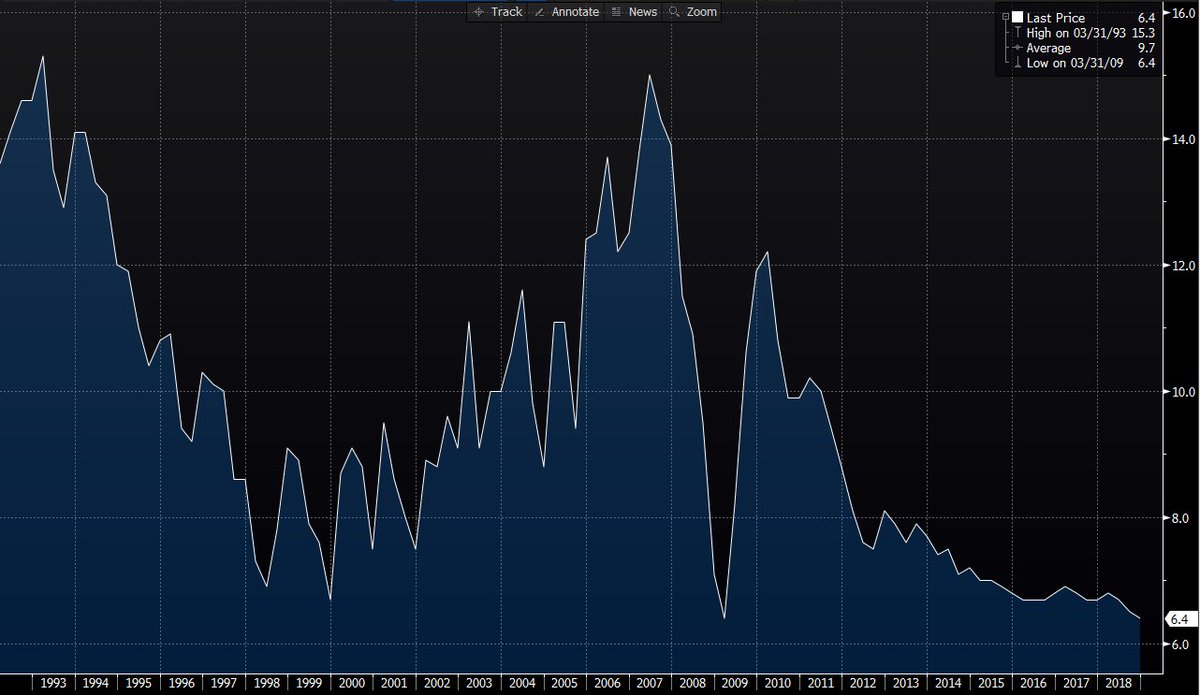

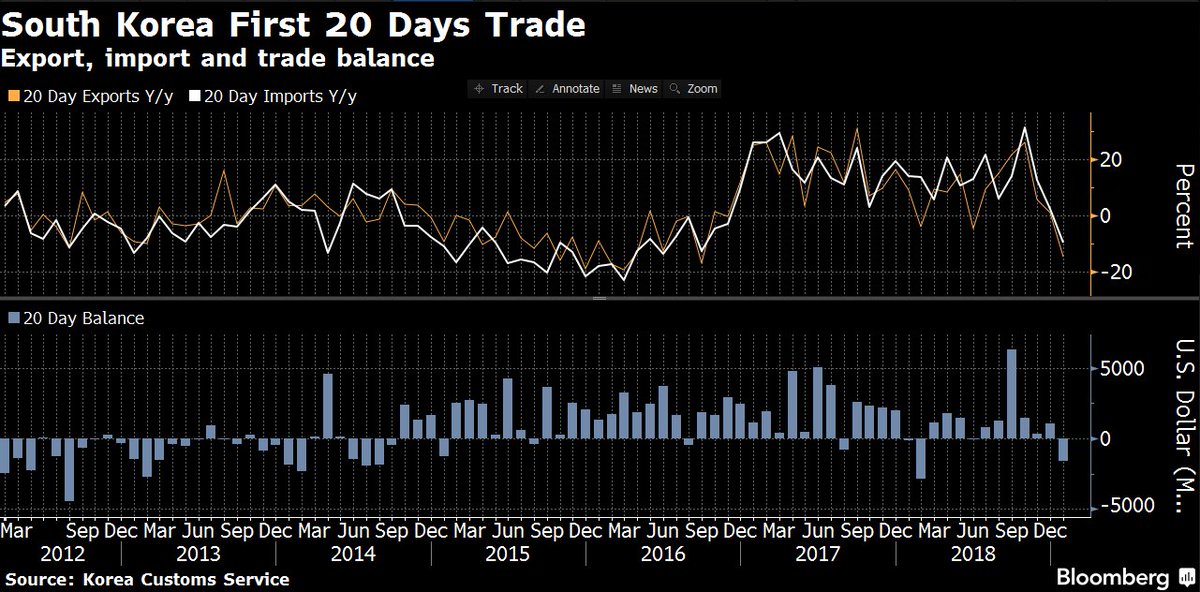

🇰🇷 #SouthKorea's #KOSPI index, a proxy for world trade growth, closed at the lowest level since March 2017.

🇬🇧 #UK OCT CBI INDUSTRIAL TRENDS TOTAL ORDERS: -6 V +2E

#Manufacturing new orders ⬇ at the fastest pace in three years in the quarter to October, reflecting ⬇ in both domestic and export orders.

cbi.org.uk/news/manufactu…

#Manufacturing new orders ⬇ at the fastest pace in three years in the quarter to October, reflecting ⬇ in both domestic and export orders.

cbi.org.uk/news/manufactu…

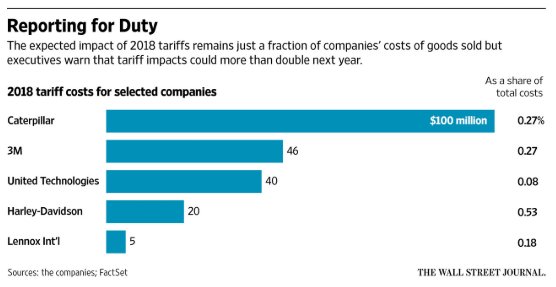

🇺🇸 🇨🇳 U.S. Manufacturers See Signs of New Risks - WSJ

*Caterpillar’s tariff costs and 3M’s slower growth in #China threaten their outlooks

*Link: on.wsj.com/2D2hzLI

*Caterpillar’s tariff costs and 3M’s slower growth in #China threaten their outlooks

*Link: on.wsj.com/2D2hzLI

🇺🇸 🇨🇳 Prospects for #Trump-Xi Deal Fade Even With #G20 Meeting Confirmed - Bloomberg

*Best hope, analysts say, is for pause on next wave of #tariffs

*Link: bloom.bg/2OJevud

*Best hope, analysts say, is for pause on next wave of #tariffs

*Link: bloom.bg/2OJevud

🇺🇸 🇨🇳 Rising costs at US manufacturers unnerve investors - FT

ft.com/content/001c05…

ft.com/content/001c05…

🇨🇳 #China’s industrial sector faces downward pressure, but still operating at a reasonable level - People’s Daily

*Link (Chinese): bit.ly/2D4JhYc

*Link (Chinese): bit.ly/2D4JhYc

🇨🇳 #China deputy head of the Ministry of Industry and Information Technology Xin Guobin told reporters that the period of fast auto sales and production expansion may be over, and slow growth is likely to be the new normal - Xinhua

xinhuanet.com/english/2018-1…

xinhuanet.com/english/2018-1…

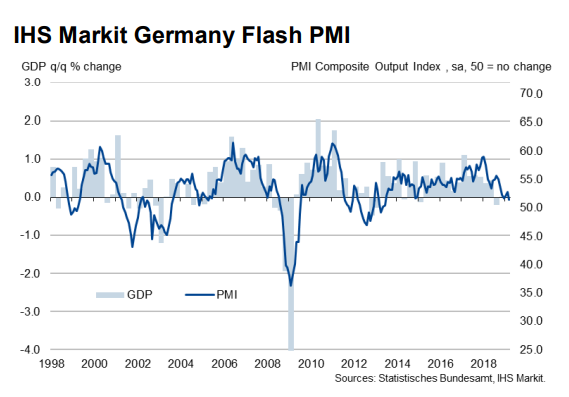

🇩🇪 #GERMANY OCT PRELIMINARY #MANUFACTURING PMI: 52.3 V 53.4E (29-month low)

*Services PMI: 53.6 v 55.5e 63rd (5-month low)

*Composite PMI: 52.7 v 54.8e (41-month low)

*Link: bit.ly/2Pf6JrH

*Services PMI: 53.6 v 55.5e 63rd (5-month low)

*Composite PMI: 52.7 v 54.8e (41-month low)

*Link: bit.ly/2Pf6JrH

🇩🇪 🇪🇺 Following Bundesbank warning on Monday, German figures suggest that economic momentum kept slowing in 4Q. It reinforces my view that the consensus is still too optimistic about:

*Eurozone 2018 and 2019 GDP

*Global trade growth in 2018 and 2019

*Eurozone 2018 and 2019 GDP

*Global trade growth in 2018 and 2019

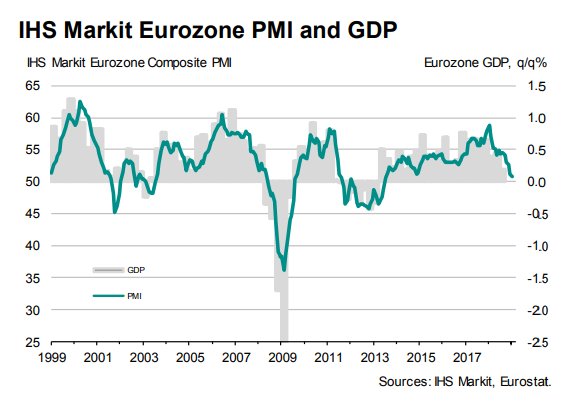

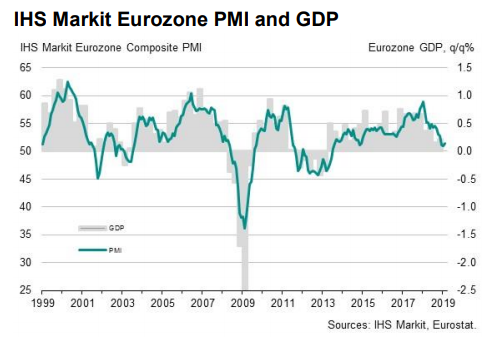

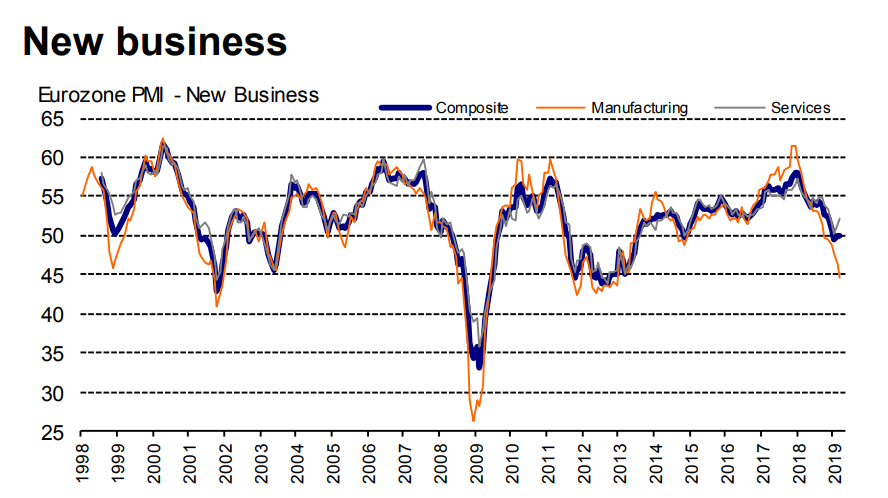

🇪🇺 EUROZONE OCT PRELIMINARY #MANUFACTURING PMI: 52.1 V 53.0E (26-month low)

*New export orders for goods decreased for the first time since June 2013 ❗

*Services PMI: 53.3 v 54.5e (24-month low)

*Composite PMI: 52.7 v 53.9e (25-month low)

*Link: bit.ly/2Apmzrm

*New export orders for goods decreased for the first time since June 2013 ❗

*Services PMI: 53.3 v 54.5e (24-month low)

*Composite PMI: 52.7 v 53.9e (25-month low)

*Link: bit.ly/2Apmzrm

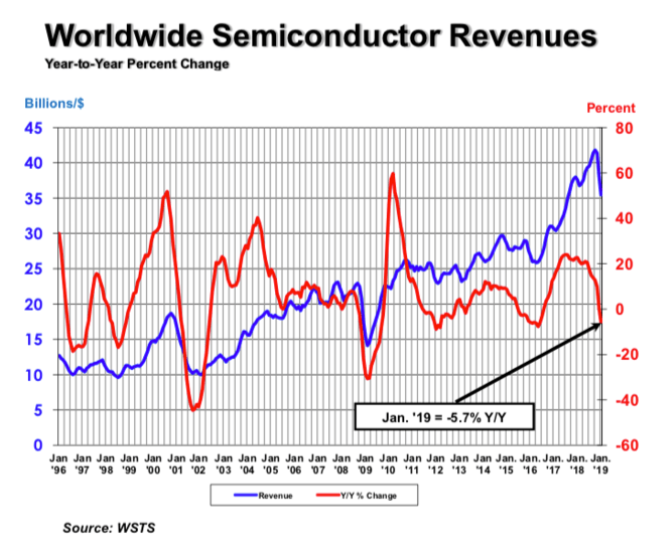

🇺🇸 AMD Follows TI With Dour Sales Forecast, Adding to Chip Woes - Bloomberg

*Revenue from graphic chips disappoints as resellers cut orders

*Link: bloom.bg/2AqIVZo

*Revenue from graphic chips disappoints as resellers cut orders

*Link: bloom.bg/2AqIVZo

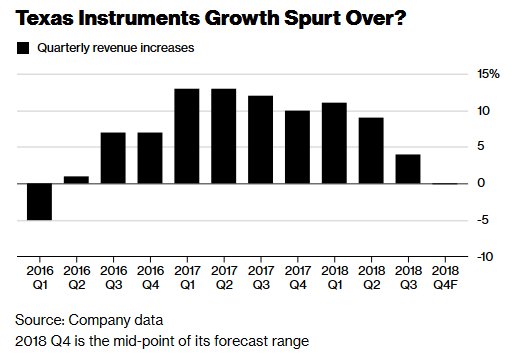

🇺🇸 Texas Instruments Inc., whose chips are in most electronic devices, gave investors the first solid piece of evidence that a multiyear technology spending binge may be ending - Bloomberg

*Link: bloom.bg/2O2WamV

*Link: bloom.bg/2O2WamV

🇺🇸 🇨🇳 #Tradewar | "Tariff (s)" were mentioned 51 times throughout the #Fed Beige in October (up from 41 in September).

wsj.com/articles/fed-r…

wsj.com/articles/fed-r…

🇰🇷 #SouthKorea's GDP Misses Forecasts, Raising Hurdle to Rate Hike - Bloomberg

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

🇪🇺 #ECB'S DRAGHI SAYS INCOMING DATA HAS BEEN WEAKER THAN EXPECTED - BBG

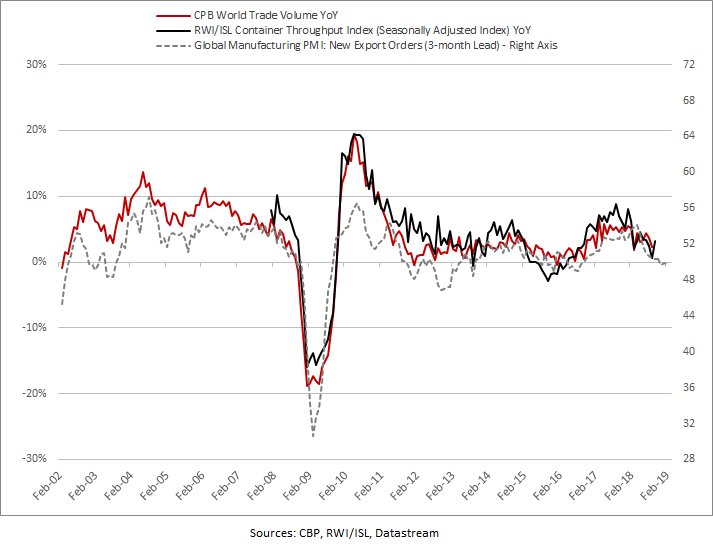

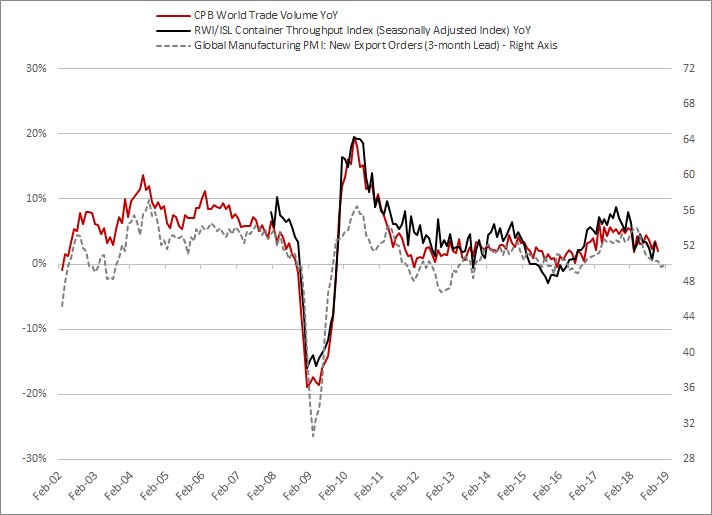

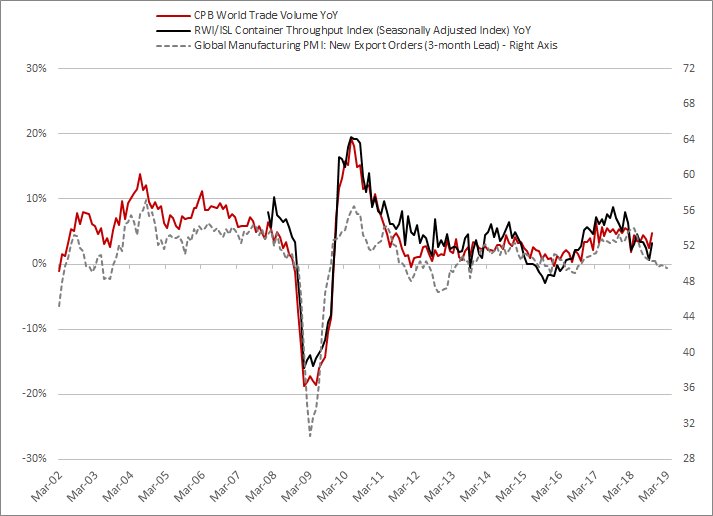

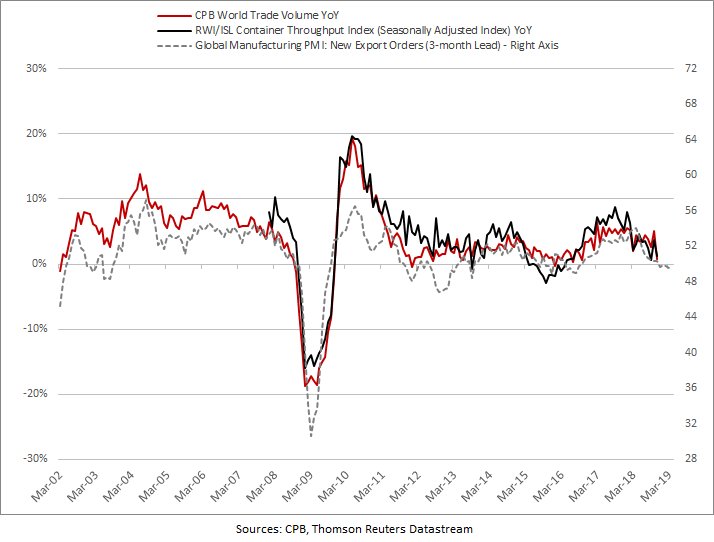

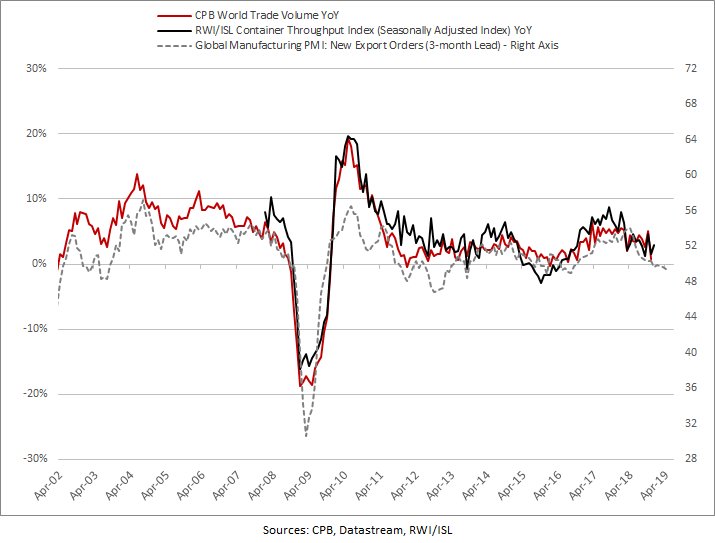

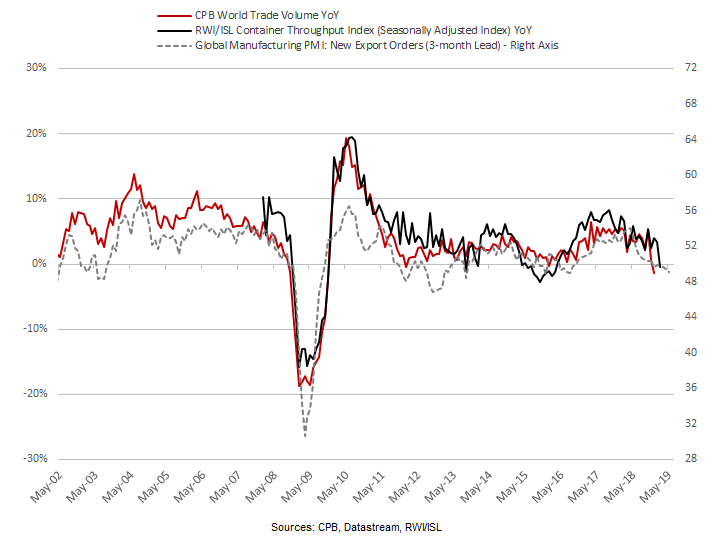

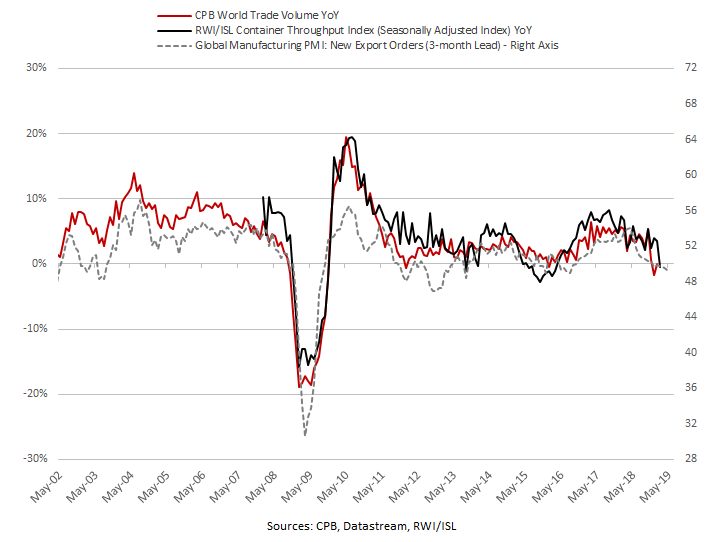

My proxies confirm that global trade growth will keep slowing in the coming months with RWI/ISL container index rising 1.5% YoY in Sept. (slowest pace since July 2016)

*It reinforces my view that the consensus is still too much optimistic for 2018 and 2019.

*It reinforces my view that the consensus is still too much optimistic for 2018 and 2019.

Other cyclical indicators also point to a slowdown (and even a contraction).

🇰🇷 Financial indicators are not in better shape with #SouthKorea's #KOSPI index, a proxy for world trade growth, closing at the lowest level since Jan. 2017.

🇺🇸 On Wednesday, the Standard and Poor's 500 Containers & Packaging Index reached its lowest level since July 2016.

🇺🇸 🇨🇳 Many U.S. firms in #China eyeing relocation as #tradewar bites: survey - Reuters

reuters.com/article/us-usa…

reuters.com/article/us-usa…

🇨🇳 Economists Cut #China GDP Estimates as #TradeWar Trumps Stimulus - Bloomberg

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

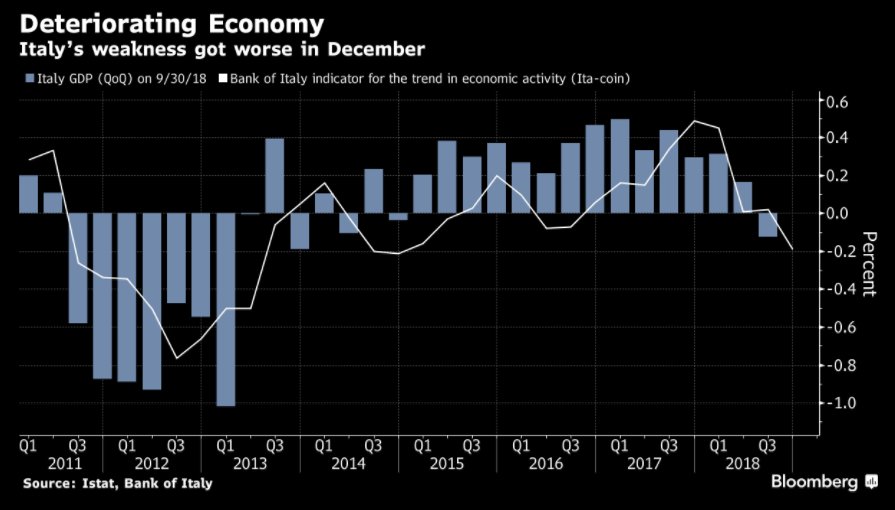

🇪🇺 In line with French figures, Italian GDP came below expectations, confirming my view that the consensus and the ECB remain too optimistic about 2018 and 2019 GDP (see previous tweets).

🇮🇹 #ITALY Q3 PRELIMINARY GDP Q/Q: 0.0% V 0.2%E; Y/Y: 0.8% V 1.0%E

🇮🇹 #ITALY Q3 PRELIMINARY GDP Q/Q: 0.0% V 0.2%E; Y/Y: 0.8% V 1.0%E

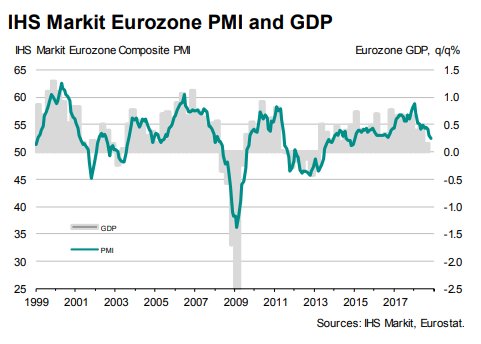

🇪🇺 EUROZONE Q3 ADVANCE GDP Q/Q: 0.2% V 0.4%E; Y/Y: 1.7% V 1.8%E

*As expected, most of economists should revise ⬇ their forecasts for 2018 and 2019 GDP in the coming days/weeks.

*ECB will do the same in Dec.

*As expected, most of economists should revise ⬇ their forecasts for 2018 and 2019 GDP in the coming days/weeks.

*ECB will do the same in Dec.

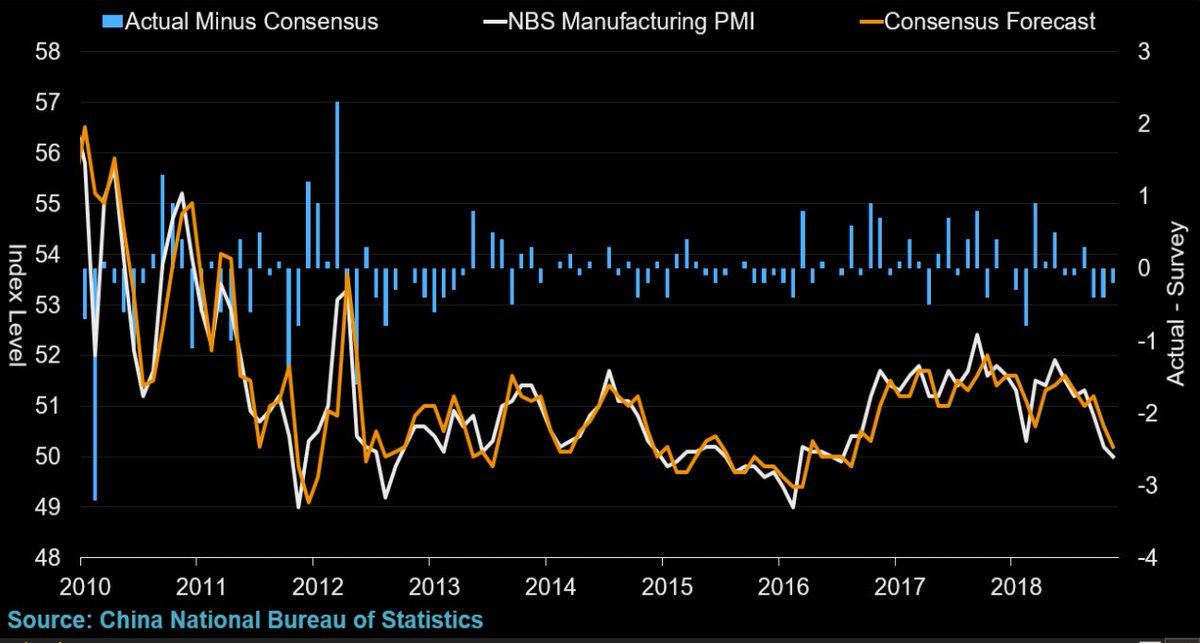

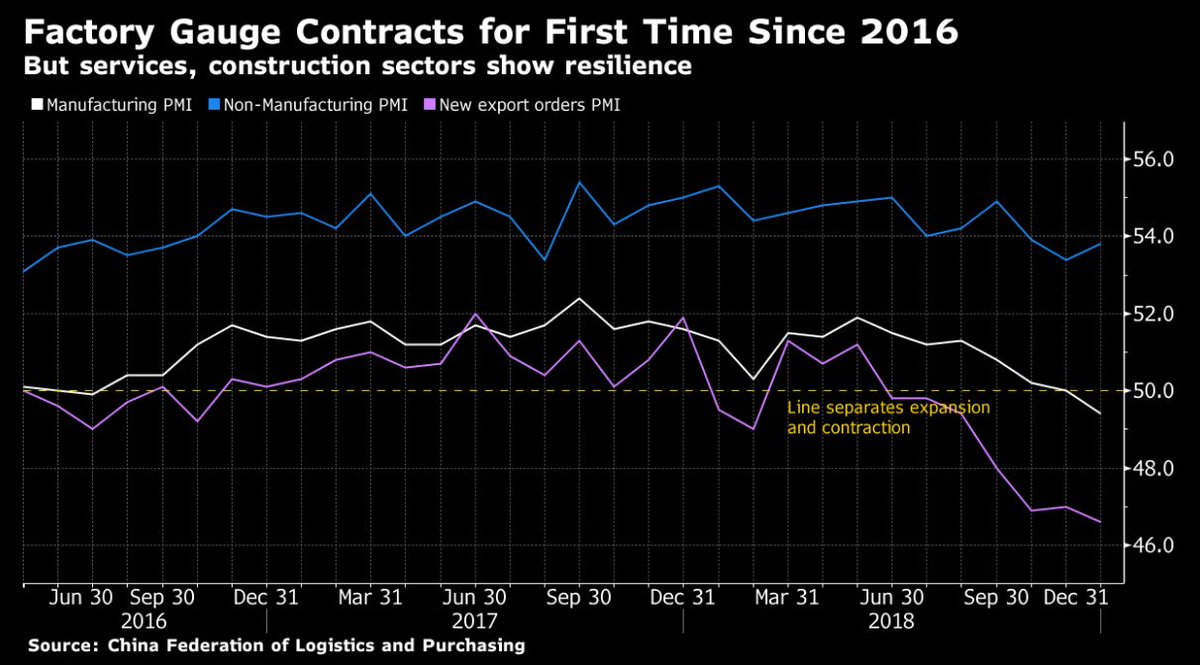

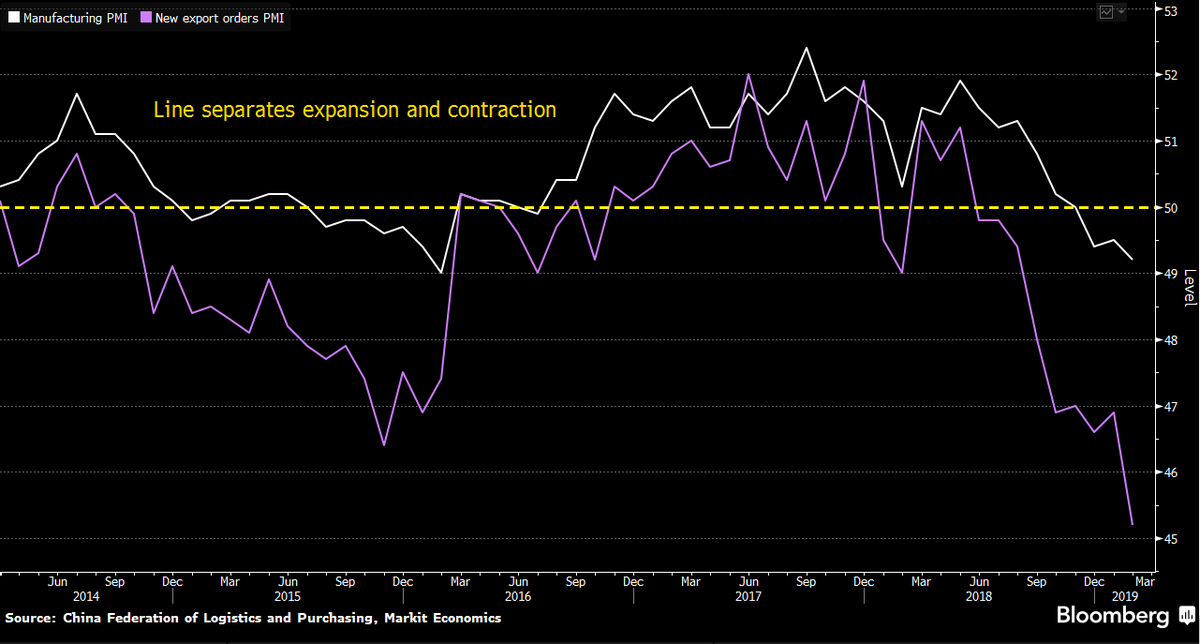

🇨🇳 #CHINA OCT OFFICIAL #MANUFACTURING PMI: 50.2 V 50.6E (lowest since July 2016)

*Non-Manufacturing PMI: 53.9 v 54.6e (lowest since August 2017)

*Composite PMI: 53.1 v 54.1 prior (lowest since February 2018)

*NBS: PMIs affected by long holiday and external environment

*Non-Manufacturing PMI: 53.9 v 54.6e (lowest since August 2017)

*Composite PMI: 53.1 v 54.1 prior (lowest since February 2018)

*NBS: PMIs affected by long holiday and external environment

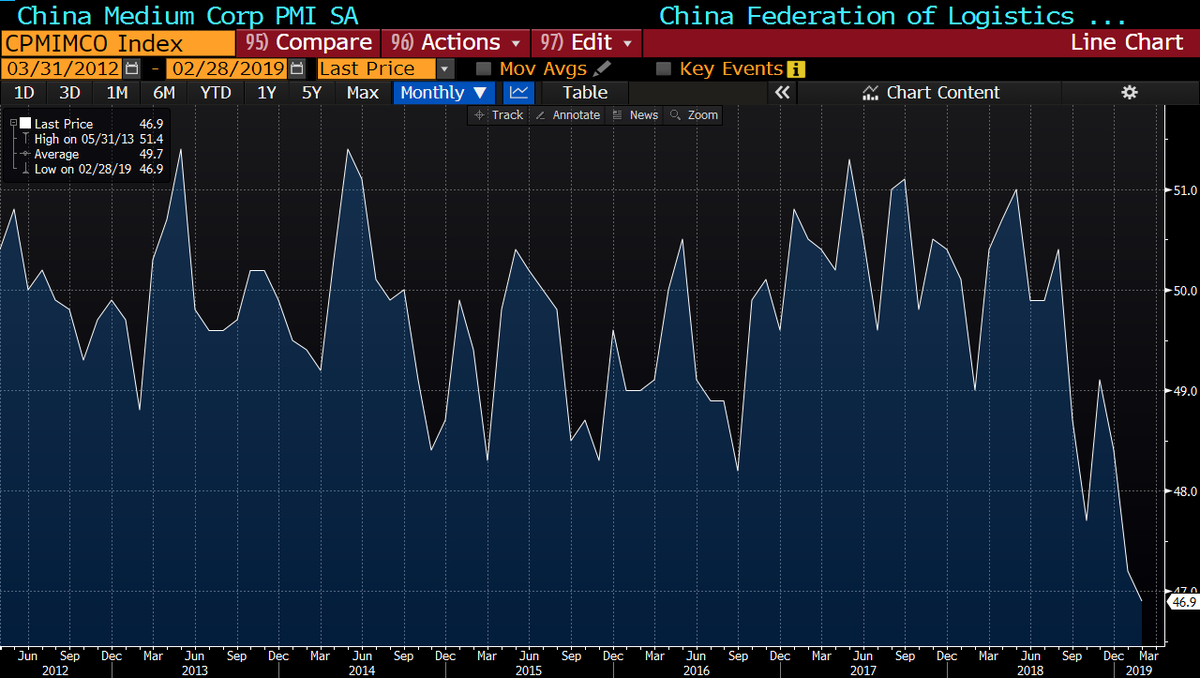

🇨🇳 #China | In October, the new export orders sub-index of the #manufacturing PMI ⬇ further in the contractionary zone. The gauge dropped 1.1pt to 46.9 (lowest since Jan. 2016), following a 1.4pt drop in September.

*Link: bloom.bg/2CTm62t

*Link: bloom.bg/2CTm62t

🇨🇳 #China | Import Expo to be held in Shanghai (from Nov. 5) has likely constrained production in the #manufacturing Yangtze River Delta area.

*The #Shanghai government ordered construction sites in the city to shut down between Oct. 23 and Nov. 12 (bit.ly/2SALteu).

*The #Shanghai government ordered construction sites in the city to shut down between Oct. 23 and Nov. 12 (bit.ly/2SALteu).

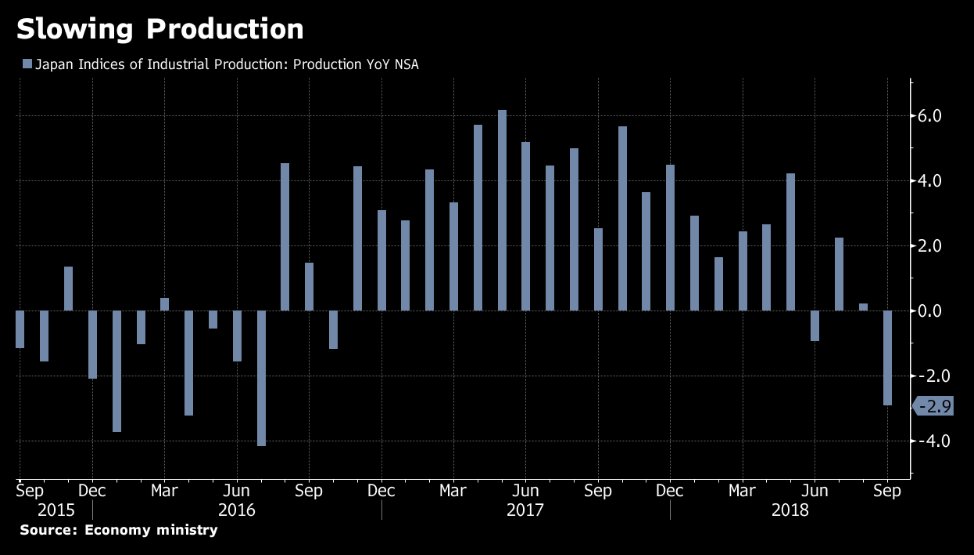

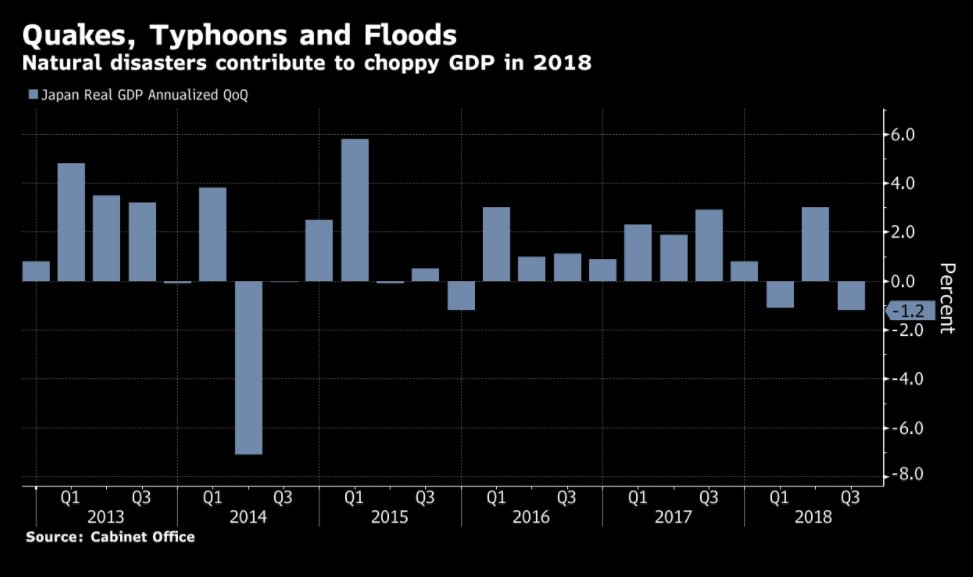

🇯🇵 #JAPAN SEPT PRELIM INDUSTRIAL PRODUCTION M/M: -1.1% V -0.3%E; Y/Y: -2.9% (largest ⬇ since Jul. 2016) V -2.1%E

*Production was impacted by typhoons, earthquakes and the US/China #tradewar

*As already discussed (bit.ly/2P4ImxG), 3Q GDP is likely to surprise ⬇.

*Production was impacted by typhoons, earthquakes and the US/China #tradewar

*As already discussed (bit.ly/2P4ImxG), 3Q GDP is likely to surprise ⬇.

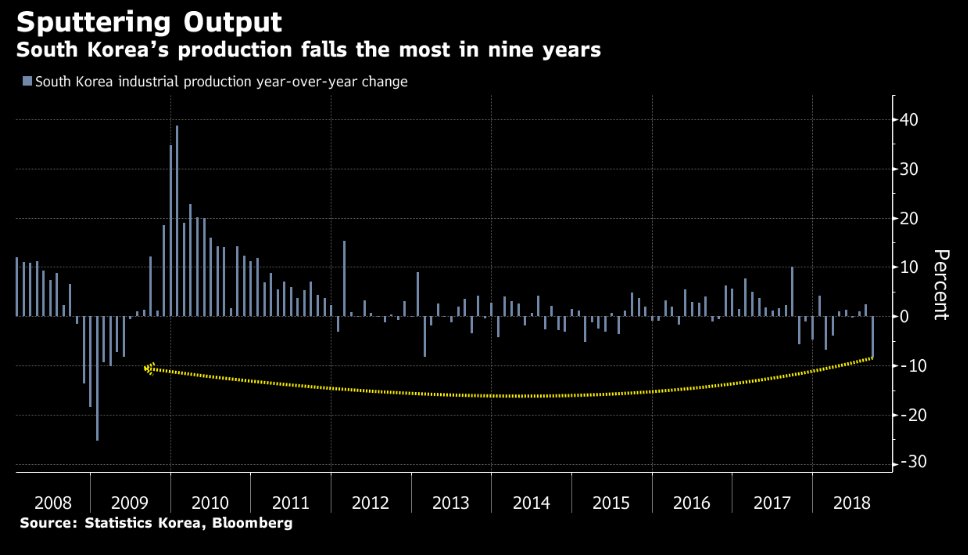

🇰🇷 #SOUTHKOREA SEPT INDUSTRIAL PRODUCTION M/M: -2.5% V -0.5%E; Y/Y: -8.4% (largest decline since March 2009) V -5.1%E

🇩🇪 #GERMANY ENERGY CONSUMPTION TO FALL 'SIGNIFICANTLY' IN 2018: AGEB - BBG

*AGEB SEES GERMAN 2018 ENERGY CONSUMPTION DOWN 5% AT 12,900 PJ

*AGEB SEES GERMAN 2018 ENERGY CONSUMPTION DOWN 5% AT 12,900 PJ

🇰🇷 Samsung Cuts Back Capital Spending as Earnings Top Estimates - Bloomberg

*Capex to drop to 31.8 trillion won in 2018, down 27%

bloomberg.com/news/articles/…

*Capex to drop to 31.8 trillion won in 2018, down 27%

bloomberg.com/news/articles/…

🇩🇪 🇨🇳 #German firms should cut their dependence on the #China market, a leading industry group says in a strategy paper that underscores rising concern over #Beijing's state-driven economic model, according to a draft seen by Reuters.

reuters.com/article/us-ger…

reuters.com/article/us-ger…

🇩🇪 🇨🇳 The 25-page #China position paper from the Federation of German Industries, due to be published in Jan., argues that a long-promised opening of the Chinese market is unlikely to take place and voices concern about ⬆ Communist party control over society and the economy ❗

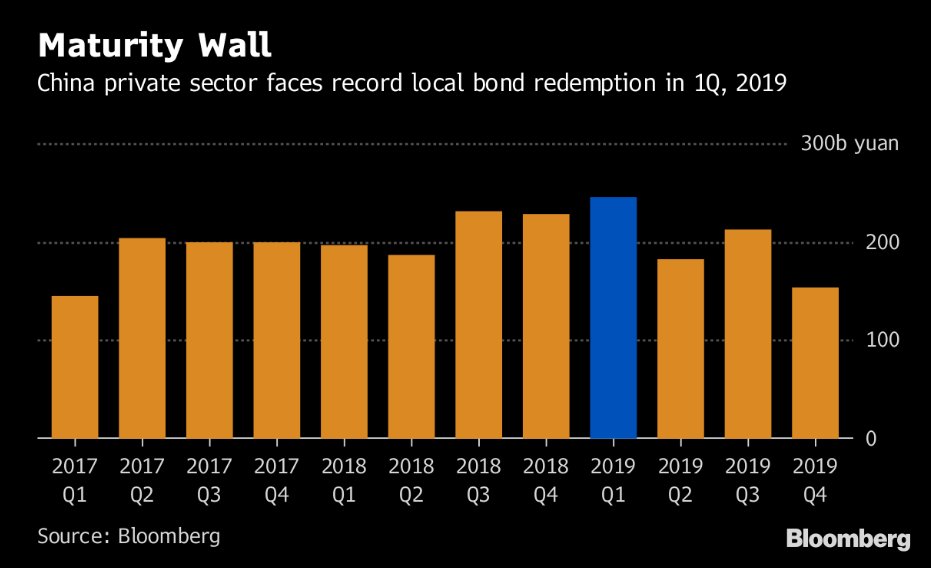

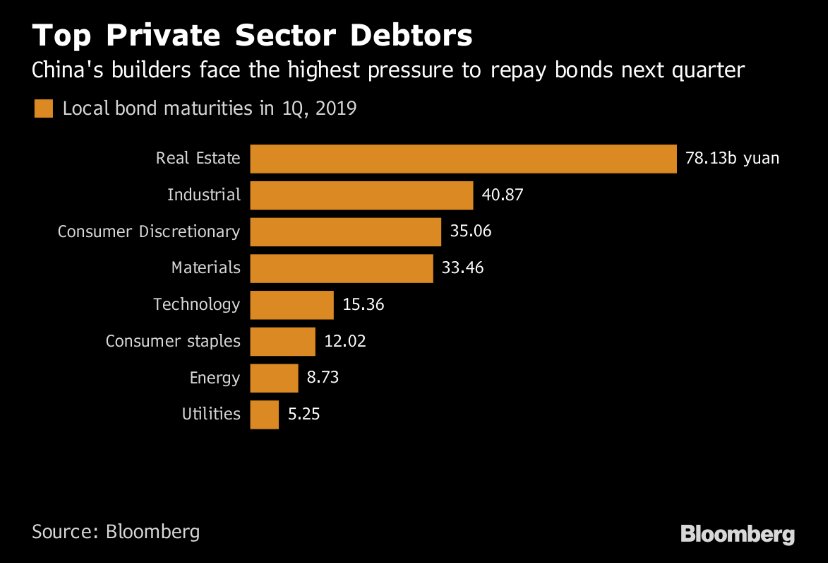

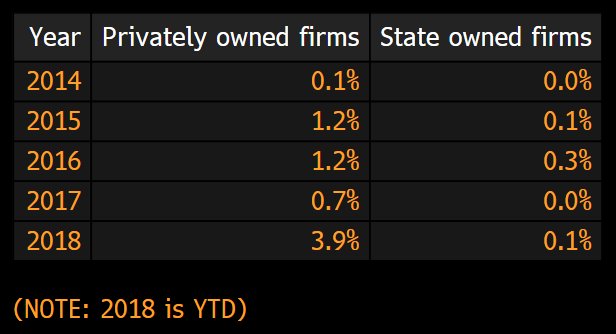

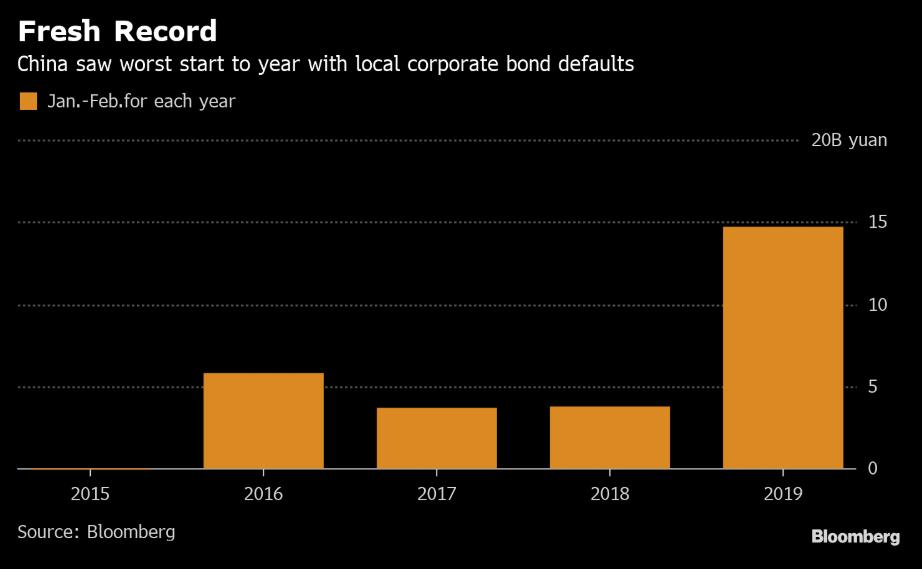

🇨🇳 #China | Non-state firms will have to repay 245.1 billion yuan ($35.2 billion) of bonds in the three months to March, with developers and industrial firms shouldering the bulk of the repayment obligations, data compiled by Bloomberg show.

🇨🇳 Surging default rates for #China local bonds from the private sector are now far higher than those of state-backed companies. The failure rate for non-state companies has jumped to 3.9% this year, from 0.7% in 2017, according to Bloomberg (citing Goldman Sachs data).

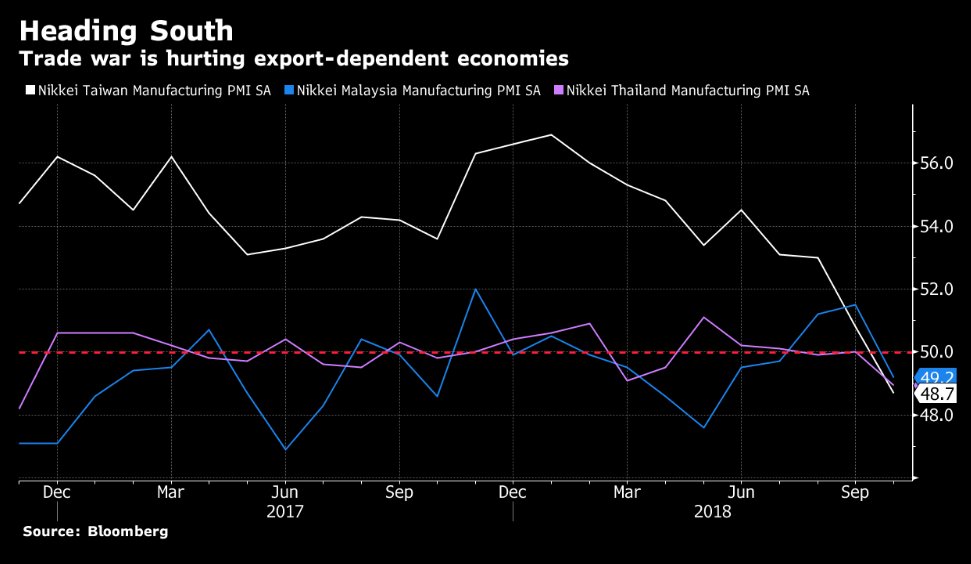

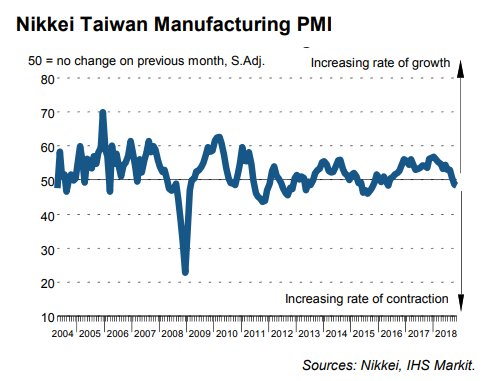

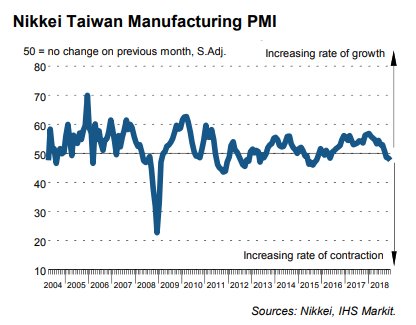

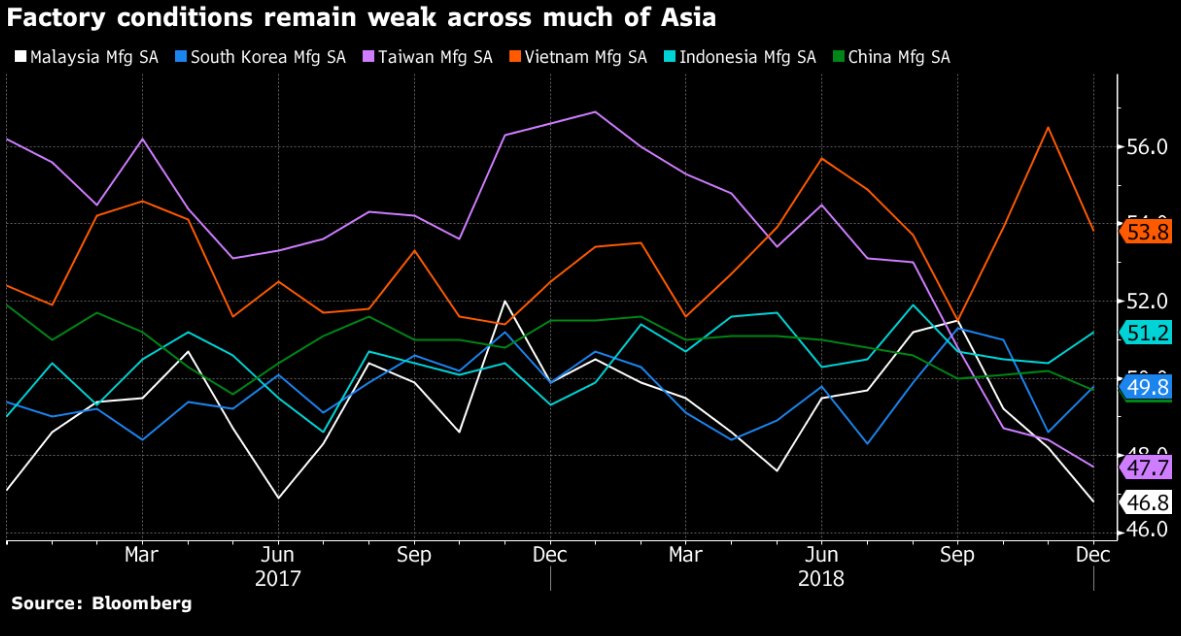

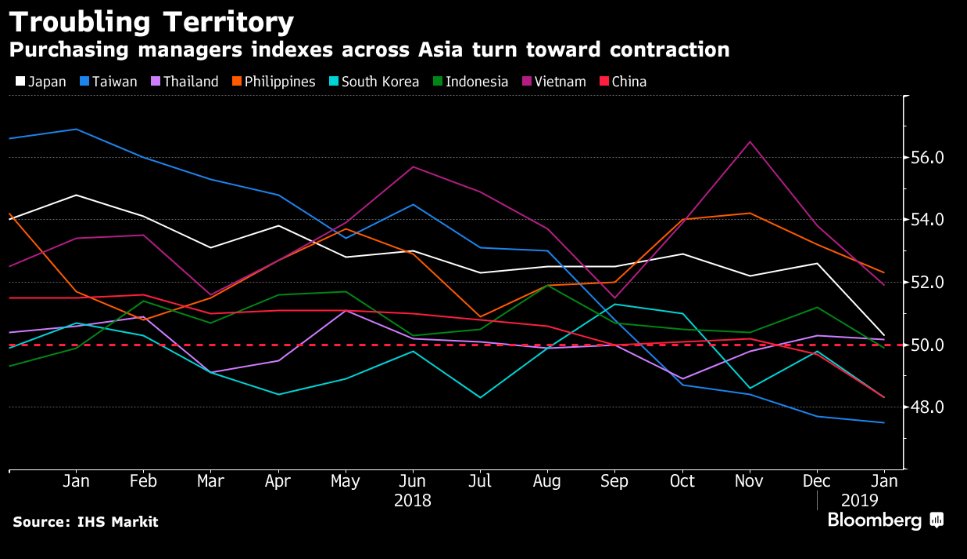

🇹🇼 🇲🇾🇹🇭 #Manufacturing gauges for some of #Asia’s most export-driven economies slipped into ⬇ territory in Oct.

#Taiwan PMI: 48.7 from 50.8 (lowest since May 2016)

#Malaysia PMI: 49.2 from 51.5 (lowest since May 2018)

#Thailand PMI: 48.9 from 50.0 (lowest since Nov. 2016)

#Taiwan PMI: 48.7 from 50.8 (lowest since May 2016)

#Malaysia PMI: 49.2 from 51.5 (lowest since May 2018)

#Thailand PMI: 48.9 from 50.0 (lowest since Nov. 2016)

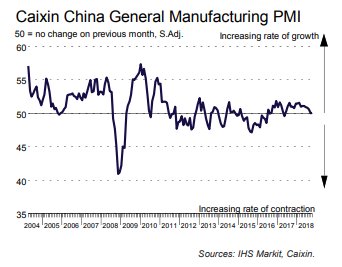

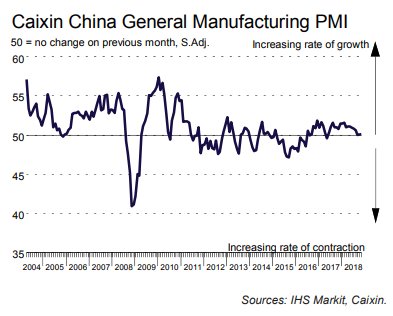

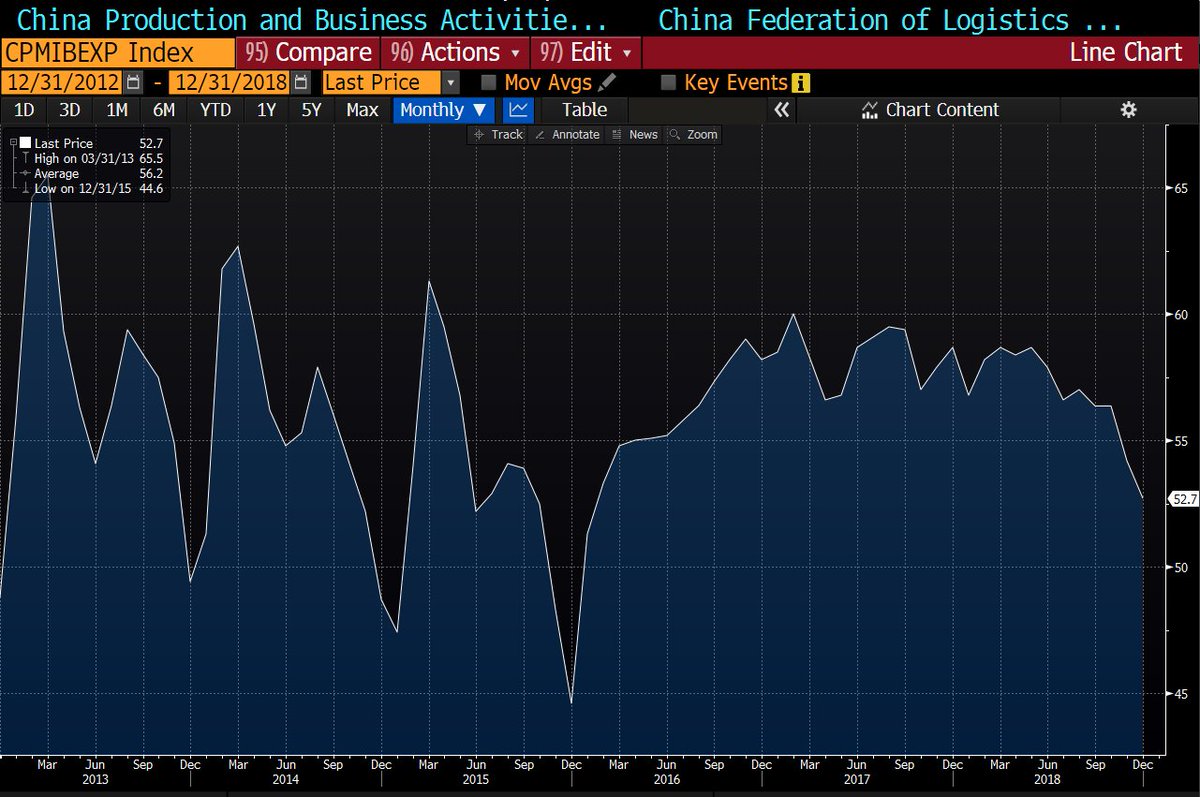

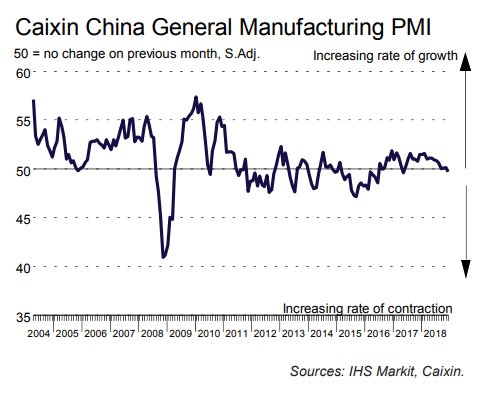

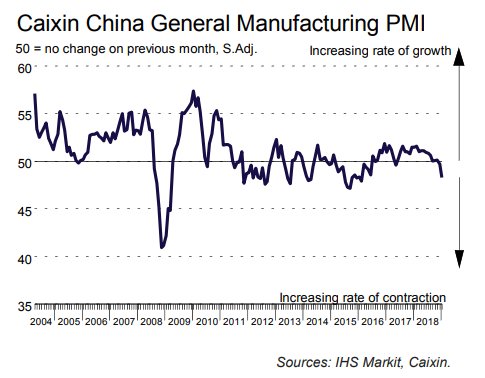

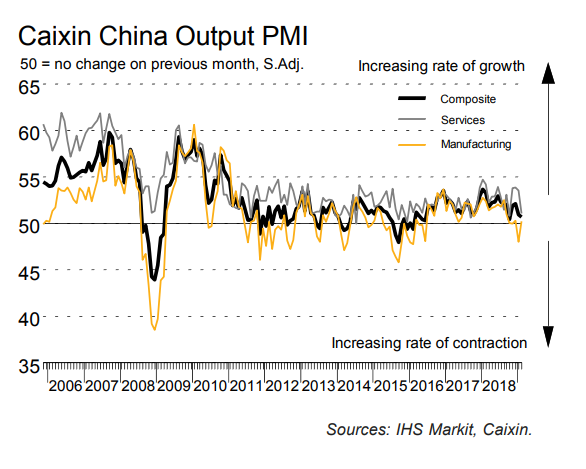

🇨🇳 #China | OCT CAIXIN PMI #MANUFACTURING: 50.1 V 50.0E;

*Business outlook for output hit 11-month low

*The new export orders component surprisingly rose (48.8 vs 47.6 prior) but stayed below the 50 threshold for a seventh consecutive month.

*Link: bit.ly/2SyEZgx

*Business outlook for output hit 11-month low

*The new export orders component surprisingly rose (48.8 vs 47.6 prior) but stayed below the 50 threshold for a seventh consecutive month.

*Link: bit.ly/2SyEZgx

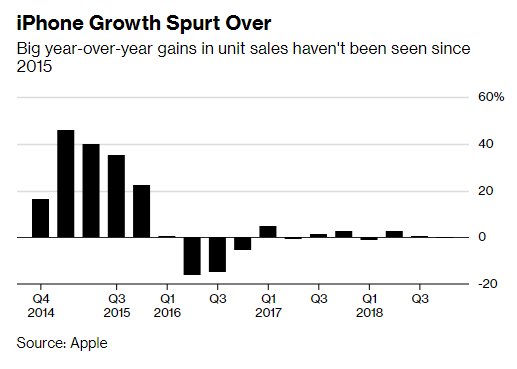

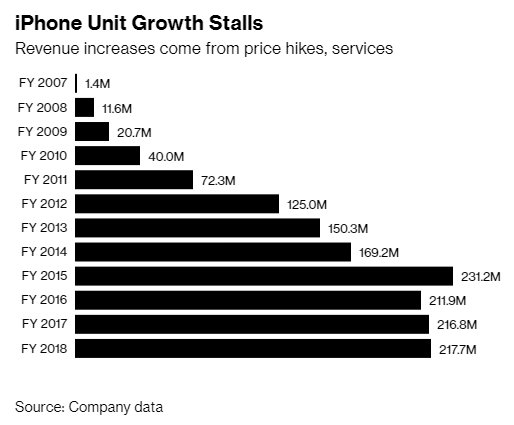

Apple Silence on iPhone Unit Sales Sparks Concern, Shows Future - Bloomberg

Analysts say company doesn’t want to disclose falling numbers

*Link: bloom.bg/2DkRB6g

Analysts say company doesn’t want to disclose falling numbers

*Link: bloom.bg/2DkRB6g

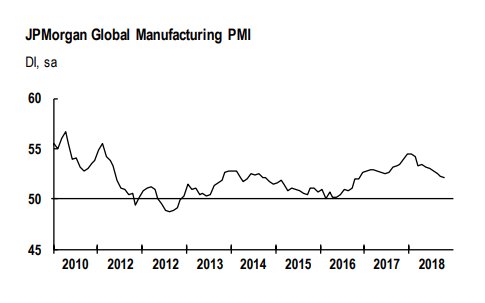

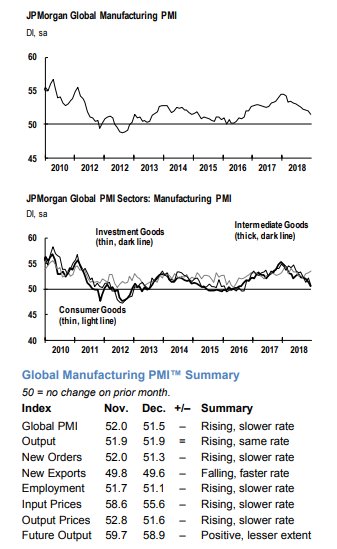

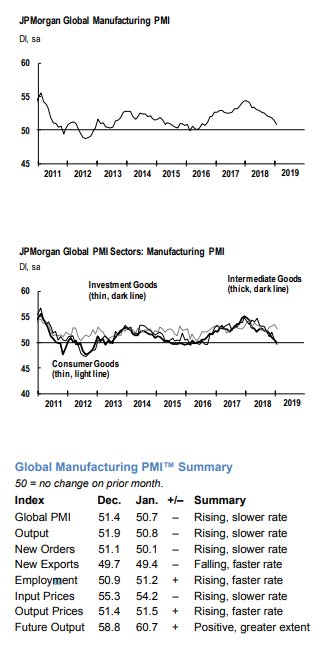

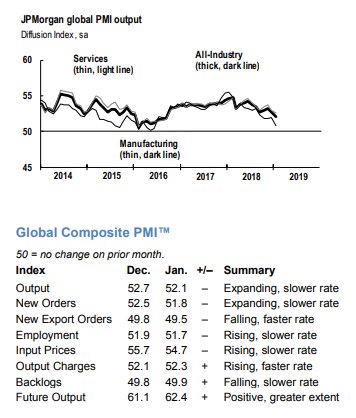

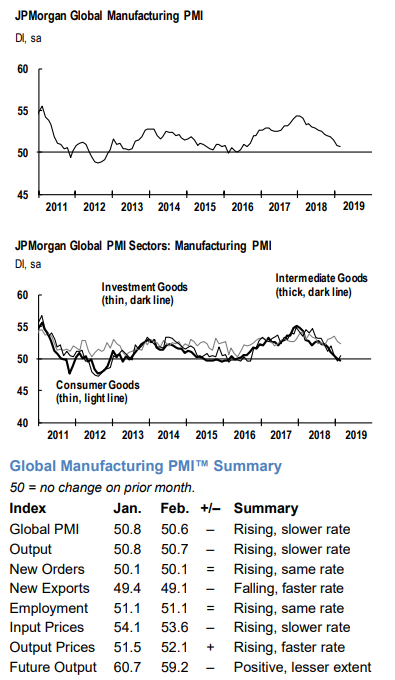

J.P.Morgan Global Manufacturing PMI fell to 52.1 from 52.2 in Sept. (lowest since Nov. 2016)

*New orders: 51.9 vs 52.0 in Sept. (lowest since Sept. 2016.

*Link: bit.ly/2zlCu8f

*New orders: 51.9 vs 52.0 in Sept. (lowest since Sept. 2016.

*Link: bit.ly/2zlCu8f

J.P.Morgan Global Manufacturing PMI: New Exports Orders rebounded to 49.9 vs 49.7 in Sept. but remained in contraction territory.

*It reinforces our view that the consensus is too optimistic about global trade growth (2018 and 2019).

*It reinforces our view that the consensus is too optimistic about global trade growth (2018 and 2019).

J.P.Morgan Global Manufacturing PMI: Output fell to 51.9 vs 52.4 in Sept. (lowest since June 2016)

*It suggests that global industrial production will keep slowing in 4Q.

*It suggests that global industrial production will keep slowing in 4Q.

🇮🇳 Apple's #iPhone sales are set to dip by around a quarter in #India's holiday season fourth quarter, putting them on course for the first full-year fall in four years, industry research firm Counterpoint said on Saturday - The Economic Times

economictimes.indiatimes.com/tech/hardware/…

economictimes.indiatimes.com/tech/hardware/…

World Economy Risks Returning to Sync, This Time to the Downside - Bloomberg

*Lengthening worry list stretches from trade to rising rates

*Link: bloom.bg/2QicL7U

*Lengthening worry list stretches from trade to rising rates

*Link: bloom.bg/2QicL7U

🇯🇵 Subaru expects 30% profit fall after engine recall - Nikkei

*Domestic sales for the first half fell 20% on the year to 67,000 vehicles, according to preliminary figures.

*Worldwide production for the first half decreased 6% to 490,000 vehicles.

asia.nikkei.com/Business/Compa…

*Domestic sales for the first half fell 20% on the year to 67,000 vehicles, according to preliminary figures.

*Worldwide production for the first half decreased 6% to 490,000 vehicles.

asia.nikkei.com/Business/Compa…

🇯🇵 🇨🇳 #Tradewar squeezes corporate earnings in #Japan and #China - Nikkei

*"Shipment to China has slowed. Recent orders are down about 30% from a year earlier" Yoshimaro Hanaki, president of Japanese machine tool builder Okuma has said.

asia.nikkei.com/Economy/Trade-…

*"Shipment to China has slowed. Recent orders are down about 30% from a year earlier" Yoshimaro Hanaki, president of Japanese machine tool builder Okuma has said.

asia.nikkei.com/Economy/Trade-…

🇨🇳 Default Risks Rise in $355 Billion #China Builder Bond Market - Bloomberg

*At least 4 property-related firms defaulted on bonds in 2018

*S&P expects defaults to rise, asks investors to be cautious

*Link: bloom.bg/2DlU5Bs

*At least 4 property-related firms defaulted on bonds in 2018

*S&P expects defaults to rise, asks investors to be cautious

*Link: bloom.bg/2DlU5Bs

🇨🇳 New onshore Co bond defaults reached 72.6b yuan ($10.5b) this year, including 23 private and 50 public offerings - Bloomberg

*#China offshore corporate-bond defaults amounted to $2.53b this year, including 9 dollar-denominated bonds and one HK dollar-based note.

*#China offshore corporate-bond defaults amounted to $2.53b this year, including 9 dollar-denominated bonds and one HK dollar-based note.

🇩🇪#Germany Oct Construction PMI: 49.8 v 50.2 prior (first decline since March 2017) - Markit

*Link: bit.ly/2zyzHst

➡ It can be partially explained by adverse weather conditions.

*Link: bit.ly/2zyzHst

➡ It can be partially explained by adverse weather conditions.

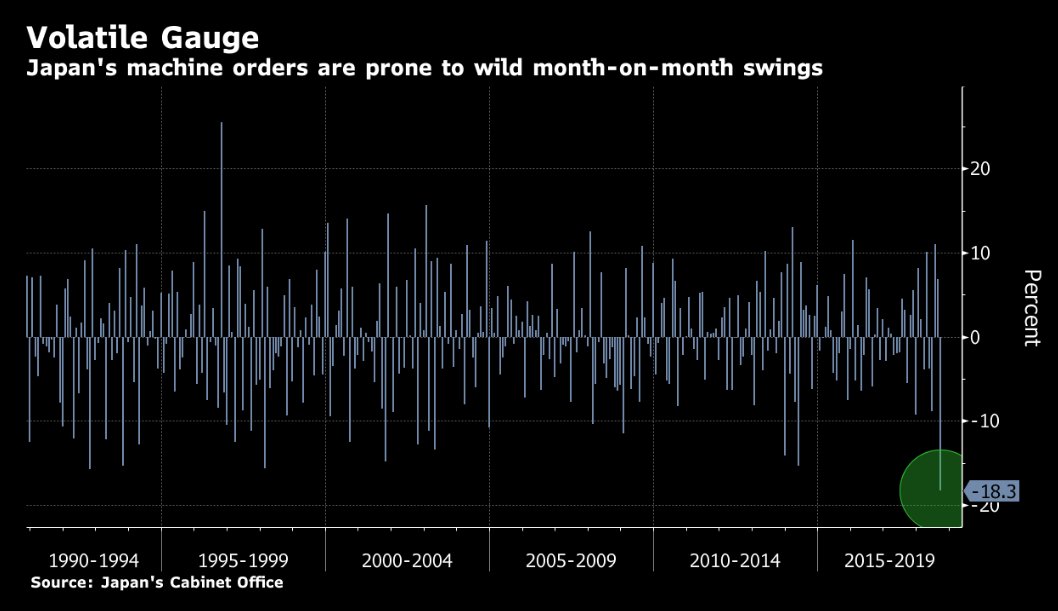

🇯🇵 #Japan core machine orders fall 18.3% in September, the largest month-on-month decline on record.

*Excluding disasters, a global and Chinese economic slowdown likely weighted ⬇.

*Excluding disasters, a global and Chinese economic slowdown likely weighted ⬇.

Despite several proxies (bit.ly/2PdAXMi; bit.ly/2P4ImxG; bit.ly/2QqJxnt) suggest a sharp contraction, economists were once again surprised ⬇

*🇯🇵 2018 GDP forecasts remain optimistic

*🇯🇵 2018 GDP forecasts remain optimistic

Qualcomm Gives Weak Forecast on Loss of #Apple #iPhone Orders - Bloomberg

*Said demand was lower in general but expects that to reverse in 2H19 as new, fifth-generation or 5G, phone services and networks are deployed.

*Link: bloom.bg/2OxsX3M

*Said demand was lower in general but expects that to reverse in 2H19 as new, fifth-generation or 5G, phone services and networks are deployed.

*Link: bloom.bg/2OxsX3M

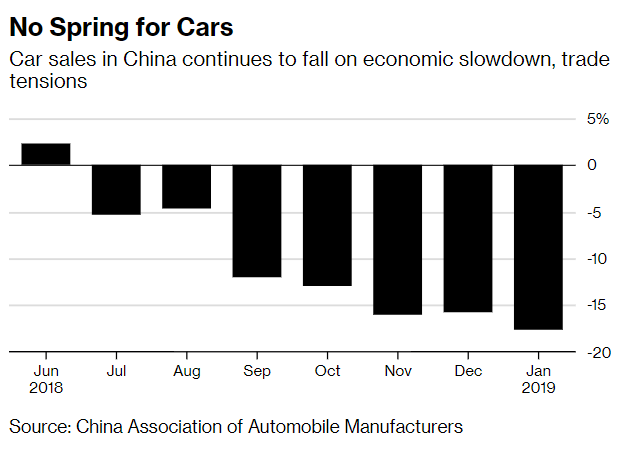

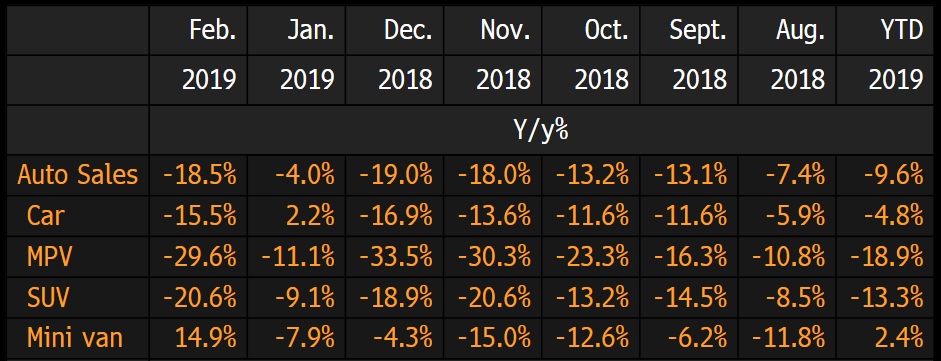

🇨🇳 #CHINA OCT. RETAIL PASSENGER VEHICLE SALES -13.2% ON YEAR: PCA - BBG

*CHINA OCT. RETAIL PASSENGER VEHICLE SALES 1.98M UNITS

*CHINA OCT. RETAIL PASSENGER VEHICLE SALES 1.98M UNITS

🇪🇺 Eu Commission is likely to revise ⬇ its GDP forecasts this morning as the latest data confirmed the sharp slowdown in 3Q:

🇩🇪 Sept. Exports M/M: -0.8% v +0.4%e

🇫🇷 Sept. Exports: -1.8% v -0.2% prior

🇩🇪 Sept. Exports M/M: -0.8% v +0.4%e

🇫🇷 Sept. Exports: -1.8% v -0.2% prior

🇫🇷 #France | With an expected overall decrease of 1% in investment for 2018, business managers have lowered their July 2018 estimate by 5 points - INSEE

*Link: bit.ly/2RIgBHM

*Link: bit.ly/2RIgBHM

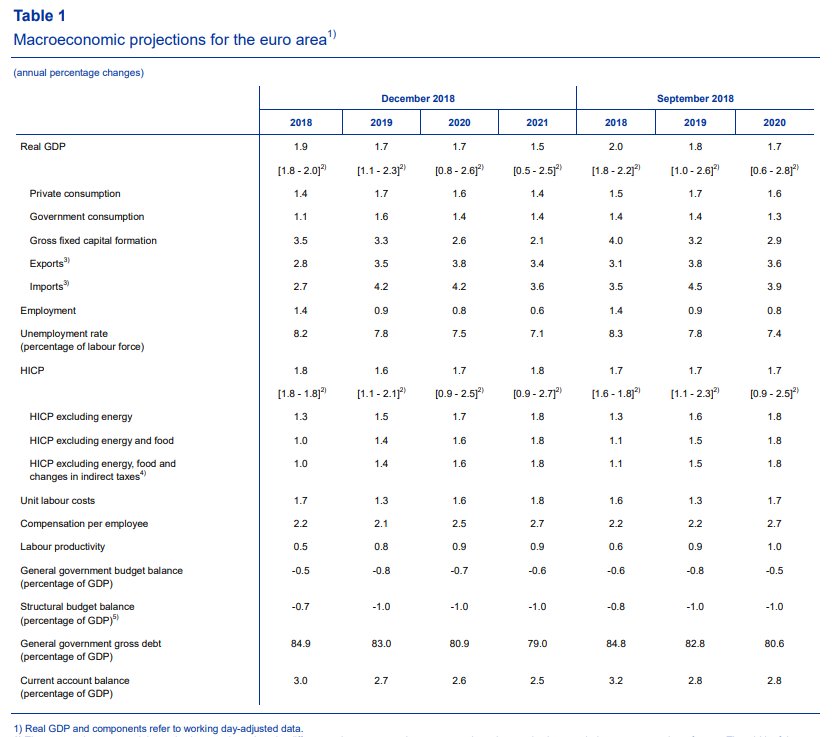

🇪🇺 European Commission cuts its 2019 GDP forecast to 1.9% from 2.0% but keeps unchanged its forecast for 2018 at 2.1%.

*It seems very optimistic. Sept. ECB forecast for 2018 was 2.0% but the central bank has already acknowledged that latest figures have been weaker than expected

*It seems very optimistic. Sept. ECB forecast for 2018 was 2.0% but the central bank has already acknowledged that latest figures have been weaker than expected

🇬🇧 #BOE'S BROADBENT SEES SIGNS OF SOMEWHAT WEAKER GROWTH IN 4Q - BBG

*BROADBENT: BREXIT UNCERTAINTY HITS PRODUCTIVITY, INVESTMENT

*BROADBENT: UNCERTAINTIES ON THINGS IN FORECASTS ARE MATERIAL

*BROADBENT: BREXIT UNCERTAINTY HITS PRODUCTIVITY, INVESTMENT

*BROADBENT: UNCERTAINTIES ON THINGS IN FORECASTS ARE MATERIAL

🇪🇺 #ECB'S GUINDOS SEES DOWNSIDE RISKS TO EURO-AREA ECONOMY - BBG

🇪🇺 #ECB'S PRAET SAYS THERE'S BEEN SOME SLOWDOWN IN EURO ECONOMY - BBG

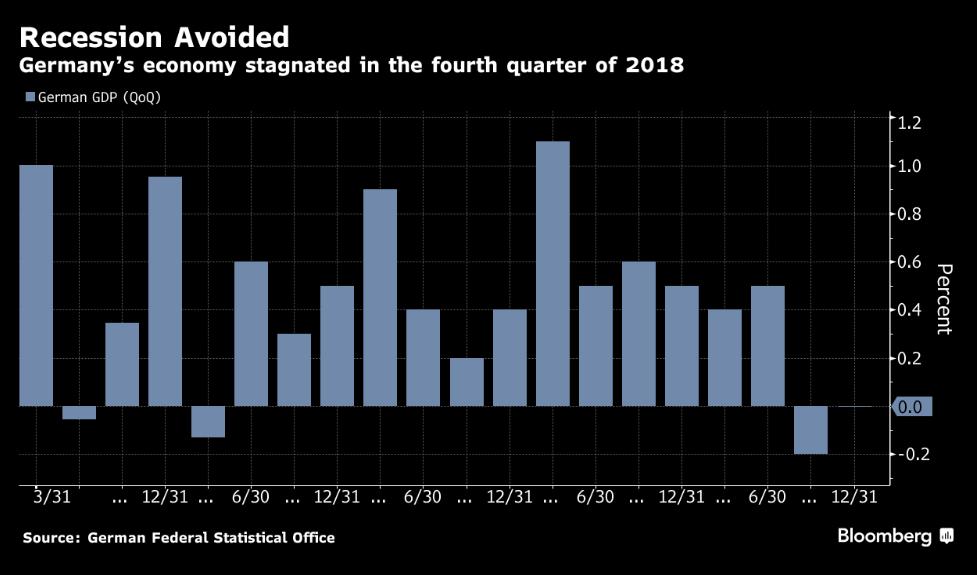

As flagged on @bfm_eco, #German GDP fell 0.2% QoQ in 3Q (confirming that the consensus forecast for 2018 remains optimistic).

🇩🇪 #GERMANY Q3 PRELIMINARY GDP Q/Q: -0.2% V -0.1%E; GDP Y/Y: 1.1% V 1.3%E

bfmbusiness.bfmtv.com/mediaplayer/vi…

🇩🇪 #GERMANY Q3 PRELIMINARY GDP Q/Q: -0.2% V -0.1%E; GDP Y/Y: 1.1% V 1.3%E

bfmbusiness.bfmtv.com/mediaplayer/vi…

#Japan | As mentioned several times (bit.ly/2B4a5Wy), the consensus forecast for 🇯🇵 2018 GDP (at 1.1%) is optimistic:

*Q3 PRELIM GDP ANNUALIZED Q/Q: -1.2% V -1.0%E

*Q3 PRELIM GDP ANNUALIZED Q/Q: -1.2% V -1.0%E

🇩🇪 #GERMANY INDUSTRY ASSOCIATION BDI CUTS EXPORT FORECAST TO 3 PCT VS 3.5 PCT - RTRS

🇪🇺 #ECB'S KNOT SAYS THERE ARE DOWNSIDE RISKS ON THE HORIZON - BBG

🇺🇸 Nvidia Corp., the biggest maker of chips for computer graphics cards, gave a weak sales forecast for the current quarter, showing the lingering loss of demand from the collapse of #cryptocurrency mining - Bloomberg

*Link: bloom.bg/2zbCLvk

*Link: bloom.bg/2zbCLvk

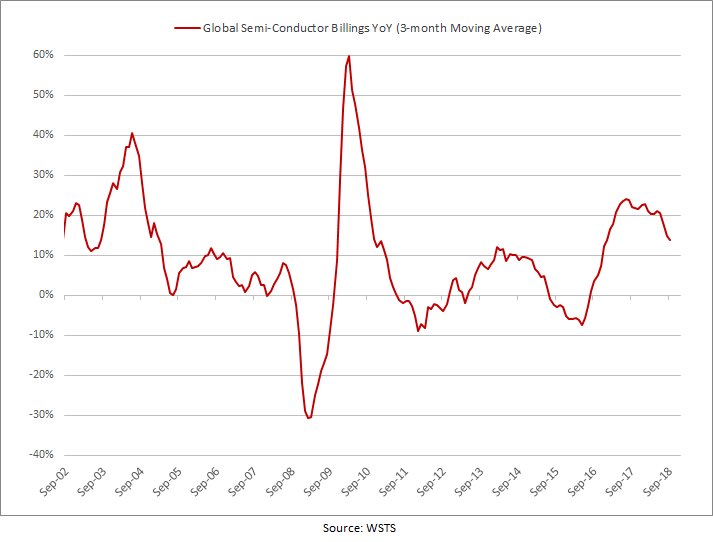

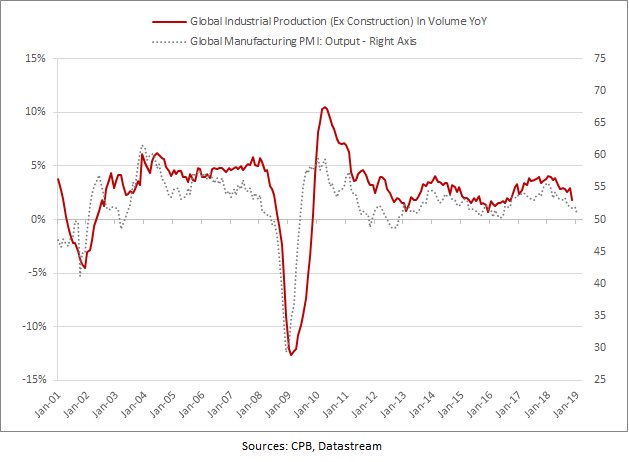

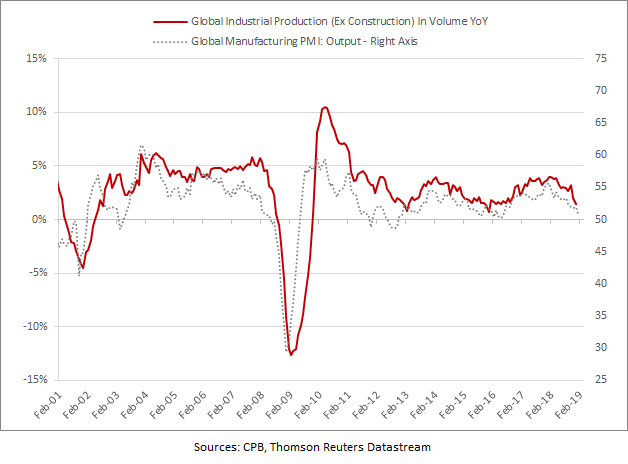

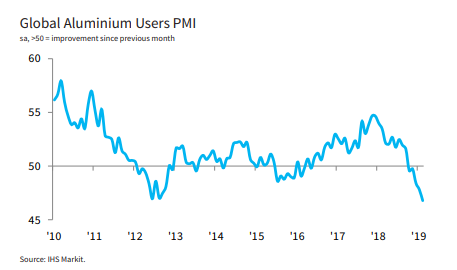

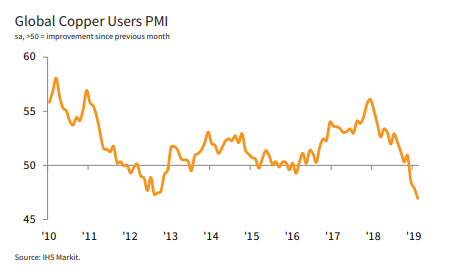

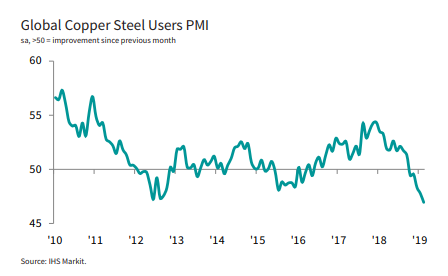

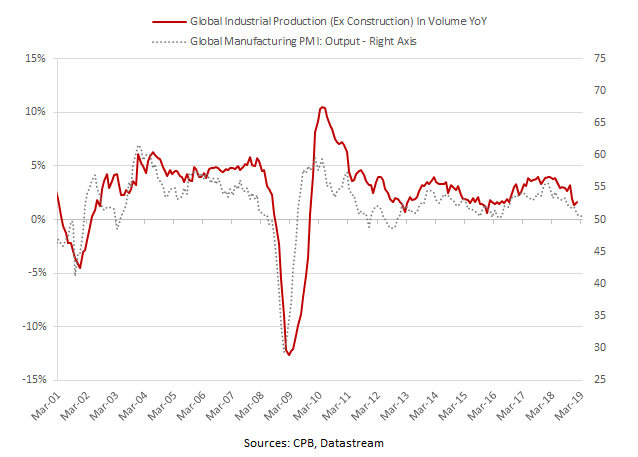

Global production growth (ex construction) has weakened since Feb. It has suffered from a normalization in the semi-conductor sector after having benefited from sizeable demand tailwinds (Iphone, Bitcoin mining, etc.) and was ⬇ impacted by political uncertainties and tariffs.

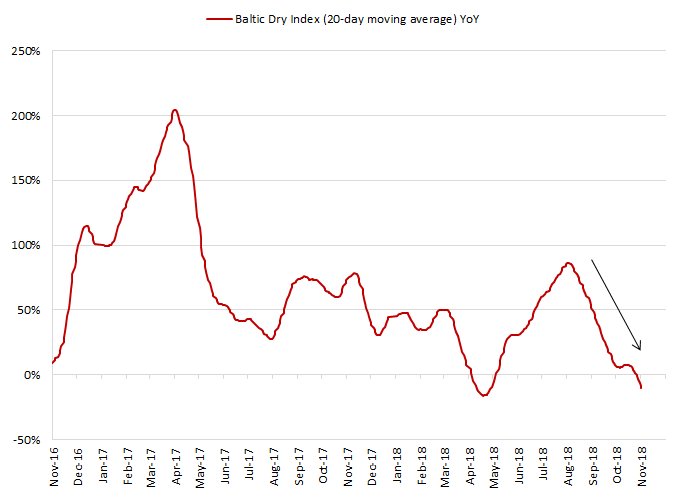

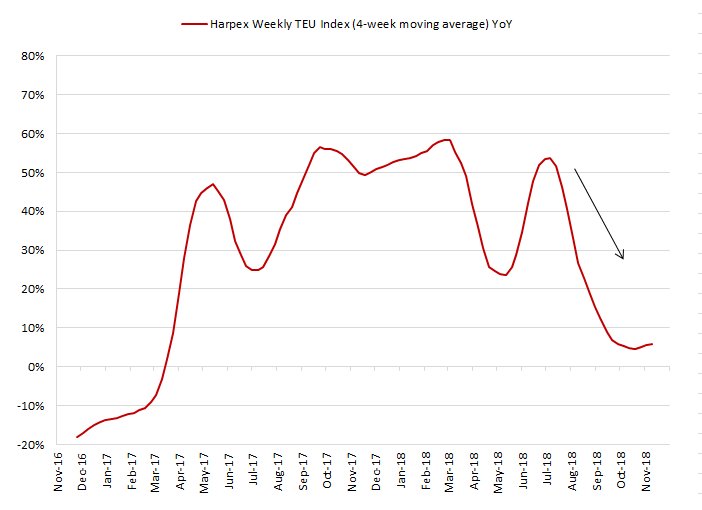

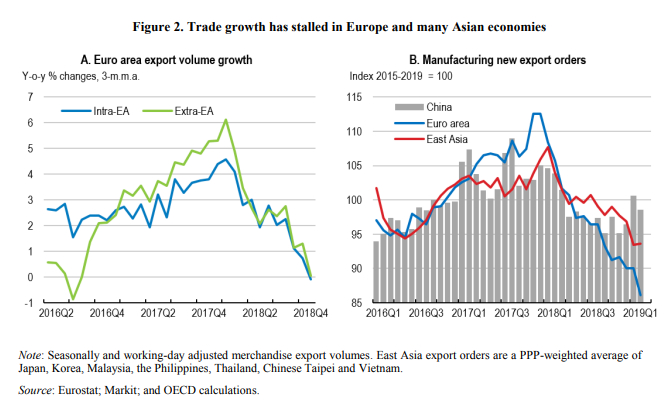

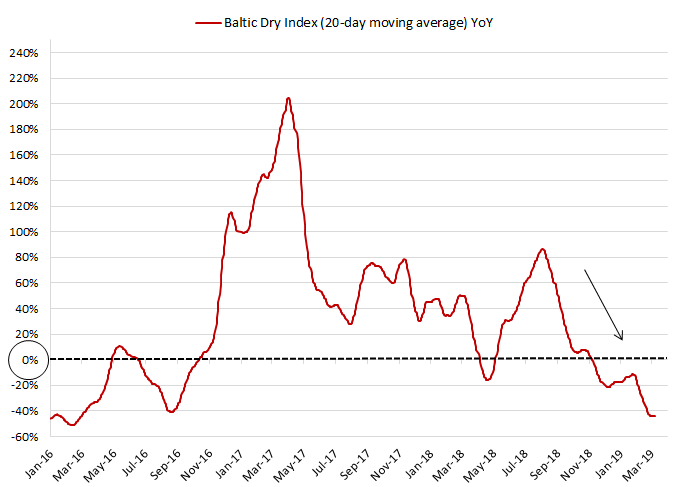

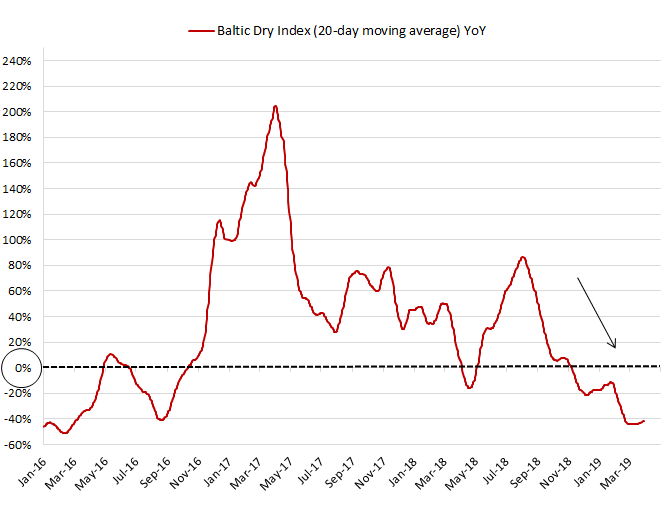

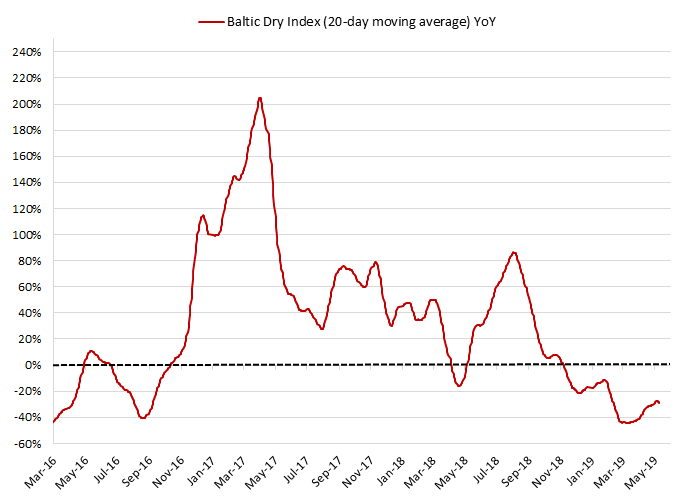

Most of freight proxies (Baltic Dry Index, Harpex, etc.) suggest that global trade growth has slowed sharply since July 2018.

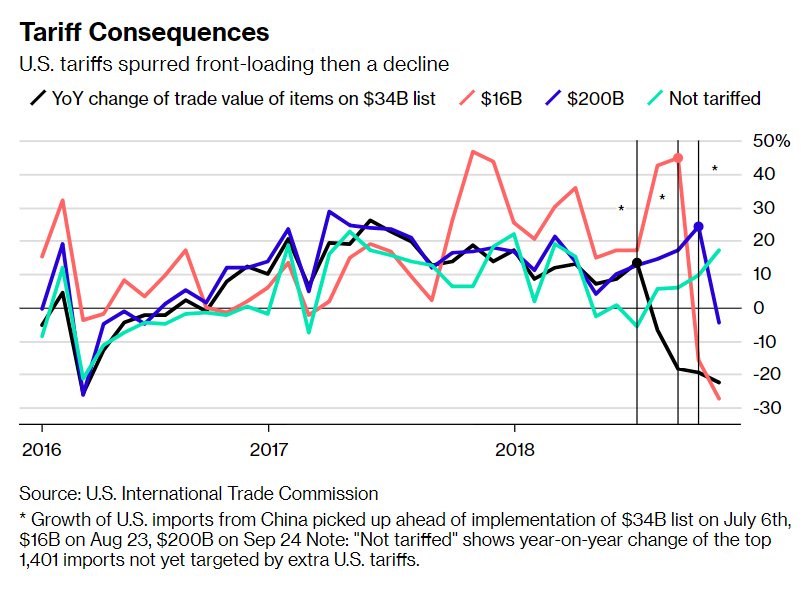

🇺🇸 🇨🇳 If the U.S. implements tariff hike on $200b Chinese goods to 25% from Jan. 1, 2019 (as suggested by Ross), global trade growth could take a significant hit at some point in Feb. (amplified by the shift in Chinese New Year dates).

🇺🇸 #Apple Suppliers Suffer as It Struggles to Forecast #iPhone Demand - WSJ

*In recent weeks, Apple slashed production orders for all three iPhone models that it unveiled in September.

wsj.com/articles/apple…

*In recent weeks, Apple slashed production orders for all three iPhone models that it unveiled in September.

wsj.com/articles/apple…

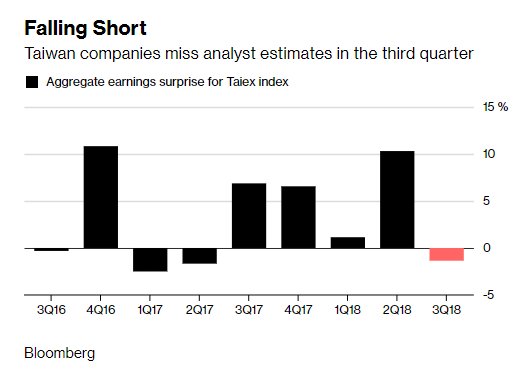

🇹🇼 #Taiwan Braces for Earnings Gloom as #IPhone, #TradeWar Bite - Bloomberg

*Apple suppliers including Hon Hai missed 3Q net income est.

*Link: bloom.bg/2A5Djmb

*Apple suppliers including Hon Hai missed 3Q net income est.

*Link: bloom.bg/2A5Djmb

🇺🇸 🇨🇳 🇨🇦 🇪🇺 🇯🇵 🇬🇧 Growth in money supplies is continuing to drop around the world - Bloomberg

🇺🇸 #Apple Shares Near Bear Market Territory - Bloomberg

*Company has fewest positive analyst ratings among big #tech

*Link: bloom.bg/2OTUPiv

*Company has fewest positive analyst ratings among big #tech

*Link: bloom.bg/2OTUPiv

🇺🇸 #Apple said to cut orders from two #China component suppliers by 30% on lukewarm #iPhone XR demand - SCMP

scmp.com/tech/big-tech/…

scmp.com/tech/big-tech/…

🇬🇧 #BOE'S SAUNDERS: GROWTH IN 4Q, 1Q 2019 WILL LIKELY SLOW - BBG

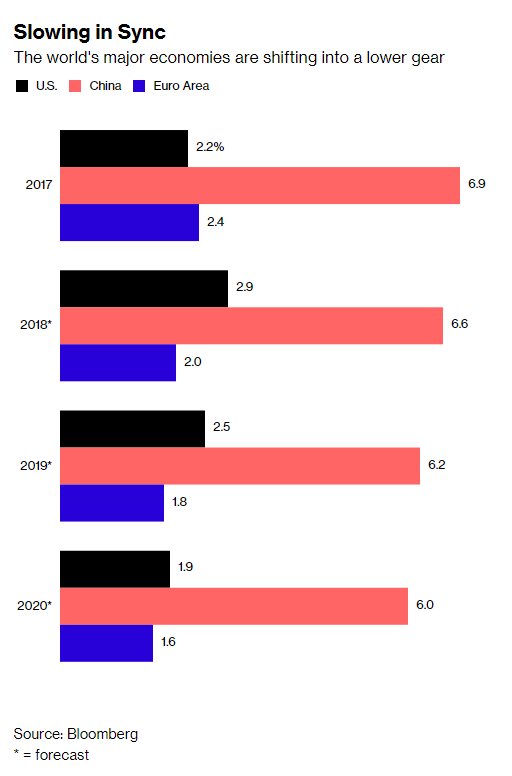

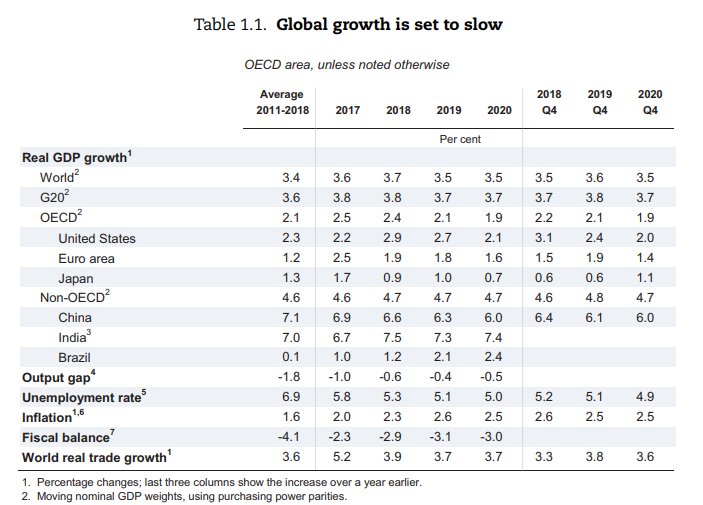

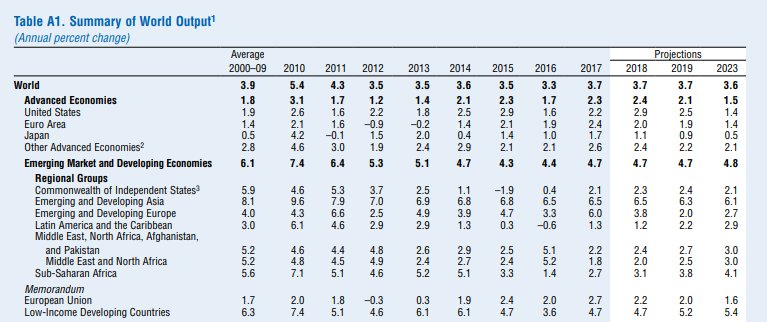

#OECD CUTS 2019 GLOBAL GROWTH FORECAST TO 3.5% VS 3.7% - BBG

*OECD LOWERS EURO-AREA GROWTH FORECASTS FOR 2018, 2019

*OECD SAYS ‘DOWNSIDE RISKS ABOUND’ FOR GLOBAL ECONOMY

*OECD LOWERS EURO-AREA GROWTH FORECASTS FOR 2018, 2019

*OECD SAYS ‘DOWNSIDE RISKS ABOUND’ FOR GLOBAL ECONOMY

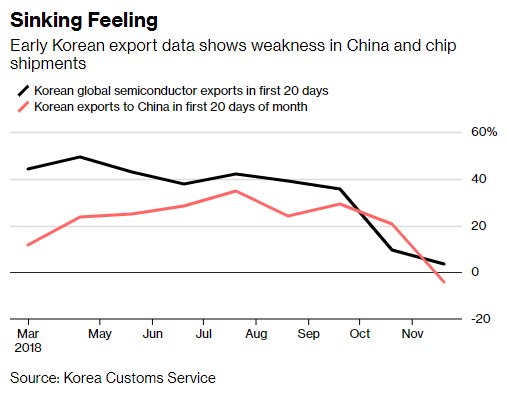

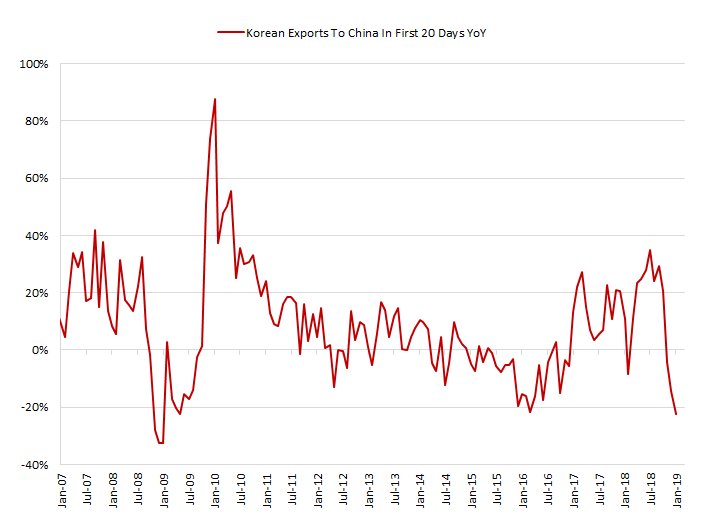

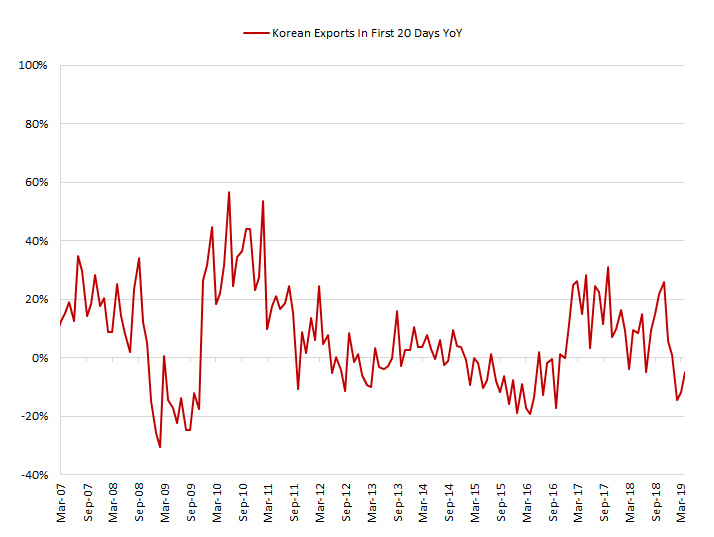

#OECD Sees Trade Tensions as Risk for Korean Exports to #China.

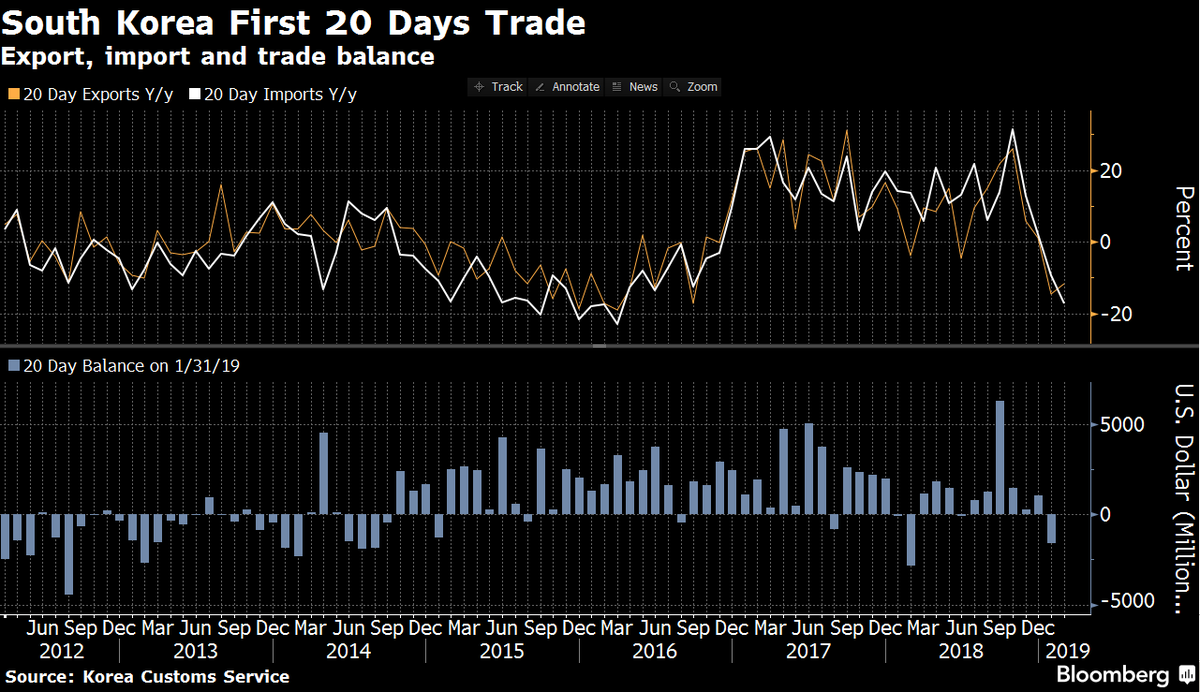

This morning, trade data for the first 20 days of Nov. showed a 4.3% ⬇ in 🇰🇷 exports to 🇨🇳, the first fall outside holiday-affected months since late 2016.

*Link (Korean): bit.ly/2DRGuSR

This morning, trade data for the first 20 days of Nov. showed a 4.3% ⬇ in 🇰🇷 exports to 🇨🇳, the first fall outside holiday-affected months since late 2016.

*Link (Korean): bit.ly/2DRGuSR

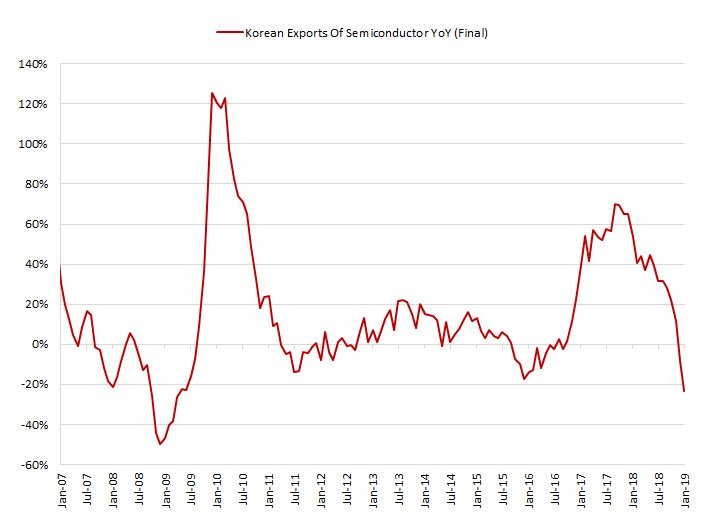

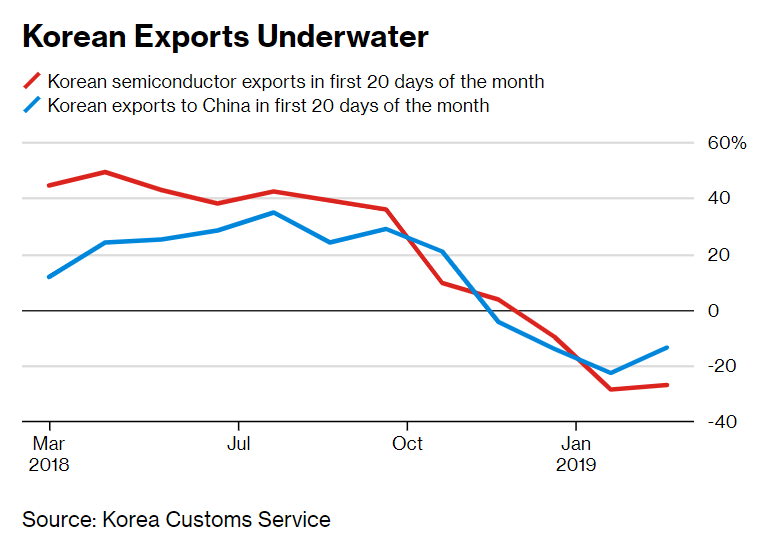

🇰🇷 #SouthKorea | A slowdown in the expansion of chip exports to 3.5% compares with gains of at least 35% in each of the first nine months of 2018 also suggests a rapid softening of the global #tech sector, for which Korea is a key supplier.

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

Several #OECD GDP forecasts seem to be the first one in line with reality with:

*Euro Area 2018 at +1.9% (vs 2.0% for ECB and 2.1% for EU Commission)

*Global GDP 2019 at 3.5% (vs 3.7% for the consensus)

*Link: bit.ly/2QbkeZM

*Euro Area 2018 at +1.9% (vs 2.0% for ECB and 2.1% for EU Commission)

*Global GDP 2019 at 3.5% (vs 3.7% for the consensus)

*Link: bit.ly/2QbkeZM

However, risks associated to OECD forecast for Global GDP in 2019 (+3.5%) look skewed to the downside given their optimistic assumption concerning world real trade growth (+3.7% for 2019).

#WTO says #G20 trade restrictions soar, cover $481 billion of #trade - Reuters

reuters.com/article/us-g20…

reuters.com/article/us-g20…

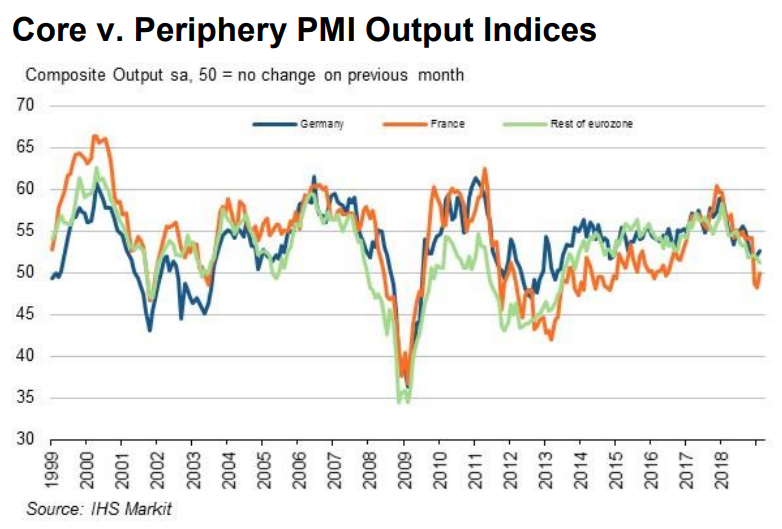

🇪🇺 🇩🇪 As expected (bit.ly/2DTybpG), Eurozone PMIs for Nov. are likely to keep declining.

*#Germany PMI Composite Output Index ⬇ to a 47-month low.

*Link: bit.ly/2TBrltt

*#Germany PMI Composite Output Index ⬇ to a 47-month low.

*Link: bit.ly/2TBrltt

🇩🇪 #Germany NOV PRELIMINARY #MANUFACTURING PMI: 51.6 V 52.2E (32-month low)

*Manufacturing order books fell for the second month running and to the greatest extent in four years.

*This largely reflected a solid and accelerated decline in goods exports orders.

*Manufacturing order books fell for the second month running and to the greatest extent in four years.

*This largely reflected a solid and accelerated decline in goods exports orders.

🇪🇺 #EUROZONE NOV PRELIMINARY #MANUFACTURING PMI: 51.5 V 52.0E (30-month low)

*New Orders 48.9 v 49.8 prior (2nd straight contraction and lowest since Nov. 2014)

*Services PMI: 53.1 v 53.6e (25-month low)

*Composite PMI 52.4 v 53.0e (47-month low)

*Link: bit.ly/2Ks4f4h

*New Orders 48.9 v 49.8 prior (2nd straight contraction and lowest since Nov. 2014)

*Services PMI: 53.1 v 53.6e (25-month low)

*Composite PMI 52.4 v 53.0e (47-month low)

*Link: bit.ly/2Ks4f4h

🇪🇺 #EUROZONE NOV PRELIMINARY PMIs:

*The weaker rise in business activity was linked to a 2nd successive monthly ⬇ in new export orders across the manufacturing and service sectors.

*The drop in exports was the largest seen in the 4-year history of this new survey indicator ❗

*The weaker rise in business activity was linked to a 2nd successive monthly ⬇ in new export orders across the manufacturing and service sectors.

*The drop in exports was the largest seen in the 4-year history of this new survey indicator ❗

🇪🇺 #Eurozone | It confirms my view that latest ECB (Sept.) and EC forecasts (Nov.) for 2018 and 2019 GDP remain optimistic.

*Despite a drop in EUR, exports remain under pressure due to global trade growth slowdown.

*Despite a drop in EUR, exports remain under pressure due to global trade growth slowdown.

🇪🇺 The new ⬇ in export orders (bit.ly/2FE60MT) in Nov. raises concerns about a sharp slowdown in global trade growth in early 2019 (likely from Feb. due to shift in Chinese New Year dates).

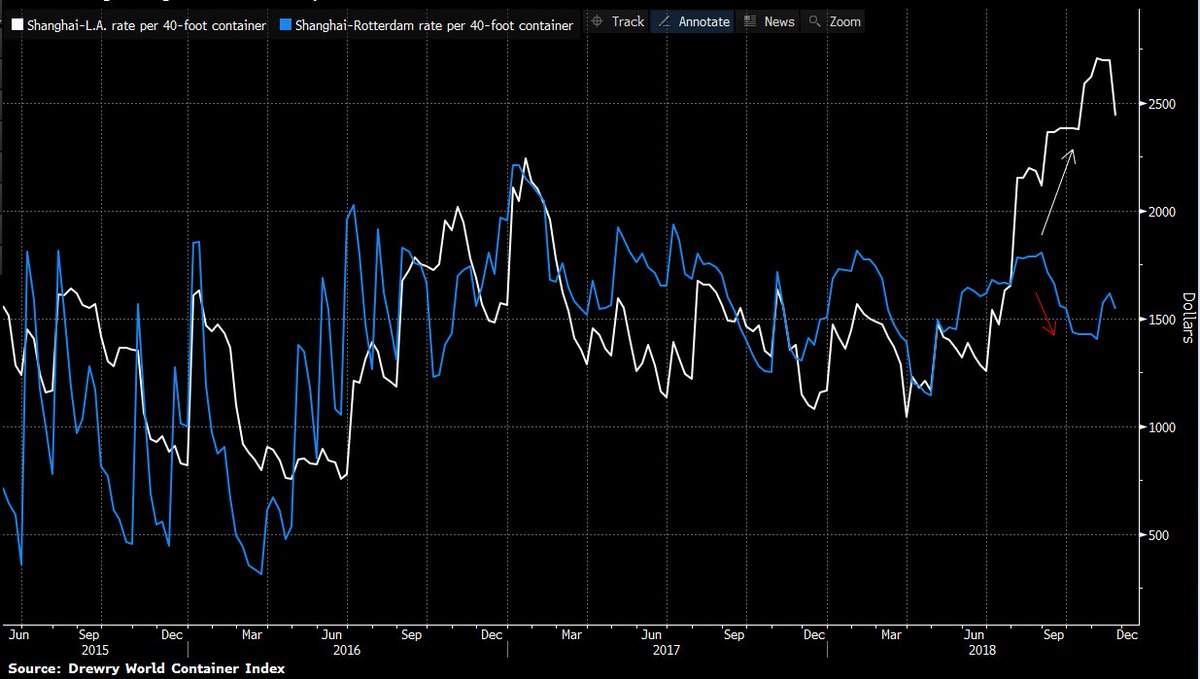

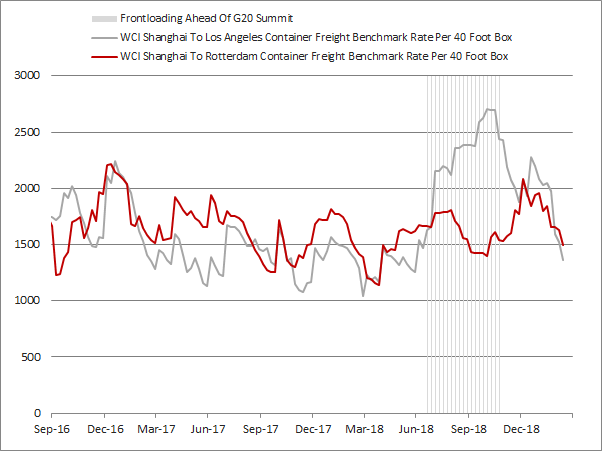

I still think that the underlying trend in global trade growth is weaker than most economists assume. The headline reflects frontloading ahead of the implementation of tariffs. Still now, freight rates on shipping routes from #China’s ports to the U.S. are higher than elsewhere.

🇯🇵 #JAPAN NOV PRELIM #MANUFACTURING PMI: 51.8 V 52.9 PRIOR (lowest since Nov 2016)

*New orders contracted for the first time since Sept 2016 while new export orders showed expansion (though at a slower pace).

*Link: bit.ly/2DWu7ot

*New orders contracted for the first time since Sept 2016 while new export orders showed expansion (though at a slower pace).

*Link: bit.ly/2DWu7ot

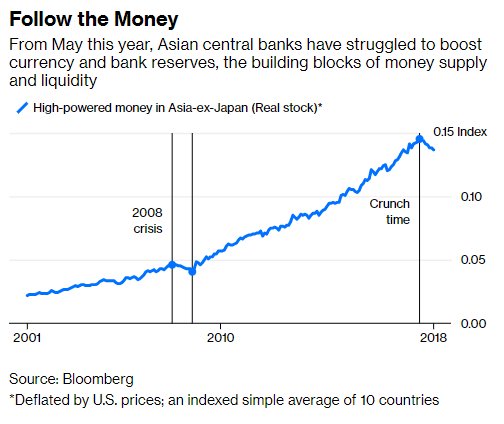

#Asia’s Liquidity Squeeze Is the Worst Since 2008 - Bloomberg

*Ex-Japan, central banks’ supply of currency plus bank reserves has ⬇ 7% in real terms since April.

*This is the steepest ⬇ in base money since the 11% ⬇ between Jan. and Oct. of 2008.

*Link: bloom.bg/2P55OGd

*Ex-Japan, central banks’ supply of currency plus bank reserves has ⬇ 7% in real terms since April.

*This is the steepest ⬇ in base money since the 11% ⬇ between Jan. and Oct. of 2008.

*Link: bloom.bg/2P55OGd

As I have repeated almost each week since July:

*DRAGHI: WORLD TRADE GROWTH MOMENTUM HAS SLOWED 'CONSIDERABLY' - BBG

*DRAGHI: WORLD TRADE GROWTH MOMENTUM HAS SLOWED 'CONSIDERABLY' - BBG

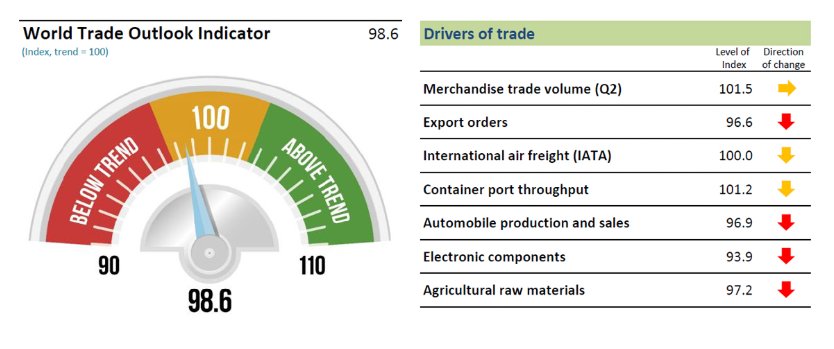

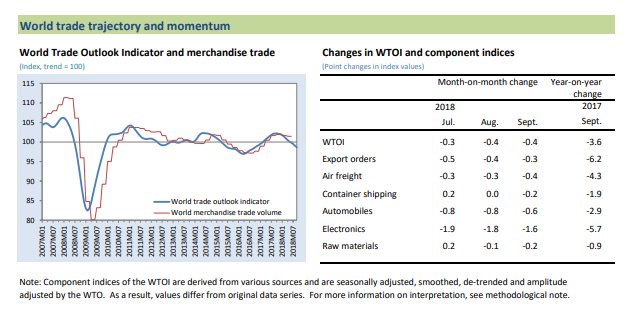

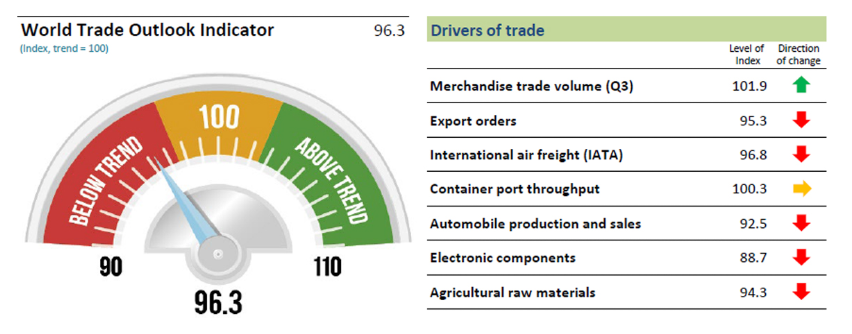

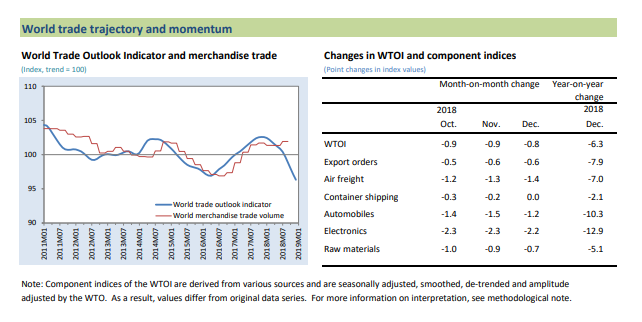

#WTO REPORT: #TRADE GROWTH TO WEAKEN FURTHER IN Q4

*The most recent WTOI reading of 98.6 is the lowest since October 2016 and reflects declines in all component indices.

*Link: bit.ly/2TGANf0

*The most recent WTOI reading of 98.6 is the lowest since October 2016 and reflects declines in all component indices.

*Link: bit.ly/2TGANf0

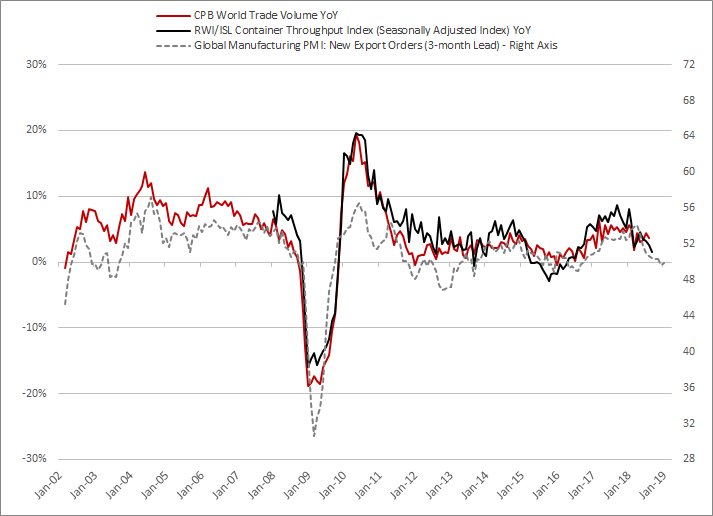

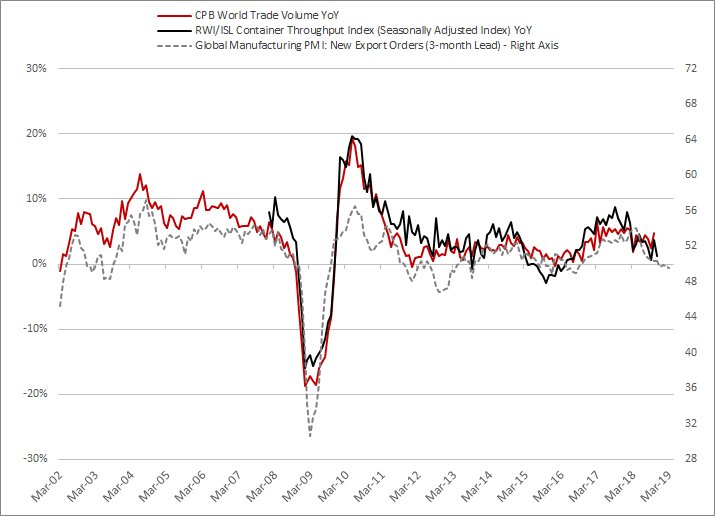

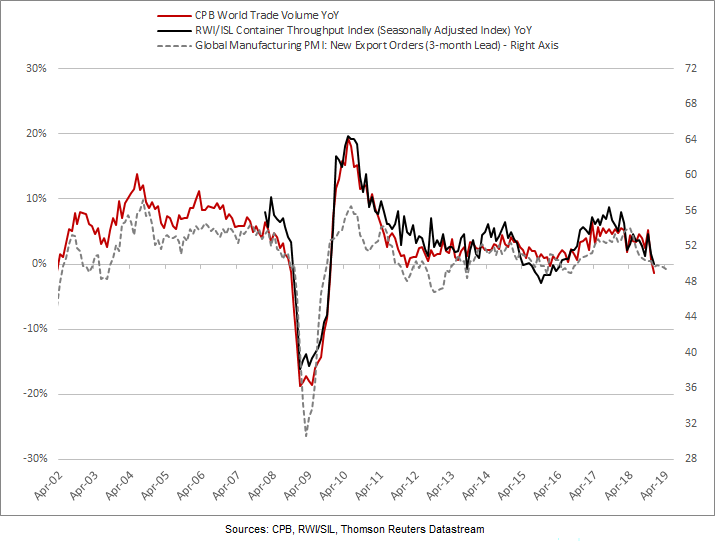

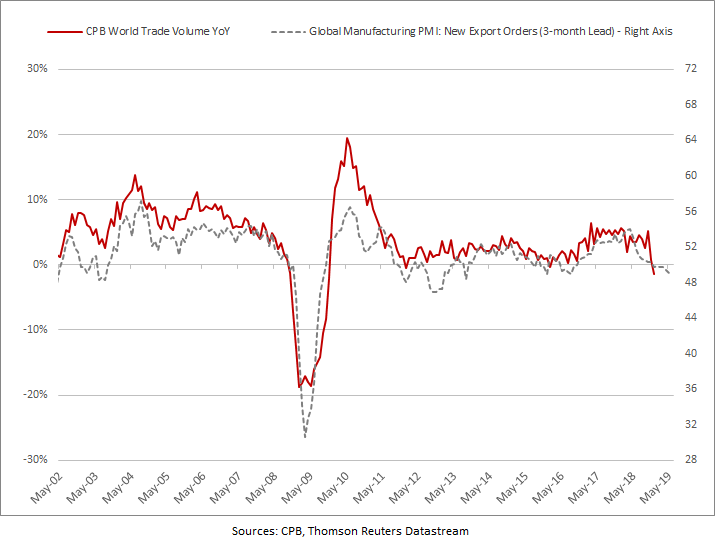

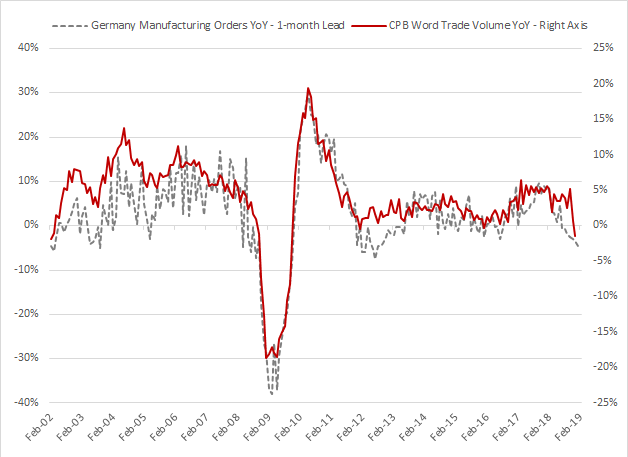

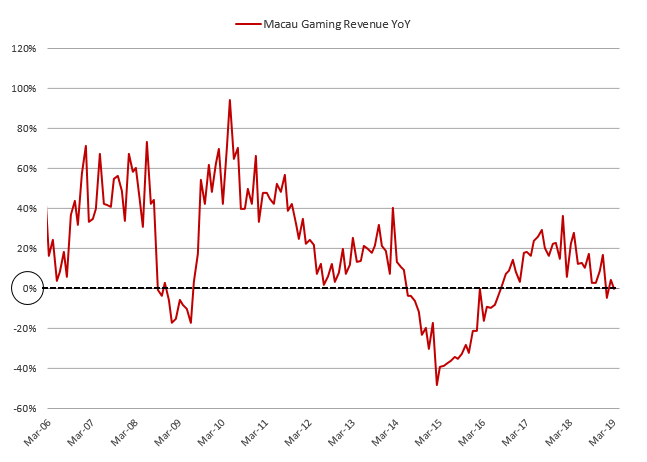

Latest CPB data (Sept.) confirmed that global trade growth kept slowing in 3Q.

*Figures also suggest that the consensus is too much optimistic for 2018 and especially 2019.

*Link: bit.ly/2rJjz2d

*Figures also suggest that the consensus is too much optimistic for 2018 and especially 2019.

*Link: bit.ly/2rJjz2d

🇺🇸 🇨🇳 In case they don't manage to find a framework/temporary deal (tariffs on hold), I will cut immediately my Global GDP forecast for next year (below my current estimate of 3.5%).

*It also means that the #Fed pause can take place sooner than I expect.

*It also means that the #Fed pause can take place sooner than I expect.

🇪🇺 Latest data related to consumer confidence were disappointing and suggests that Eurozone GDP is likely to remain muted in 4Q

🇩🇪 Dec. (18-month low)

🇮🇹 Nov. (6-month low)

🇫🇷 Nov. (45-month low)

➡ #ECB will revise downward (again) its GDP forecasts (2018/2019) at next meeting

🇩🇪 Dec. (18-month low)

🇮🇹 Nov. (6-month low)

🇫🇷 Nov. (45-month low)

➡ #ECB will revise downward (again) its GDP forecasts (2018/2019) at next meeting

Global Economy May Be Slowing More Than Expected, Lagarde Says - Bloomberg

*In a report ahead of the #G20, the IMF noted that recent data suggest greater slowdown than thought last month.

*Link: bloom.bg/2rbzbgo

*In a report ahead of the #G20, the IMF noted that recent data suggest greater slowdown than thought last month.

*Link: bloom.bg/2rbzbgo

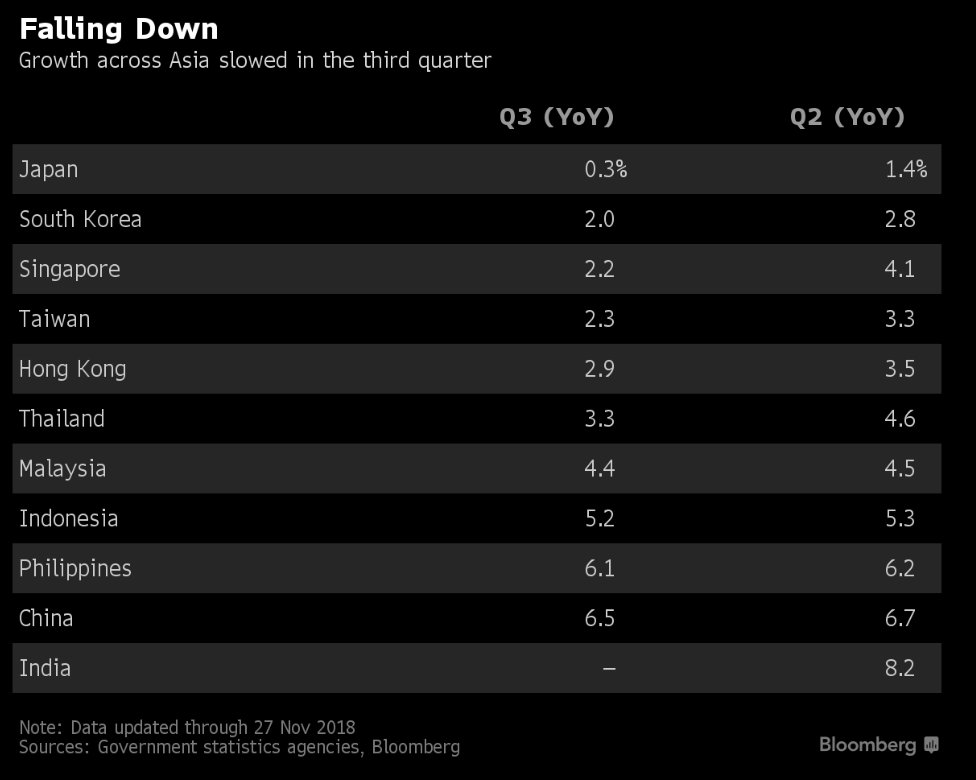

#Asia's Growth Is Shifting Down a Gear - Bloomberg

*Growth in #China, #Japan, Southeast #Asia was weaker last quarter

*Link: bloom.bg/2SoKopB

*Growth in #China, #Japan, Southeast #Asia was weaker last quarter

*Link: bloom.bg/2SoKopB

🇨🇳 #CHINA NOV #MANUFACTURING PMI: 50.0 V 50.2E (lowest since July 2016); NON-MANUFACTURING: 53.4 V 53.8E (lowest since Aug. 2017)

*Link: bloom.bg/2Q2dVsr

*Link: bloom.bg/2Q2dVsr

🇨🇳 #CHINA NOV #MANUFACTURING PMI (1):

*The weakness was largely driven by domestic factors, reflected by ⬇ in the sub-components for imports (-0.5 to 47.1), new orders (-0.4 to 50.4) and output (-0.1 to 51.9).

*The weakness was largely driven by domestic factors, reflected by ⬇ in the sub-components for imports (-0.5 to 47.1), new orders (-0.4 to 50.4) and output (-0.1 to 51.9).

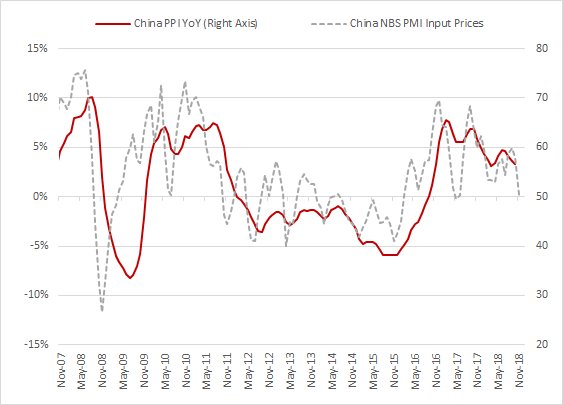

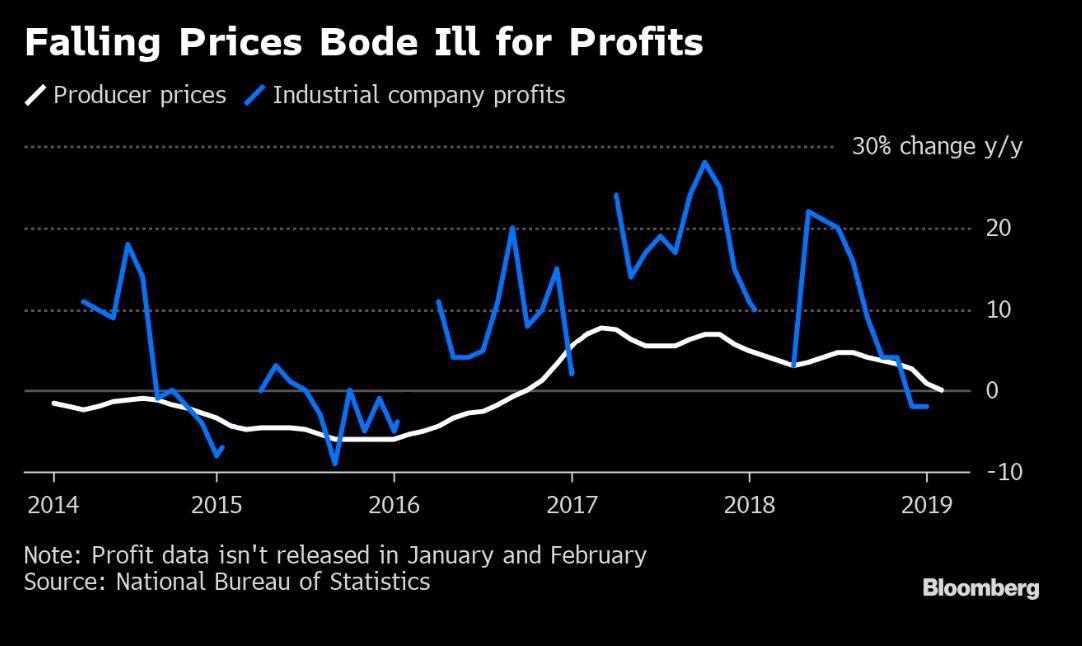

🇨🇳 #CHINA NOV #MANUFACTURING PMI (2): Sharp ⬇ in prices were reported.

*Significant ⬇ in commodity prices weighted on input price index (-7.7 to 50.3) while output price index also fell (-5.6 to 46.4).

*The drop in input price index suggests that PPI YoY will slow.

*Significant ⬇ in commodity prices weighted on input price index (-7.7 to 50.3) while output price index also fell (-5.6 to 46.4).

*The drop in input price index suggests that PPI YoY will slow.

🇨🇳 #CHINA NOV #MANUFACTURING PMI (3): Other figures suggest that trade growth will remain under pressure.

*Indexes for imports (-0.5 to 47.1) and new export orders (+0.3 to 47.0) remained in contraction territory.

*Indexes for imports (-0.5 to 47.1) and new export orders (+0.3 to 47.0) remained in contraction territory.

#IMF LAGARDE TOLD LEADERS THAT GLOBAL GROWTH MODERATING, MORE UNEVEN - BBG

*LAGARDE: TRADE TENSIONS HAVING NEGATIVE IMPACT

*Link: bit.ly/2PdZw79

*LAGARDE: TRADE TENSIONS HAVING NEGATIVE IMPACT

*Link: bit.ly/2PdZw79

🇨🇳 #CHINA NOV CAIXIN PMI #MANUFACTURING: 50.2 V 50.1E

*New export orders 47.7 v 48.8 prior ❗

➡ Contrary to the official PMI, the survey highlights more external weakness.

*Link: bit.ly/2BNmTRe

*New export orders 47.7 v 48.8 prior ❗

➡ Contrary to the official PMI, the survey highlights more external weakness.

*Link: bit.ly/2BNmTRe

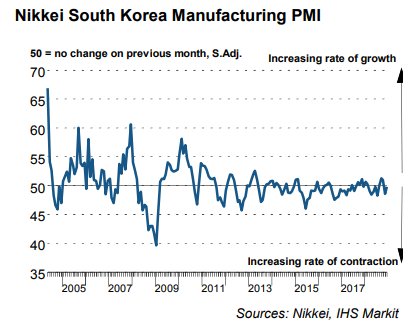

🇰🇷 🇹🇼🇨🇳 🇺🇸 #SouthKorea and #Taiwan took a dive in November as slowing #smartphone demand and U.S.-#China #trade tensions hit home.

*#Manufacturing PMIs:

- SK: 48.6 (4-month low) v 51.0 prior

- TW: 48.4 (lowest since October 2015) v 48.7 prior

*#Manufacturing PMIs:

- SK: 48.6 (4-month low) v 51.0 prior

- TW: 48.4 (lowest since October 2015) v 48.7 prior

🇺🇸 🇨🇳 The readings show how the U.S./#China #tradewar is reverberating through the region’s integrated #technology supply chain, pressuring #manufacturing hubs.

Global #Manufacturing PMI: New Exports Orders fell slightly in Nov. (-0.1pt to 49.8) and remained in contraction territory for the 3rd straight month.

*Even if global trade growth YoY should rebound in Oct., then a normalization ⬇ is very likely.

*Link: bit.ly/2AYe4CT

*Even if global trade growth YoY should rebound in Oct., then a normalization ⬇ is very likely.

*Link: bit.ly/2AYe4CT

🇨🇳 #China’s Nov. trade data were weak with exports ⬆ 5.4% YoY (8-month low; vs +15.6% prior) and imports ⬆ 3.0% YoY (47-month low; vs +21.4% prior)

*Slowdown was partly due to unfavorable base effects, ⬇ oil prices

*Shipments to most regions slowed reflecting ⬇ global demand

*Slowdown was partly due to unfavorable base effects, ⬇ oil prices

*Shipments to most regions slowed reflecting ⬇ global demand

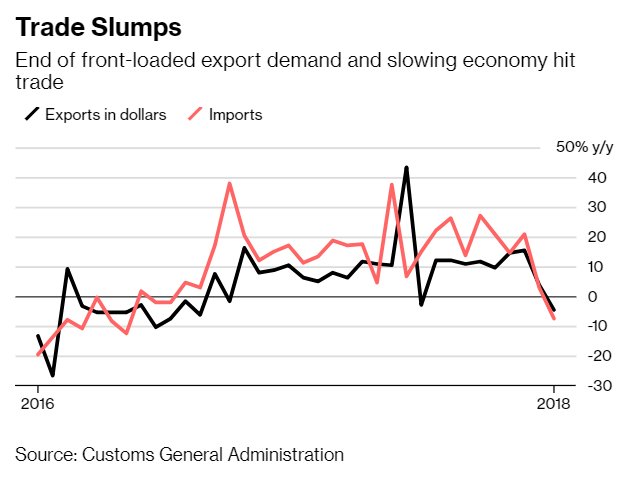

🇨🇳 Exports to the 🇺🇸 suggest fading frontloading with products hit by tariffs confirming slowdown.

*However that outperformed exports to other areas with shipments to the EU, Asean, Japan all slowing markedly.

*Weakness in imports also reflects sluggish domestic activity

*However that outperformed exports to other areas with shipments to the EU, Asean, Japan all slowing markedly.

*Weakness in imports also reflects sluggish domestic activity

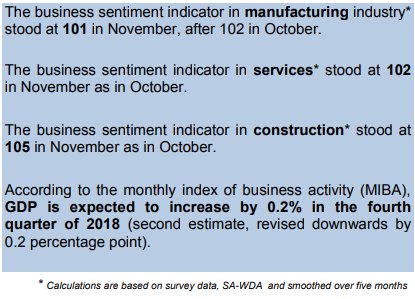

🇫🇷 Bank of #France cuts Q4 GDP forecast from 0.4% to 0.2%

*Link: bit.ly/2zTNGKt

*It reinforces my view that Eurozone 2018 GDP will be lower than the consensus expects.

*The #ECB will revise ⬇ its 2018 forecast next week.

*Link: bit.ly/2zTNGKt

*It reinforces my view that Eurozone 2018 GDP will be lower than the consensus expects.

*The #ECB will revise ⬇ its 2018 forecast next week.

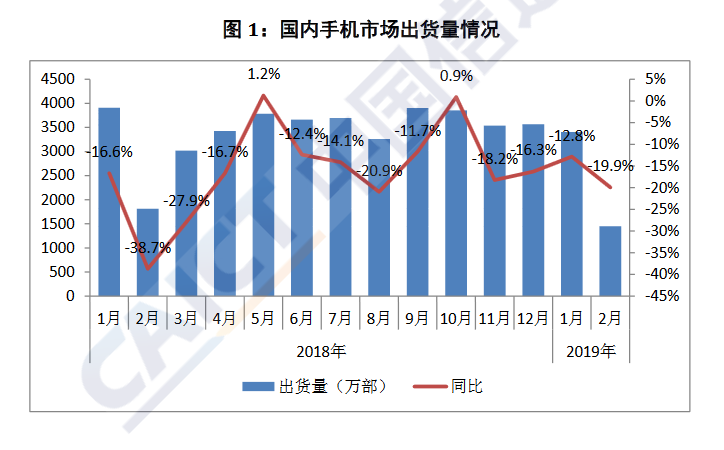

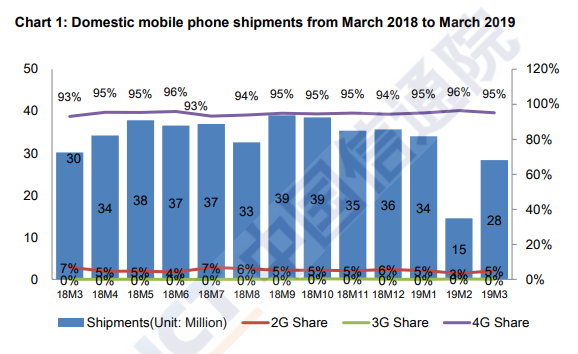

🇨🇳 #China Nov. Mobile Phone Shipments Drop 18% YoY - Academy of Information and Communications Technology

*Mobile phone shipments fell 8% MoM to 35.4m units in Nov.

*4G phone shipments down 17% YoY to 33.6m units

*39 new phone models were introduced in Nov., down 49% on year

*Mobile phone shipments fell 8% MoM to 35.4m units in Nov.

*4G phone shipments down 17% YoY to 33.6m units

*39 new phone models were introduced in Nov., down 49% on year

🇨🇳 #CHINA NOV. RETAIL PASSENGER VEHICLE SALES -18% ON YEAR: PCA - BBG

*CHINA NOV. RETAIL PASSENGER VEHICLE SALES 2.05M UNITS

*CHINA NOV. RETAIL PASSENGER VEHICLE SALES 2.05M UNITS

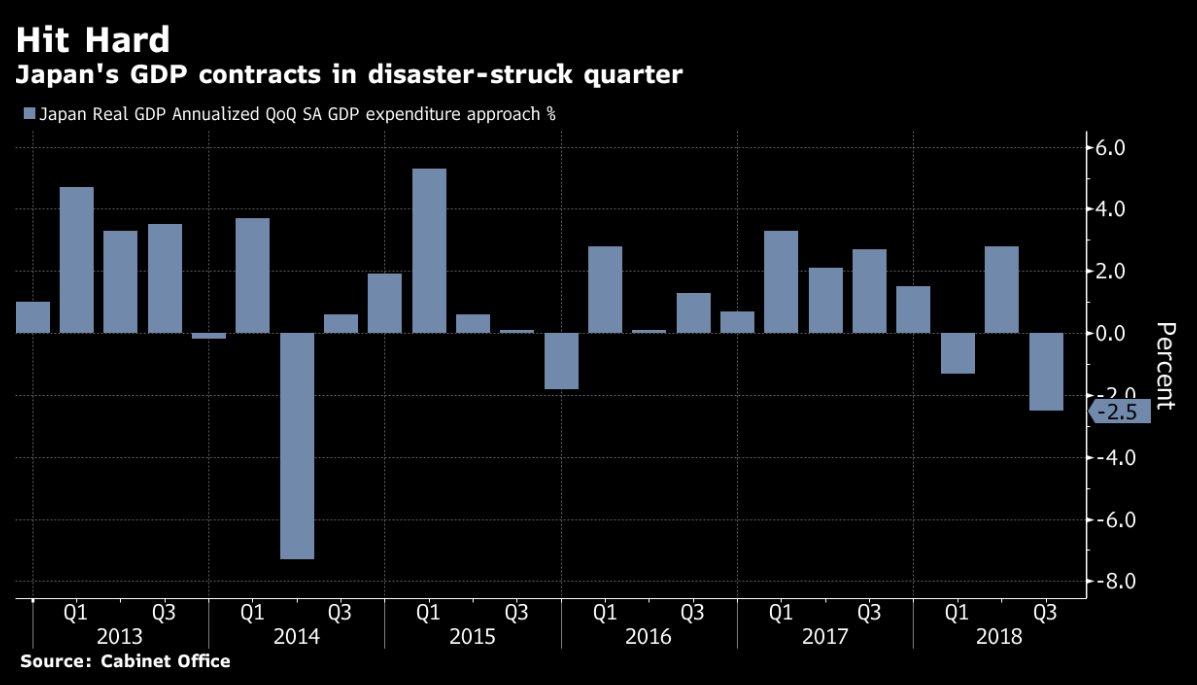

🇯🇵 #Japan Economy Shrinks Worse-Than-Forecast 2.5% on Capex Fall - Bloomberg

*Business investment slumps by the most in nine years

*Link: bloom.bg/2G5Vhej

➡ Figures reinforce my view that Japanese 2018 GDP will be lower than the consensus expects (+1.0%e).

*Business investment slumps by the most in nine years

*Link: bloom.bg/2G5Vhej

➡ Figures reinforce my view that Japanese 2018 GDP will be lower than the consensus expects (+1.0%e).

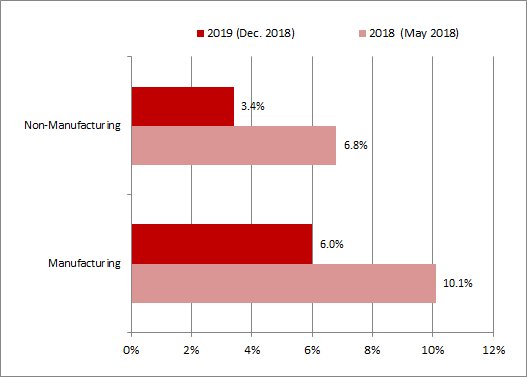

🇺🇸 The ISM’s semi-annual survey showed purchasing managers see capital spending:

⬆ 6.0% in 2019 in manufacturing (below the 10.1% projection made for 2018 in May)

⬆ 3.4% in 2019 in services (below the 6.8% projection made for 2018 in May)

*Lin: bit.ly/2hf9khA

⬆ 6.0% in 2019 in manufacturing (below the 10.1% projection made for 2018 in May)

⬆ 3.4% in 2019 in services (below the 6.8% projection made for 2018 in May)

*Lin: bit.ly/2hf9khA

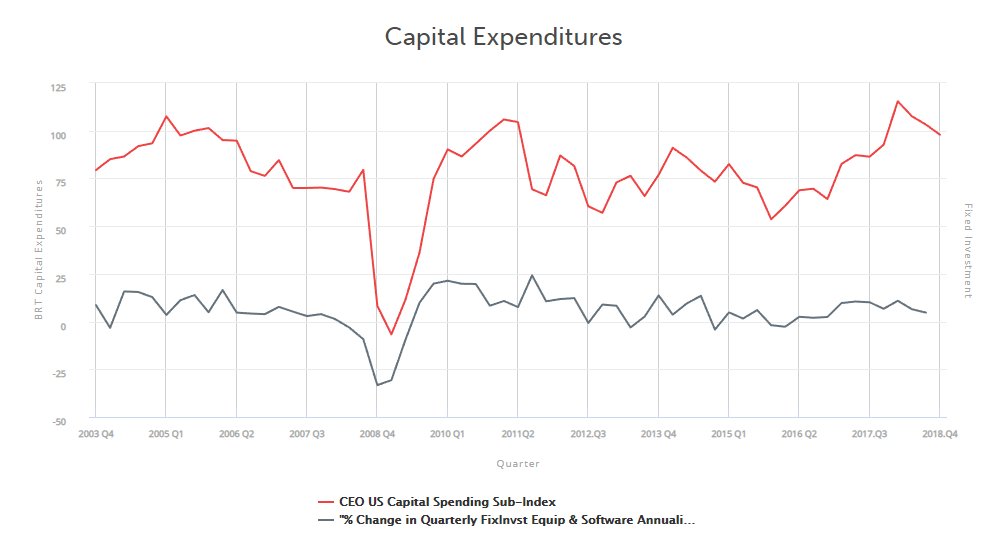

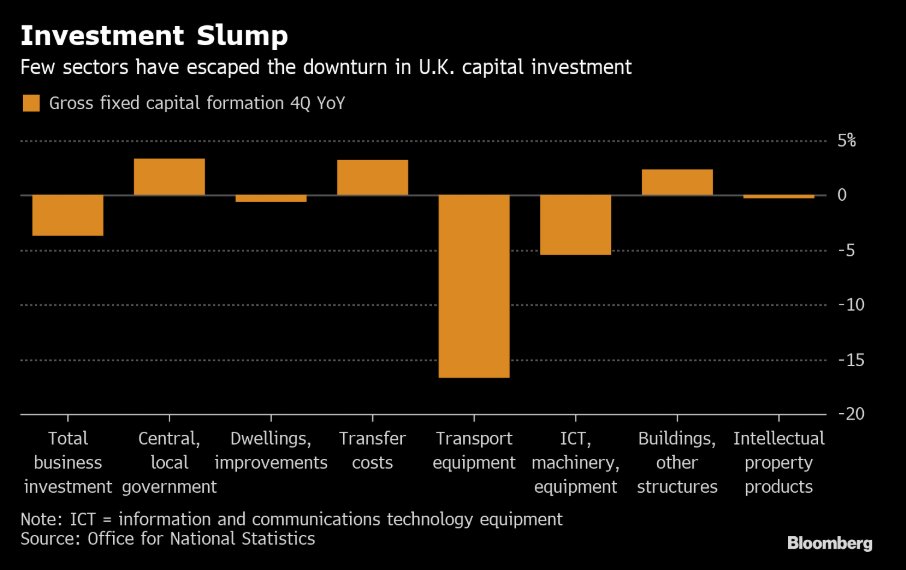

🇺🇸 The Business Roundtable survey (4Q18) showed that sentiment among US corporate leaders declined for the third straight quarter.

*Plans for capital investment and hiring and sales expectations all declined compared with the prior quarter.

*Link: bit.ly/2rxqJrY

*Plans for capital investment and hiring and sales expectations all declined compared with the prior quarter.

*Link: bit.ly/2rxqJrY

🇺🇸 The latest CNBC/SurveyMonkey Small Business Survey showed that after five straight quarters of gains, those who say conditions for business are currently "good" dipped from 58% to 55% in 4Q18.

cnbc.com/2018/12/10/cnb…

cnbc.com/2018/12/10/cnb…

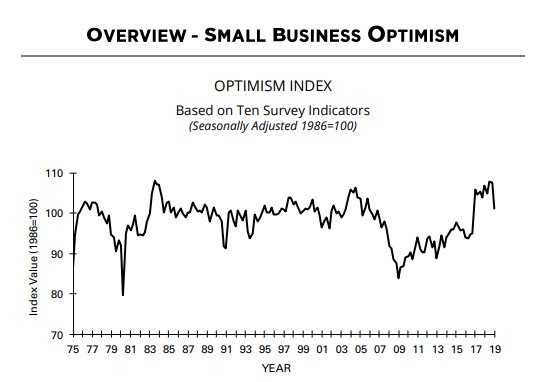

🇺🇸 The net share of companies expecting the economy to improve in 6 months dropped in November to a two-year low of 22% (vs 33% prior) - NFIB

*Small business optimism: 104.8 (lowest since April 2018) vs 107.4 prior

*Link: bit.ly/Lg4Ndz

*Small business optimism: 104.8 (lowest since April 2018) vs 107.4 prior

*Link: bit.ly/Lg4Ndz

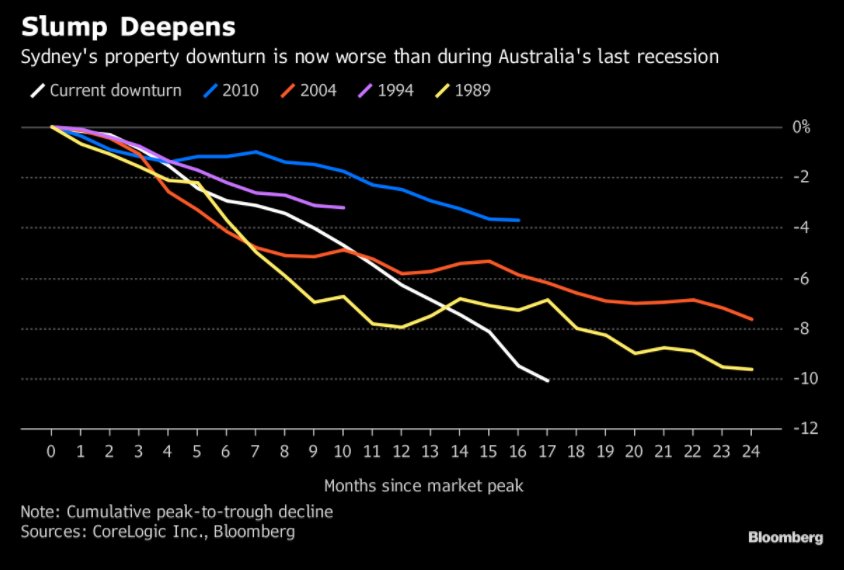

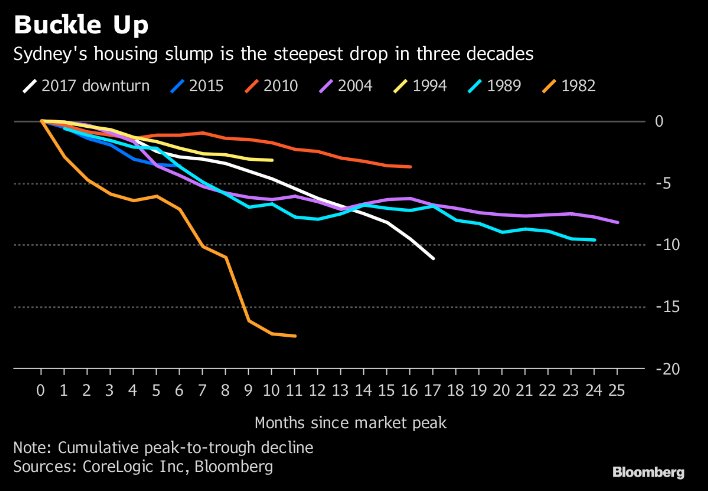

🇦🇺 #Australia | #Sydney’s property market ⬇ has reached a new milestone, with values falling further than the late 1980s - Bloomberg

*Home values ⬇ 10.1% since their 2017 peak, surpassing the top-to-bottom ⬇ of 9.6% recorded between 1989 and 1991

*Link: bloom.bg/2L9WRe4

*Home values ⬇ 10.1% since their 2017 peak, surpassing the top-to-bottom ⬇ of 9.6% recorded between 1989 and 1991

*Link: bloom.bg/2L9WRe4

🇪🇺 #EUROZONE DEC PRELIMINARY MANUFACTURING PMI: 51.4 V 51.8E (34-month low)

*Services PMI: 51.4 v 53.4e (49-month low)

*Composite PMI: 51.3 v 52.8e (49-month low)

*Link: bit.ly/2zZAwf8

*Services PMI: 51.4 v 53.4e (49-month low)

*Composite PMI: 51.3 v 52.8e (49-month low)

*Link: bit.ly/2zZAwf8

🇪🇺 #EUROZONE PMIs: "New export orders (which include intra-eurozone trade) fell for the third successive month, recording the steepest decline since the series began over four years ago". ❗

🇪🇺 As a reminder, as expected (bit.ly/2QwonID), yesterday, the #ECB cut its GDP forecasts for:

*2018 (from 2.0% to 1.9%)

*2019 (from 1.8% to 1.7%)

*Link: bit.ly/2QB33SE

➡ 2018f is now in line with my view but 2019f looks a bit optimistic

*2018 (from 2.0% to 1.9%)

*2019 (from 1.8% to 1.7%)

*Link: bit.ly/2QB33SE

➡ 2018f is now in line with my view but 2019f looks a bit optimistic

🇨🇳 #China sparks suspicion as it holds release of statistics - Nikkei

*Concealment added to whispers that Beijing doctors figures

asia.nikkei.com/Economy/China-…

*Concealment added to whispers that Beijing doctors figures

asia.nikkei.com/Economy/China-…

🇨🇳 #China | As an example, the article highlighted the Guandong PMI was not published on its 1-Nov scheduled date. Analysts speculated that it was because Guandong is highly geared towards exports to Europe and the US.

🇨🇳 #China | Yesterday, Central Bank Governor Yi Gang noted that there is increasing downward pressure on the economy which was confirmed by stats this morning:

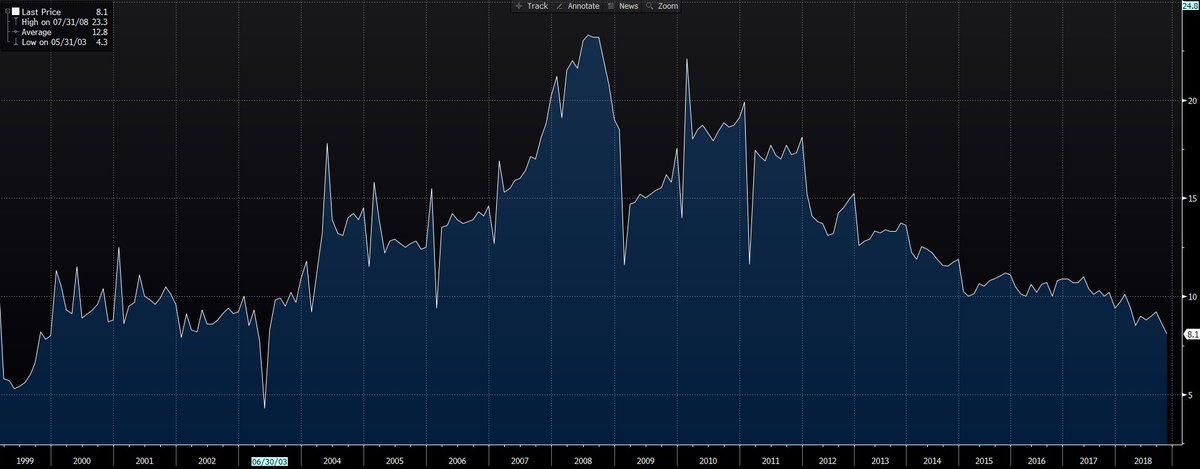

➡ Growth in retail sales slowed to +8.1% YoY in Nov. (the weakest reading since June 2003)

➡ Growth in retail sales slowed to +8.1% YoY in Nov. (the weakest reading since June 2003)

🇪🇺 Some #ECB policymakers wanted even more cautious tone on economy - sources - Reuters

uk.reuters.com/article/uk-ecb…

uk.reuters.com/article/uk-ecb…

🇯🇵 #Japan trims 2019 growth forecast to 1.3% (from 1.5% prior) - Nikkei

asia.nikkei.com/Economy/Japan-…

asia.nikkei.com/Economy/Japan-…

🇰🇷 #SouthKorea 's economy to grow 2.6 pct-2.7 pct in 2019 (down from 2.9% prior): gov't - Yonhap

en.yna.co.kr/view/AEN201812…

en.yna.co.kr/view/AEN201812…

🇺🇸 Americans Turn More Pessimistic on Economy, Trump Approval Down - Bloomberg

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

Recent market 'jolt' will be first of many as easy money era ends, says BIS - Reuters

reuters.com/article/us-bis…

reuters.com/article/us-bis…

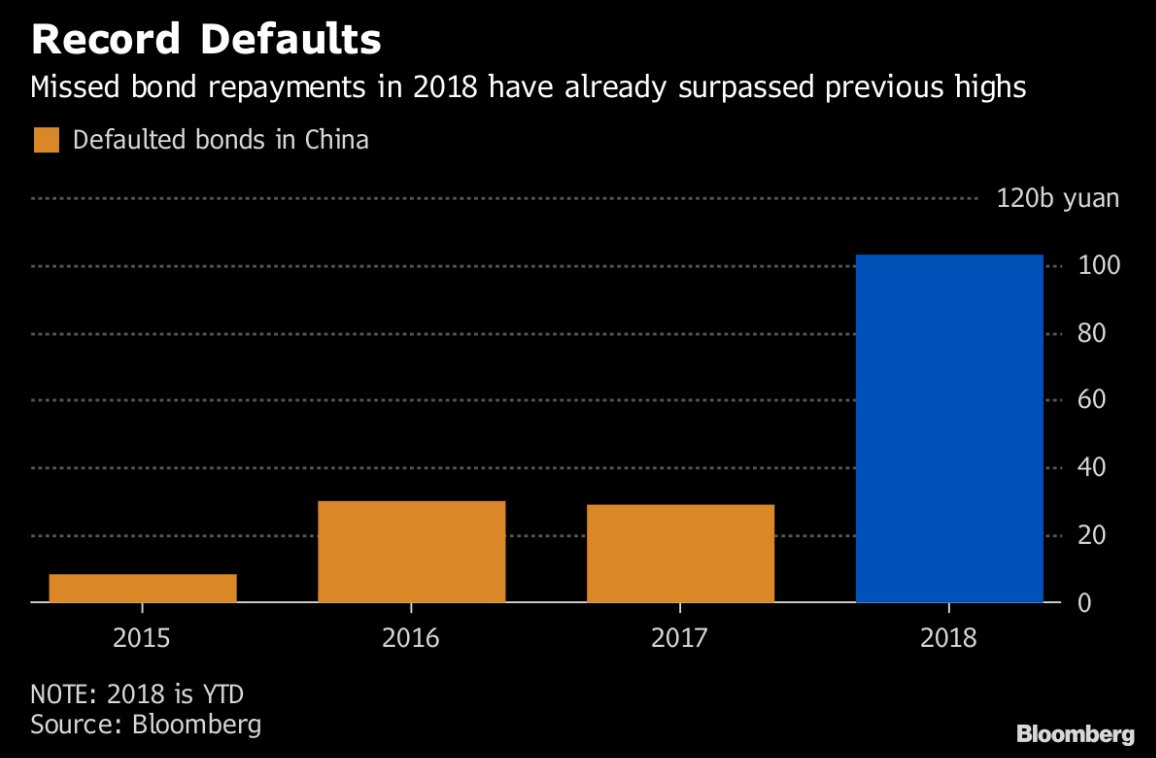

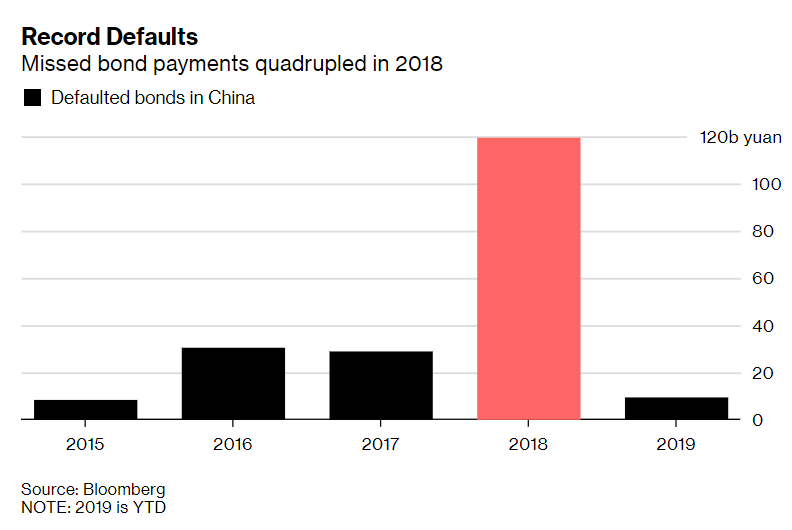

🇨🇳 #China Sees Bankruptcies Surge; Bondholders May Get Less Back - Bloomberg

*Missed bond payments in 2018 have almost quadrupled the tally last year

*Link: bloom.bg/2QDU6YH

*Missed bond payments in 2018 have almost quadrupled the tally last year

*Link: bloom.bg/2QDU6YH

As expected | 🇩🇪 #Germany’s dominant car industry may take longer than feared to recover from a slump, weighing on growth in the euro zone’s biggest economy, the Bundesbank said in a monthly economic report on Monday - Reuters

in.reuters.com/article/us-ger…

in.reuters.com/article/us-ger…

🇨🇳 As trade war bites, #China advisers recommend lowering 2019 growth target - Reuters

reuters.com/article/us-chi…

reuters.com/article/us-chi…

🇨🇳 Chinese President Xi Jinping said on Tuesday that #China's reforms and opening up are not easy, and could face unimaginable storms - Reuters

uk.reuters.com/article/uk-chi…

uk.reuters.com/article/uk-chi…

🇨🇳 #China Inc. to Suffer More Defaults in 2019 as Profits Stall - Bloomberg

*Energy sector leads China’s record local bond default in 2018

*Private firms will face increasing liquidity pressure: S&P

*Link: bloom.bg/2Civxrs

*Energy sector leads China’s record local bond default in 2018

*Private firms will face increasing liquidity pressure: S&P

*Link: bloom.bg/2Civxrs

🇯🇵 #Japan | In line with Nikkei discussion (bit.ly/2QF79ZK), the government revised ⬇ its forecasts for:

*FY18 to 0.9% (vs 1.5% prior)

*FY19 to 1.3% (vs 1.5% prior)

➡ Both still look optimistic.

reuters.com/article/us-jap…

*FY18 to 0.9% (vs 1.5% prior)

*FY19 to 1.3% (vs 1.5% prior)

➡ Both still look optimistic.

reuters.com/article/us-jap…

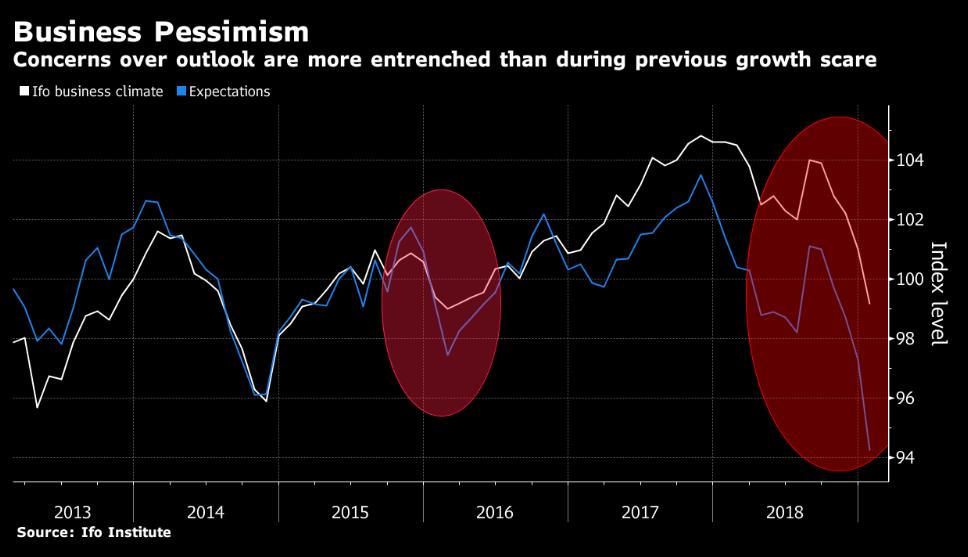

🇩🇪 #GERMANY DEC IFO BUSINESS CLIMATE: 101.0 V 101.7E (lowest since Sept. 2016); CURRENT ASSESSMENT: 104.7 V 105.0E (lowest since June 2017)

- Expectations Survey: 97.3 v 98.3e (lowest since Nov. 2014)

- Expectations Survey: 97.3 v 98.3e (lowest since Nov. 2014)

Meanwhile...

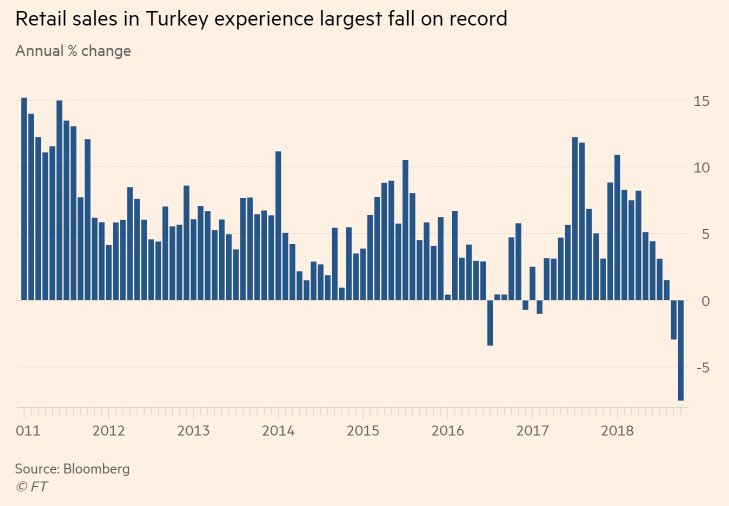

🇹🇷 #Turkey retail sales suffer worst drop on record - FT

*Sales volumes fell by 7.5% YoY in October, the sharpest decline since records began in 2010.

*It follows a 3% drop in Sept., the first annual contraction since Feb. 2017

*Link: on.ft.com/2A71tgR

🇹🇷 #Turkey retail sales suffer worst drop on record - FT

*Sales volumes fell by 7.5% YoY in October, the sharpest decline since records began in 2010.

*It follows a 3% drop in Sept., the first annual contraction since Feb. 2017

*Link: on.ft.com/2A71tgR

🇨🇳 #China | Xinhua reports the National Bureau of Statistics (NBS) said Guangdong Province has violated the law by surveying and publishing the local purchasing managers' index (PMI) with an expired license.

xinhuanet.com/english/2018-1…

xinhuanet.com/english/2018-1…

FedEx Corp. plunged as as a darkening view of demand for shipping services outside the U.S. prompted the company to slash its profit forecast and pare international air-freight capacity - Bloomberg

*Link: bloom.bg/2EEF7Hg

*Link: bloom.bg/2EEF7Hg

*The company noted that world trade slowed in Q3 to just +3.5% vs +5.3% in Q317 (bit.ly/2SbUrOU)

➡ As already discussed, my proxies pointed to more slowdown in the coming months.

➡ In detail, an uptick is very likely in Oct. before another sharp slowdown from Nov.

➡ As already discussed, my proxies pointed to more slowdown in the coming months.

➡ In detail, an uptick is very likely in Oct. before another sharp slowdown from Nov.

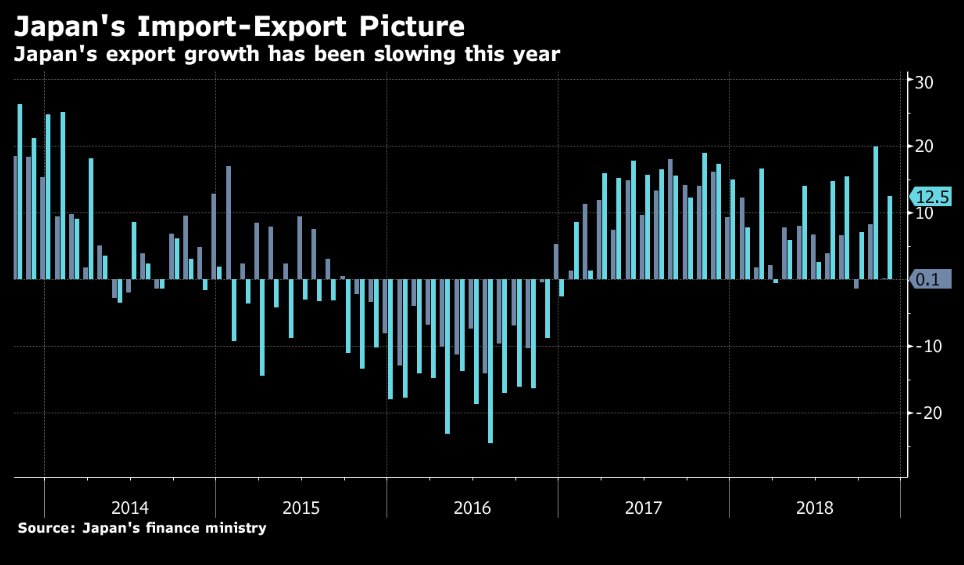

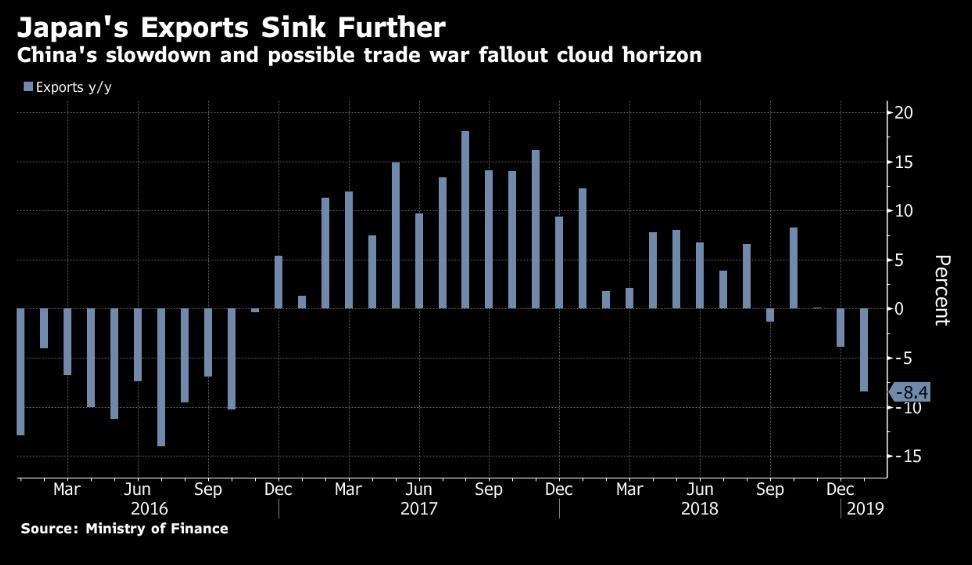

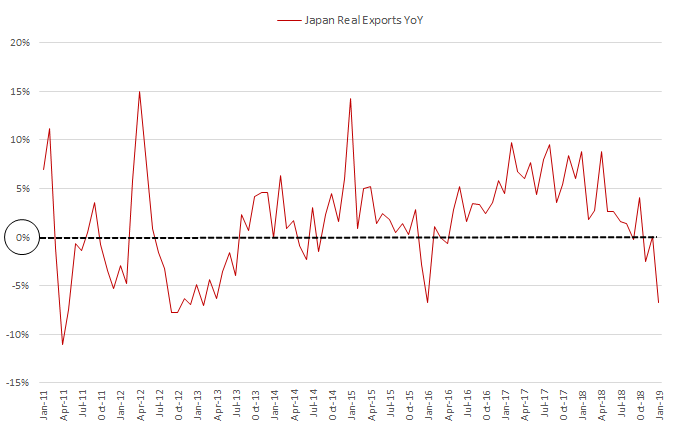

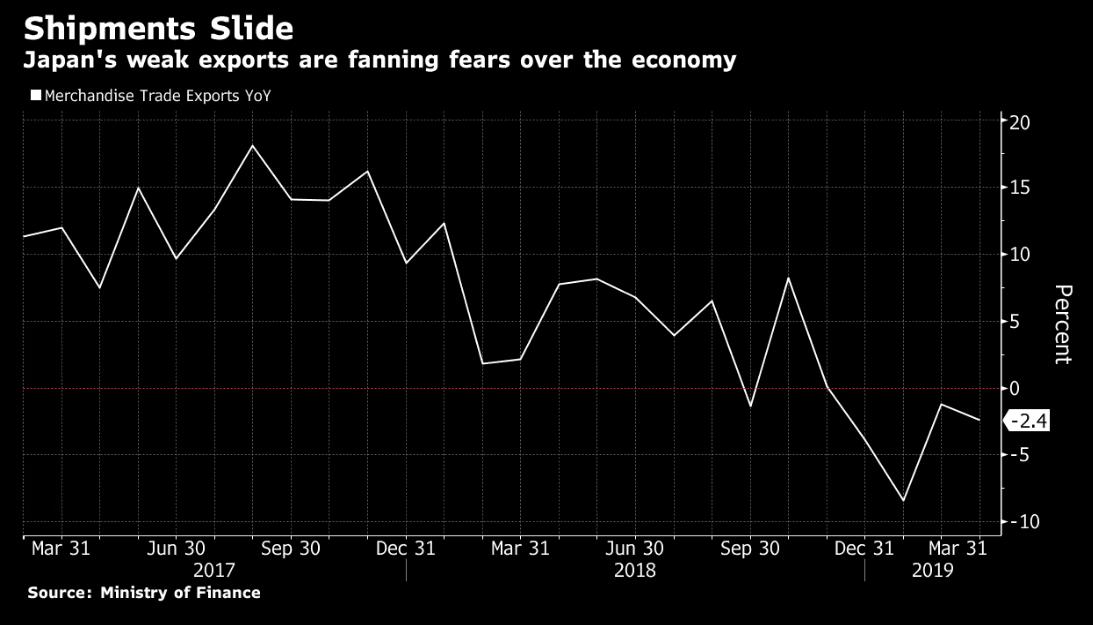

🇯🇵 #Japan November Exports YoY: 0.1% vs 8.2% prior

*Imports YoY: 12.5% vs 19.9% prior

*Real exports YoY: -2.4% vs +6.3% (largest ⬇ since Jan. 2016)

*Link: bit.ly/2EBb8QJ

*Imports YoY: 12.5% vs 19.9% prior

*Real exports YoY: -2.4% vs +6.3% (largest ⬇ since Jan. 2016)

*Link: bit.ly/2EBb8QJ

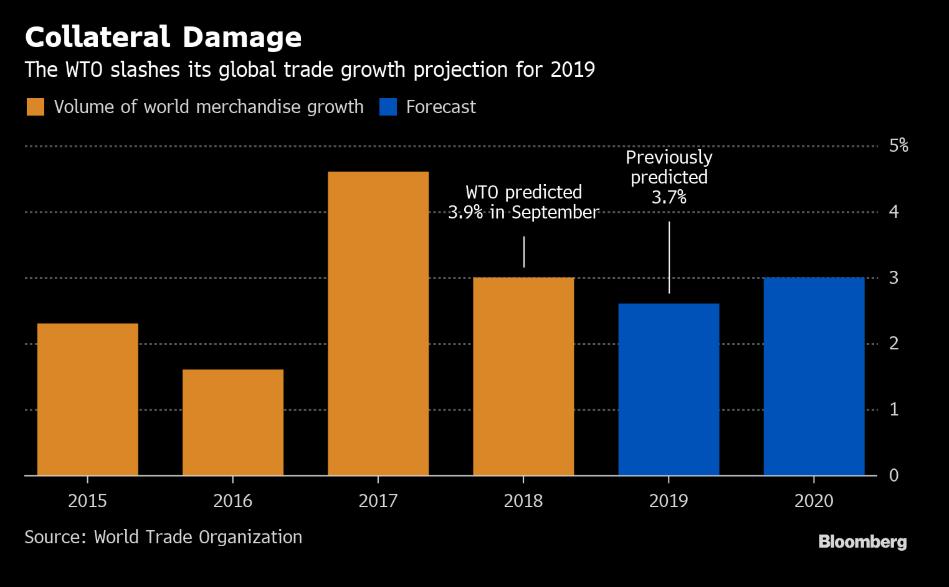

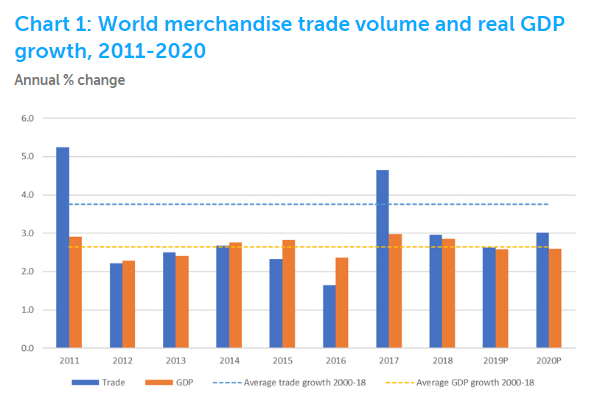

One of World Trade's Top Prognosticators Is Worried About 2019 - Bloomberg

*The WTO in Sept. ⬇ its forecast for global trade growth, predicting the volume of goods moving around the world would expand by 3.9% this year and slow to 3.7% in 2019.

bloomberg.com/news/articles/…

*The WTO in Sept. ⬇ its forecast for global trade growth, predicting the volume of goods moving around the world would expand by 3.9% this year and slow to 3.7% in 2019.

bloomberg.com/news/articles/…

Koopman said the organization was holding to those forecasts for now, though he added that risks were rising that they could be ⬇ again early next year.

➡ My proxies suggest that world trade growth is set to moderate to ~+3.5% in 2018 and <3% in 2019.

➡ My proxies suggest that world trade growth is set to moderate to ~+3.5% in 2018 and <3% in 2019.

🇰🇷 #SouthKorea | Trade data for the first 20 days of Dec. showed:

*a 1.0% YoY ⬆ in total exports (6-month low; vs +5.7% in Nov.)

*a 14.2% YoY ⬇ in exports to #China (largest ⬇ since October 2016 vs -4.1% in Nov.)

*Link: bit.ly/2Ac6GUJ

*a 1.0% YoY ⬆ in total exports (6-month low; vs +5.7% in Nov.)

*a 14.2% YoY ⬇ in exports to #China (largest ⬇ since October 2016 vs -4.1% in Nov.)

*Link: bit.ly/2Ac6GUJ

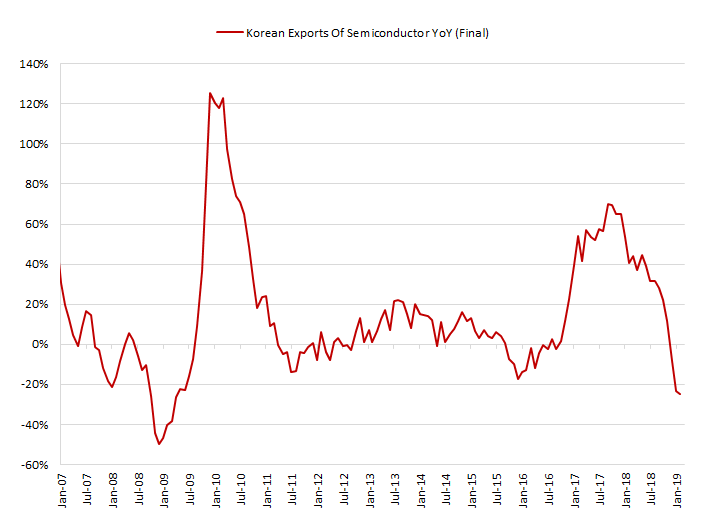

🇰🇷 | A contraction of semiconductor exports of 9.8% YoY (vs +3.5% in Nov.) also suggests a rapid softening of the global #tech sector, for which #SouthKorea is a key supplier.

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

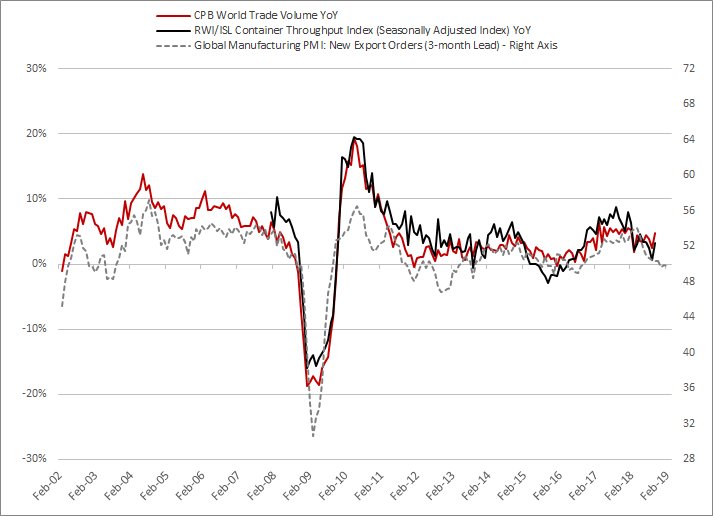

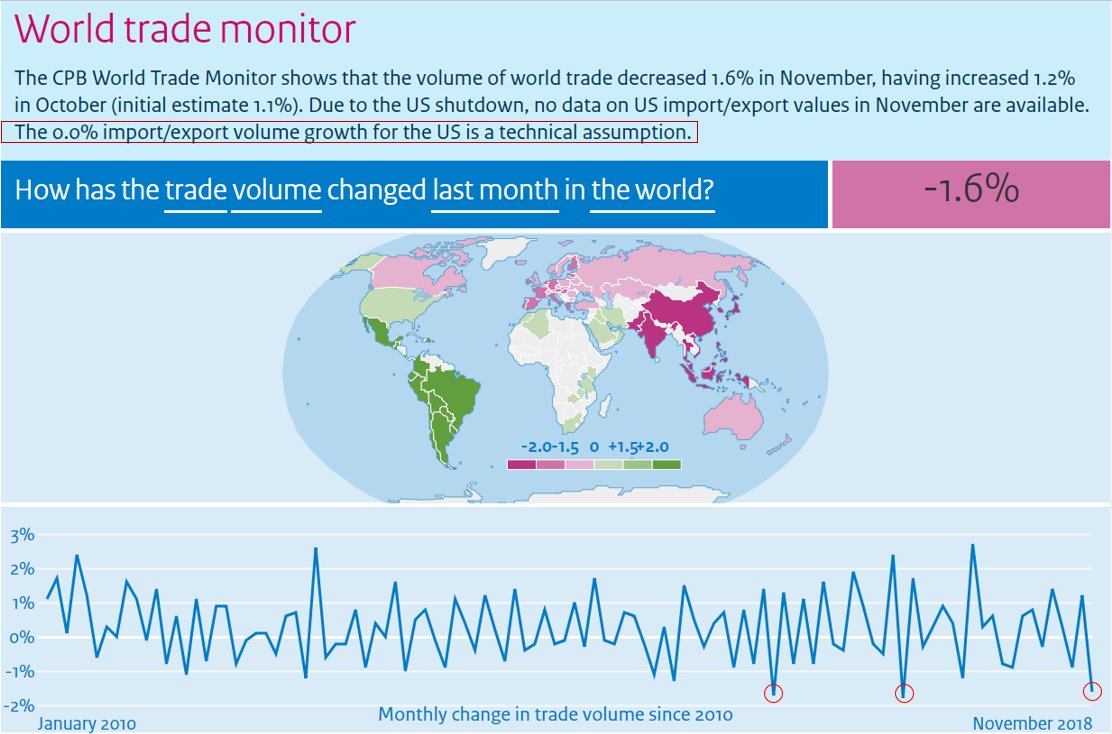

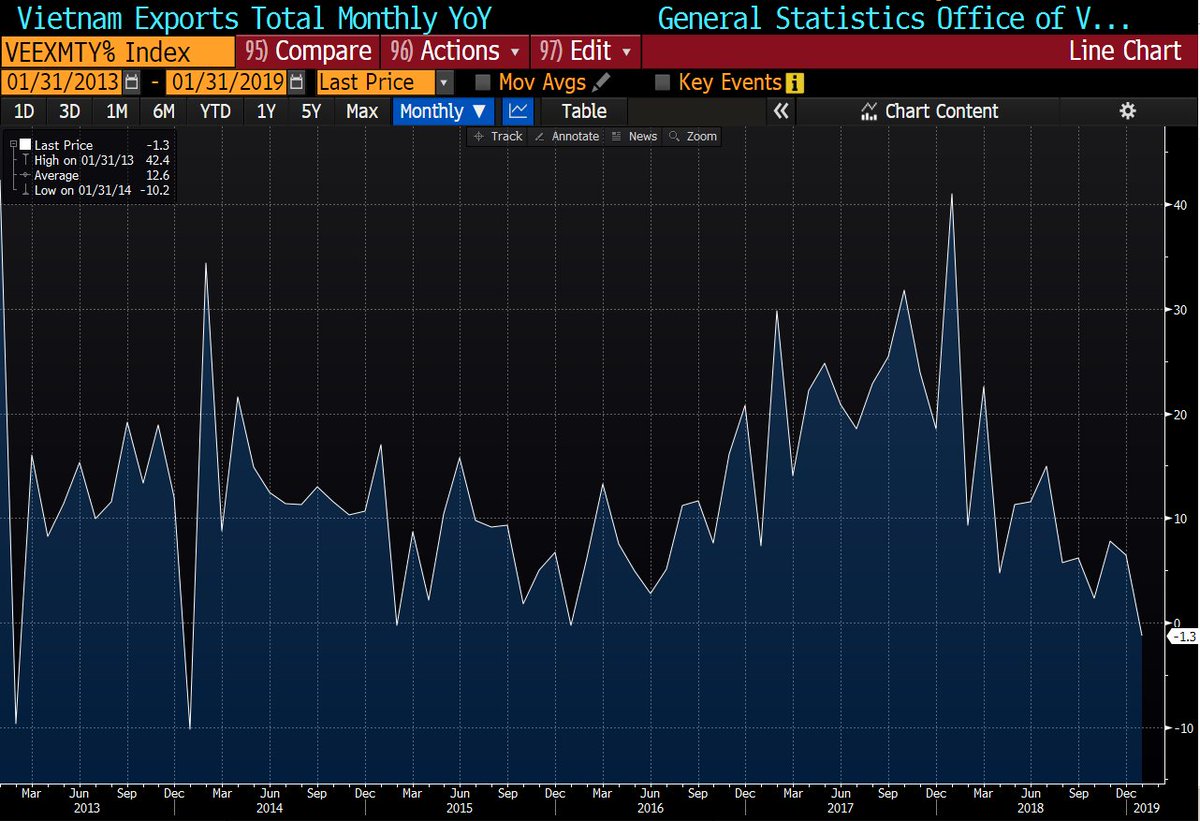

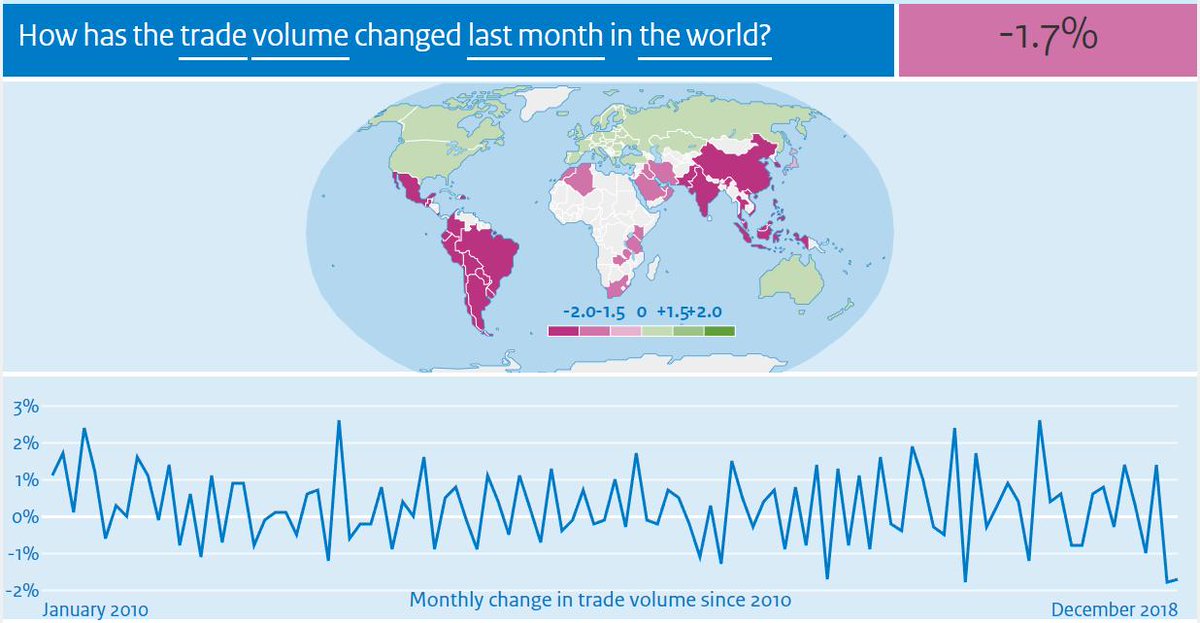

As expected (bit.ly/2CxCMf0), CPB data showed World trade growth (volume) ⬆ in Oct. (+4.7% YoY vs +2.5% YoY) due to front-loading and #Japan recovery

*Link: bit.ly/2T4KAum

➡ I still expect a sharp slowdown from Nov. amid ⬇ activity and negative base effect

*Link: bit.ly/2T4KAum

➡ I still expect a sharp slowdown from Nov. amid ⬇ activity and negative base effect

The acceleration seen in Oct. is larger than I expected, suggesting that world trade growth (in volume) should average [3.6%-3.7%] based on World Bank measure.

*It would be down from 4.8% in 2017 but up compared to my previous forecast for 2018 (~+3.5%).

*It would be down from 4.8% in 2017 but up compared to my previous forecast for 2018 (~+3.5%).

🇯🇵 🇨🇳 Japanese carmakers Nissan and Mazda will cut production in #China by 20% after the country’s new car market shrank in 2018 for the first time in 28 years - Nikkei

*Link (Japanese): nikkei.com/article/DGXMZO…

*Link (Japanese): nikkei.com/article/DGXMZO…

🇩🇪 #Germany | Almost 53 percent of so-called “Mittelstand” companies surveyed by the BVMW industry association fear that a recession could strike in the next 12 months, the group said Friday - Bloomberg

*Link: bloom.bg/2CD2uPh

*Link: bloom.bg/2CD2uPh

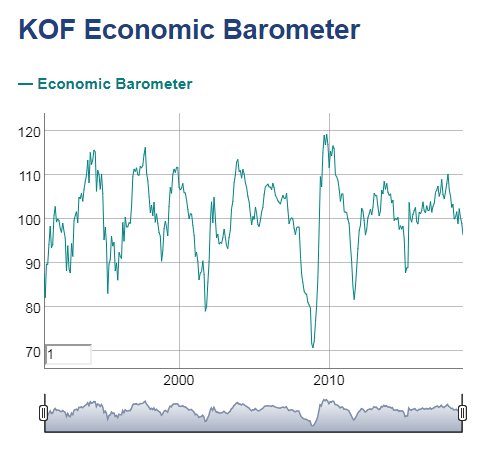

🇨🇭 In December, the KOF Economic Barometer fell by 2.6 pts to 96.3.

*More clearly than last month, the indicator lies below its long-term average.

*Link: bit.ly/2ETbTUz

*More clearly than last month, the indicator lies below its long-term average.

*Link: bit.ly/2ETbTUz

🇨🇳 #CHINA DEC #MANUFACTURING PMI: 49.4 V 50.0E (lowest since Feb 2016); NON-MANUFACTURING PMI: 53.8 V 53.2E (2-month high)

- COMPOSITE PMI: 52.6 V 52.8 PRIOR (record low since records began in Jan. 2017)

*Link: bloom.bg/2RnCRdH

- COMPOSITE PMI: 52.6 V 52.8 PRIOR (record low since records began in Jan. 2017)

*Link: bloom.bg/2RnCRdH

🇨🇳 #CHINA DEC #MANUFACTURING PMI (1):

- The weakness was driven by domestic factors, reflected by the ⬇ in the sub-components for:

*new orders (-0.7 to 49.7; 1st contraction since Feb. 2016)

*output (-1.1 to 50.8; 10-month low)

*imports (-1.2 to 45.9; lowest since Feb. 2016)

- The weakness was driven by domestic factors, reflected by the ⬇ in the sub-components for:

*new orders (-0.7 to 49.7; 1st contraction since Feb. 2016)

*output (-1.1 to 50.8; 10-month low)

*imports (-1.2 to 45.9; lowest since Feb. 2016)

🇨🇳 #CHINA DEC #MANUFACTURING PMI (2):

- The significant ⬇ in commodity prices weighted on input price index (-5.5 to 44.8; lowest since Nov. 2015) suggesting that:

*PPI YoY will ⬇

*Industrial profits will keep ⬇

- The significant ⬇ in commodity prices weighted on input price index (-5.5 to 44.8; lowest since Nov. 2015) suggesting that:

*PPI YoY will ⬇

*Industrial profits will keep ⬇

🇨🇳 #CHINA DEC #MANUFACTURING PMI (3):

- Other figures suggest that trade growth will remain under pressure:

*Indexes for imports (-1.2 to 45.9; lowest since Feb. 2016) and new export orders (-0.4 to 46.6; lowest since Nov. 2015) remained in contraction territory.

- Other figures suggest that trade growth will remain under pressure:

*Indexes for imports (-1.2 to 45.9; lowest since Feb. 2016) and new export orders (-0.4 to 46.6; lowest since Nov. 2015) remained in contraction territory.

🇨🇳 #CHINA DEC #MANUFACTURING PMI (4):

- Finally, the sub-component for business expectations tumbled 1.5 pts to 52.7. *While still a positive reading (>50), it was the lowest since January 2016.

- Finally, the sub-component for business expectations tumbled 1.5 pts to 52.7. *While still a positive reading (>50), it was the lowest since January 2016.

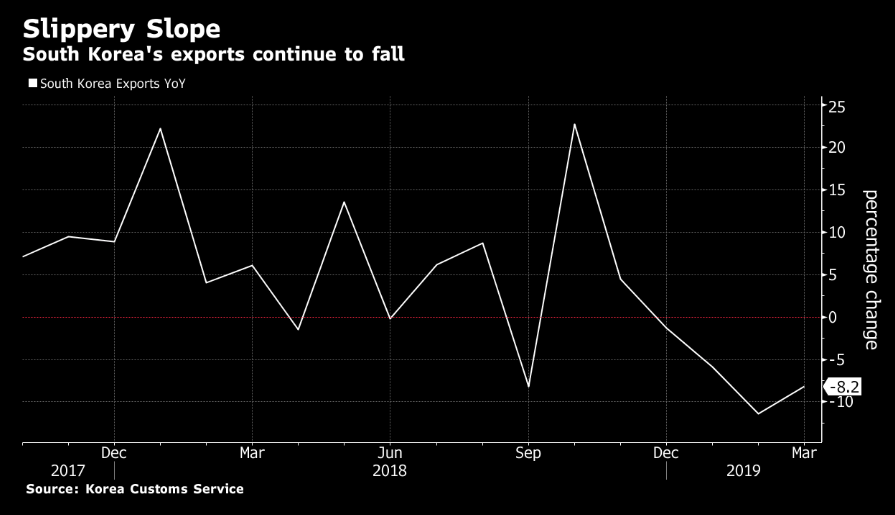

🇰🇷 #SouthKorea Dec Exports YoY: -1.2% (3-month low) v 2.5%e

*It was down from -1.0% in the first 20 days of Dec.

*Shipments of semiconductors, which dominate the country’s exports, fell 8.3% YoY (largest drop since April 2016).

bloomberg.com/news/articles/…

*It was down from -1.0% in the first 20 days of Dec.

*Shipments of semiconductors, which dominate the country’s exports, fell 8.3% YoY (largest drop since April 2016).

bloomberg.com/news/articles/…

🇨🇳 #CHINA DEC CAIXIN #MANUFACTURING PMI: 49.7 V 50.2E (first contraction since May 2017)

*New Orders index: 49.8 v 50.9 prior (first contraction since June 2016)

*New export orders ⬇for the 9th month in a row

*Link: bit.ly/2QeZRqI

*New Orders index: 49.8 v 50.9 prior (first contraction since June 2016)

*New export orders ⬇for the 9th month in a row

*Link: bit.ly/2QeZRqI

🇰🇷 🇹🇼 🇨🇳 🇺🇸 #SouthKorea and #Taiwan remained in contraction territory in Dec. as slowing #smartphone demand and U.S.-#China #trade tensions hit home.

*#Manufacturing PMIs:

- SK: 49.8 v 48.6 prior

- TW: 47.7 (lowest since September 2015) v 48.4 prior

*#Manufacturing PMIs:

- SK: 49.8 v 48.6 prior

- TW: 47.7 (lowest since September 2015) v 48.4 prior

🇰🇷 Focusing on #SouthKorea, export orders declined for the 5th consecutive month in Dec.

*Link: bit.ly/2Apb56U

➡ Yesterday, data showed that exports contracted YoY over the same period.

*Link: bit.ly/2Apb56U

➡ Yesterday, data showed that exports contracted YoY over the same period.

#China Leads Slump in #Asia Factories as #TradeWar Cools Demand - Bloomberg

*#Manufacturing oriented economies in Asia already feeling pain

*Link: bloom.bg/2AsbJjS

*#Manufacturing oriented economies in Asia already feeling pain

*Link: bloom.bg/2AsbJjS

🇸🇪 🇪🇺 #Sweden Dec PMI #Manufacturing: 52.0 v 56.2e (lowest since Feb 2016)

- Prior revised lower from 56.7 to 55.4

➡ Sweden PMI is often seen as a leading indicator for a broader slowdown in European manufacturing.

bloomberg.com/news/articles/…

- Prior revised lower from 56.7 to 55.4

➡ Sweden PMI is often seen as a leading indicator for a broader slowdown in European manufacturing.

bloomberg.com/news/articles/…

🇹🇷 #Turkey Dec #Manufacturing PMI: 44.2 (3-month low; 9th straight contraction) v 44.7 prior

*Link: bit.ly/2LMbftf

*Link: bit.ly/2LMbftf

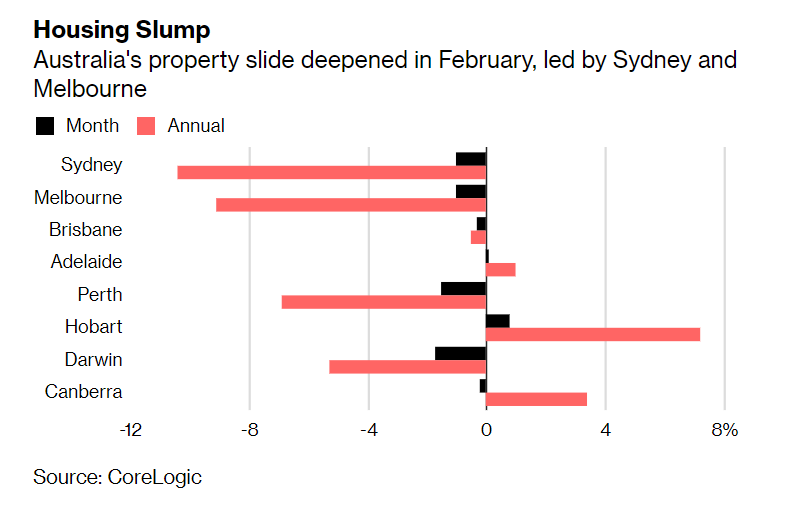

🇦🇺 #Sydney #Housing Slump Deepens as Prices Drop Most Since 1980s - Bloomberg

*Prices in #Australia’s largest city drop 11.1% from 2017 peak

*Link: bloom.bg/2SwkGQn

*Prices in #Australia’s largest city drop 11.1% from 2017 peak

*Link: bloom.bg/2SwkGQn

🇰🇷 #SouthKorea's #KOSPI index, a proxy for world trade growth, remained under pressure this morning and points to a sharp slowdown.

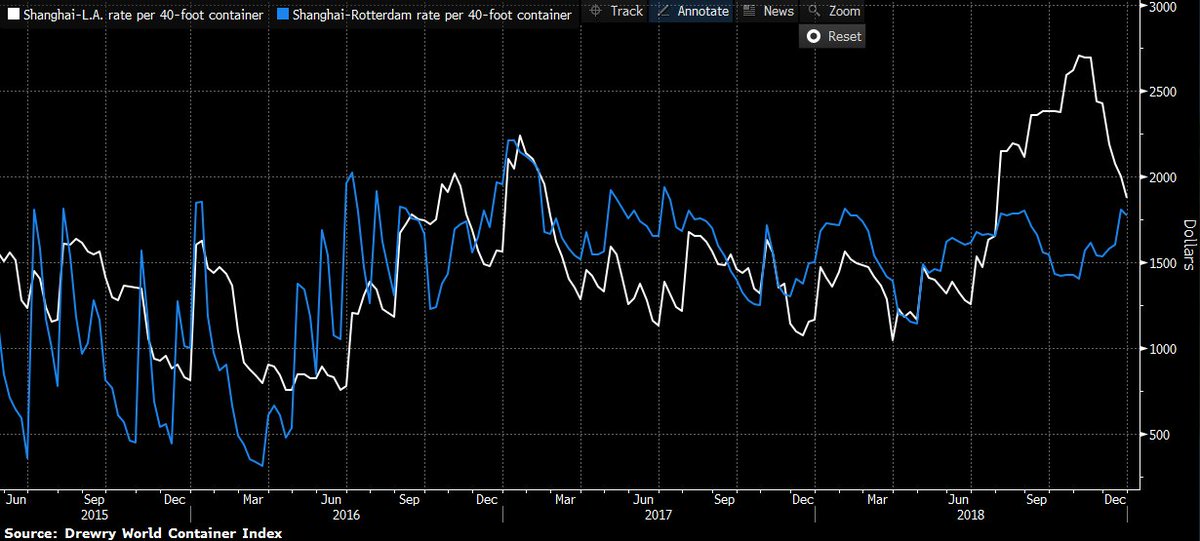

As flagged several times (bit.ly/2F5tQQG), I expect a sharp slowdown of global trade growth from Nov amid:

*⬇ activity

*negative base effect

*the end of frontloading (in line with the ⬇ normalization of #Shanghai-LA containers rate)

*⬇ activity

*negative base effect

*the end of frontloading (in line with the ⬇ normalization of #Shanghai-LA containers rate)

🇨🇳 #China's Q4 GDP growth highly likely fell below 6.5%: magazine - Global Times

*Downward pressure comes from the China-US #tradewar, one-size-fits-all policies and inaction at some agencies.

*Note: 3Q GDP was up 6.5% YoY

*Link: globaltimes.cn/content/113437…

*Downward pressure comes from the China-US #tradewar, one-size-fits-all policies and inaction at some agencies.

*Note: 3Q GDP was up 6.5% YoY

*Link: globaltimes.cn/content/113437…

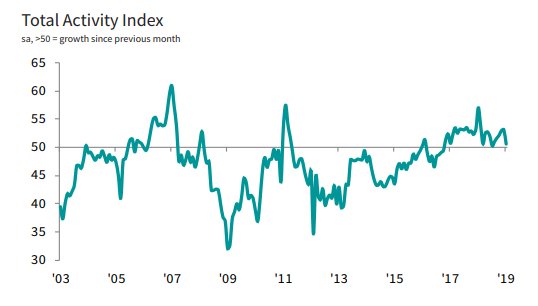

Global #Manufacturing PMI: 51.5 (27-month low) V 52.0 prior

*New order growth was the weakest since August 2016.

*Link: bit.ly/2To631k

*New order growth was the weakest since August 2016.

*Link: bit.ly/2To631k

Global #Manufacturing PMI: New Exports Orders ⬇ in Dec. (-0.2pt to 49.6; lowest since May 2016) and remained in contraction territory for the 4th straight month.

*As discussed (bit.ly/2GRnMgo), I expect a sharp slowdown of global trade growth from Nov.

*As discussed (bit.ly/2GRnMgo), I expect a sharp slowdown of global trade growth from Nov.

Last month, I cut my global GDP forecast for 2019 (for the first time since May 2018) from 3.5% to 3.4% as global trade growth won't exceed 3% this year (based on World Bank methodology).

*It was +4.8% in 2017 and likely ~3.6%/3.7% in 2018.

*It was +4.8% in 2017 and likely ~3.6%/3.7% in 2018.

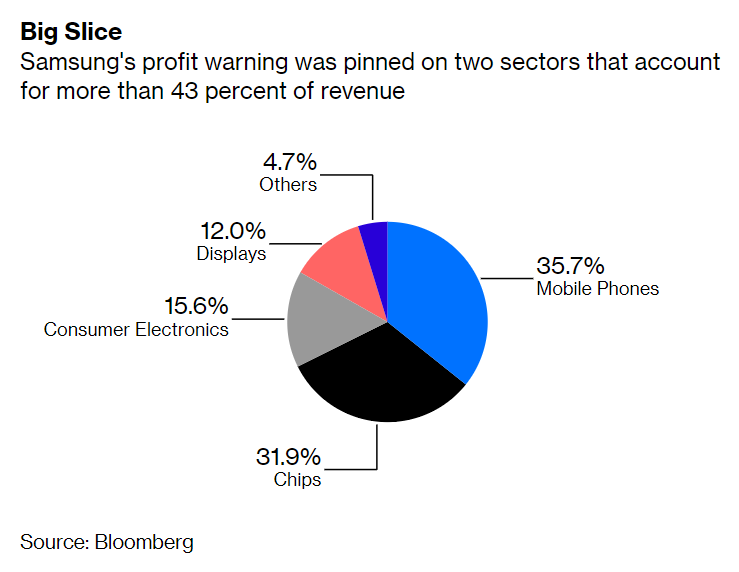

🇺🇸 #Apple Cuts Sales Outlook on Weakness in #IPhone Demand, #China - Bloomberg

*The announcement sent shares down as much as 8.5 percent in extended trading.

*Letter from Cook to investors (apple.co/2TnIC8E)

bloomberg.com/news/articles/…

*The announcement sent shares down as much as 8.5 percent in extended trading.

*Letter from Cook to investors (apple.co/2TnIC8E)

bloomberg.com/news/articles/…

Excluding specific factors, the announcement is only a confirmation of what I described on the macro front:

*A significant ⬇ in the semiconductor sector seen via 🇰🇷 exports (bit.ly/2LN3Wlj)

*A slowdown in #China (bit.ly/2AtDHMp)

*A significant ⬇ in the semiconductor sector seen via 🇰🇷 exports (bit.ly/2LN3Wlj)

*A slowdown in #China (bit.ly/2AtDHMp)

🇺🇸 🇨🇳 *HASSETT: `LOT' OF COS. COULD SEE SLOWING EARNINGS ON #CHINA - BBG

*CHINA ECONOMY SLOWING, COULD BE RECESSION, HASSETT SAYS ON CNN

*CHINA ECONOMY SLOWING, COULD BE RECESSION, HASSETT SAYS ON CNN

🇦🇺 🇭🇰 🇸🇬 🇨🇳 #Housing | #Property Markets From Hong Kong to Sydney Join Global Slump - Bloomberg

*Rising interest rates, volatile stocks have dented sentiment

*Link: bloom.bg/2BW1sMS

*Rising interest rates, volatile stocks have dented sentiment

*Link: bloom.bg/2BW1sMS

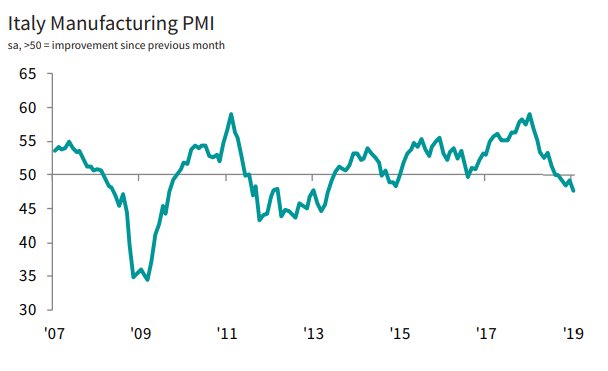

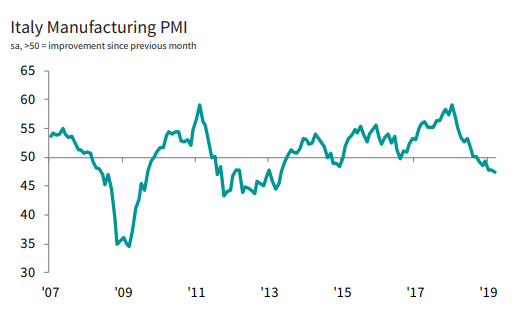

🇮🇹 #ITALY DEC SERVICES PMI: 50.5 V 50.1E (3-month high)

*Composite PMI: 50.0 v 49.3e (3-month high)

*Link: bit.ly/2Qm1y5I

➡ Dec. print was above expectations, yet, the Composite PMI reached 49.6 in 4Q suggesting another contraction (and therefore a technical recession)

*Composite PMI: 50.0 v 49.3e (3-month high)

*Link: bit.ly/2Qm1y5I

➡ Dec. print was above expectations, yet, the Composite PMI reached 49.6 in 4Q suggesting another contraction (and therefore a technical recession)

🇮🇹 #Italy | Yesterday, the #BOI coincident indicator decreased to -0.19 in Dec. (lowest since Dec. 2014)

*It fell to -11 in 4Q18 (lowest since 1Q15 and down from +2 in 3Q18)

*Link: bit.ly/2VnyIFP

*It fell to -11 in 4Q18 (lowest since 1Q15 and down from +2 in 3Q18)

*Link: bit.ly/2VnyIFP

🇫🇷 Dec. Services and Composite PMIs were revised ⬇ compared to flash estimates suggesting that the impact of #YellowVestProtests was stronger than initially feared.

*As I expected (bit.ly/2R8VkLP), 4Q GDP should be close to 0%.

*As I expected (bit.ly/2R8VkLP), 4Q GDP should be close to 0%.

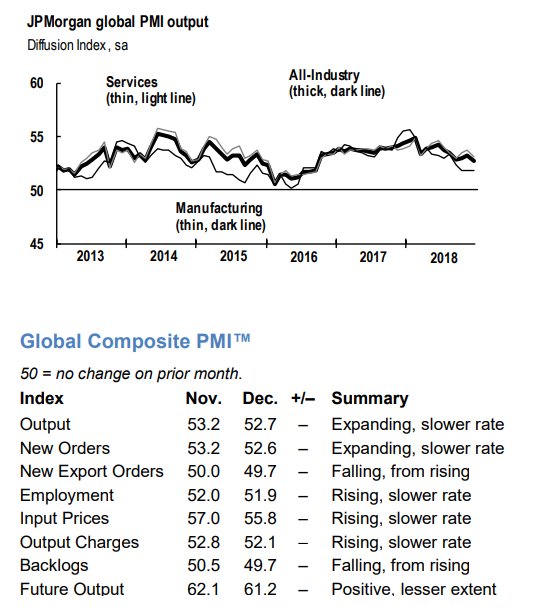

Dec. Global Composite PMI:

*Output: 52.7 (27-month low) v 53.2 prior

*New Export Orders: 49.7 v 50.0 prior (2nd contraction during the past four months).

*Link: bit.ly/2sbRxOH

*Output: 52.7 (27-month low) v 53.2 prior

*New Export Orders: 49.7 v 50.0 prior (2nd contraction during the past four months).

*Link: bit.ly/2sbRxOH

🇨🇳 Nervous markets: how vulnerable is #China’s economy? - FT

*An economics professor at Renmin University in #Beijing sparked a minor furore last month when he claimed a secret government research group had estimated growth could be as low as 1.67% in 2018

ft.com/content/5839f5…

*An economics professor at Renmin University in #Beijing sparked a minor furore last month when he claimed a secret government research group had estimated growth could be as low as 1.67% in 2018

ft.com/content/5839f5…

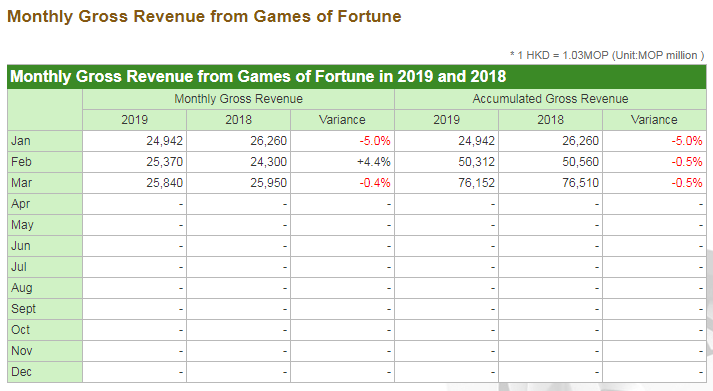

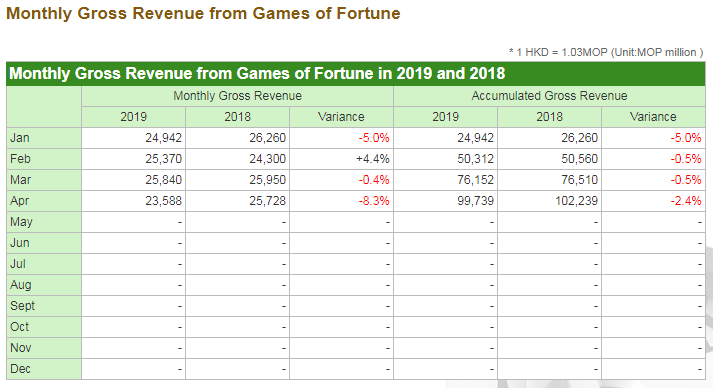

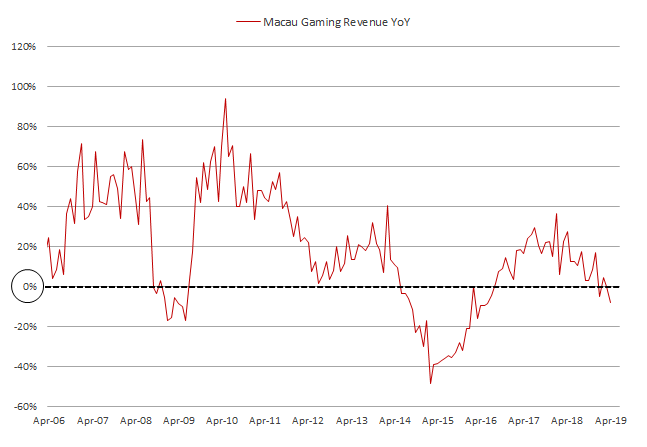

🇲🇴 Morgan Stanley switched its view on the world’s biggest #gambling hub, estimating a 2% ⬇ in 2019 revenue (down from +5%) - Bloomberg

*Earlier this month, JPMorgan forecasted revenue would ⬇ 1% in 2019.

*Analysts expect a ⬇ this month (would break a 29-month growth streak)

*Earlier this month, JPMorgan forecasted revenue would ⬇ 1% in 2019.

*Analysts expect a ⬇ this month (would break a 29-month growth streak)

🇯🇵 #Japan Dec PMI Services: 51.0 v 52.3 prior (3-month low)

*PMI Composite: 52.0 v 52.4 prior (3-month low)

*Link: bit.ly/2LSpaOy

*PMI Composite: 52.0 v 52.4 prior (3-month low)

*Link: bit.ly/2LSpaOy

🇦🇺 #Australia Dec AIG #Manufacturing Index: 49.5 v 51.3 prior (first contraction in 26 months, lowest reading since Aug 2016)

*Exports 47.1, -3.8 pts

*Exports 47.1, -3.8 pts

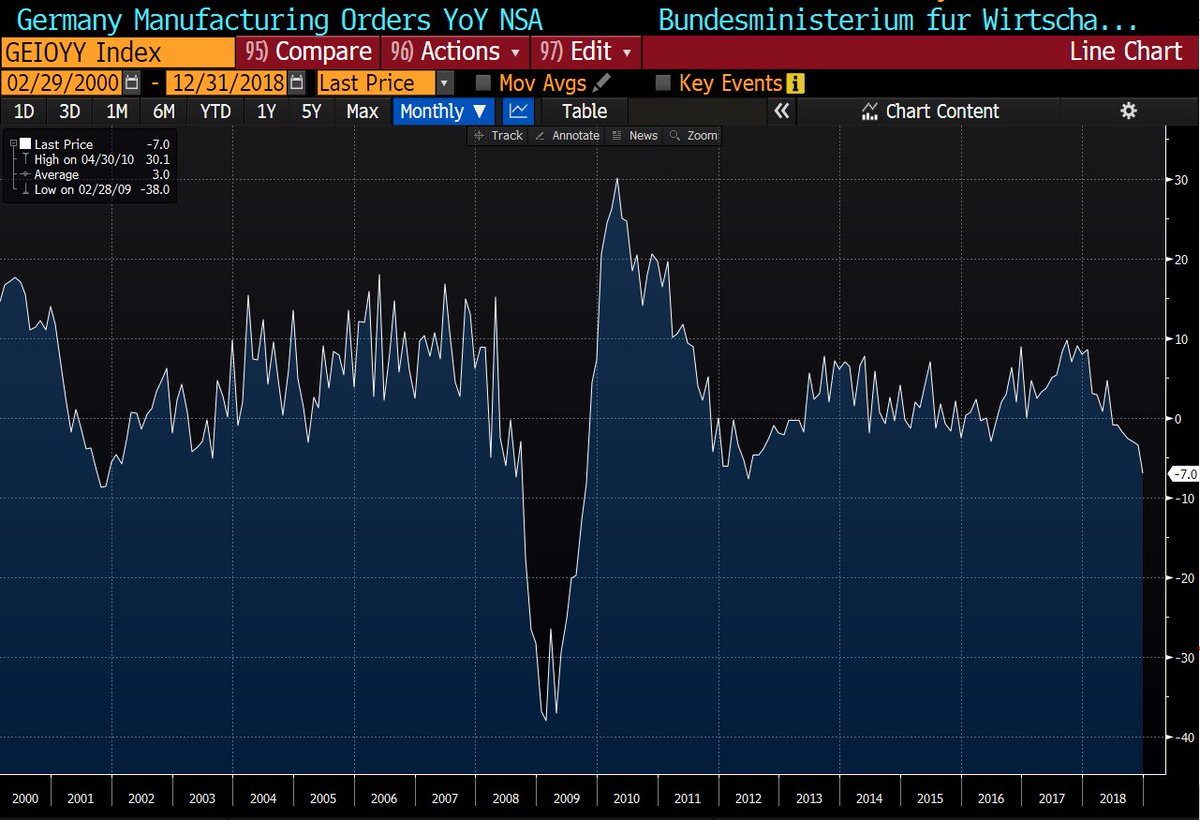

🇩🇪 #GERMANY NOV FACTORY ORDERS; Y/Y: -4.3% (largest decline since Aug. 12) V -2.7%E

*Prior YoY revised lower from -2.7% to -3.0%.

➡ It's a good leading indicator of global trade growth, which suggests more downside ahead.

*Prior YoY revised lower from -2.7% to -3.0%.

➡ It's a good leading indicator of global trade growth, which suggests more downside ahead.

🇩🇪 #GERMANY NOV INDUSTRIAL PRODUCTION M/M: -1.9% V +0.3%E (largest MoM ⬇ since July 2018); Y/Y: -4.7% V -0.8%E (largest YoY ⬇ since Dec. 2009)

- Prior MoM revised lower from -0.5% to -0.8%

- Prior YoY revised lower from 1.6% to 0.5%

- Prior MoM revised lower from -0.5% to -0.8%

- Prior YoY revised lower from 1.6% to 0.5%

🇩🇪 The downward revision in October and the sharp drop in November suggest that German GDP is unlikely to rebound significantly in 4Q.

Given that 🇫🇷 GDP will be also muted in 4Q (bit.ly/2Ripnkk), EU GDP will come below ECB expectations (+0.4%e QoQ), likely implying a downward revision for 2018 (from +1.9% to +1.8%).

🇪🇺 It implies a lower base effect for 2019 and reinforces my bearish view that both the consensus and the #ECB are too much optimistic on 2019 GDP:

*Bloomberg consensus: +1.6%

*ECB: +1.7% (bit.ly/2QB33SE)

*Bloomberg consensus: +1.6%

*ECB: +1.7% (bit.ly/2QB33SE)

🇪🇺 I would not be surprised if the #ECB acknowledges the recent growth slowdown at the next meeting (Jan. 24) or before and clearly prepares the ground for supportive measures such as new TLTROs (reut.rs/2SsIlk7)

🇩🇪 *Note that 2018 German GDP will be released on Jan. 15.

🇩🇪 *Note that 2018 German GDP will be released on Jan. 15.

🇰🇷 Samsung Q4 Profit Forecast disappointed as smartphone and memory markets slowed (reut.rs/2GWxgqC).

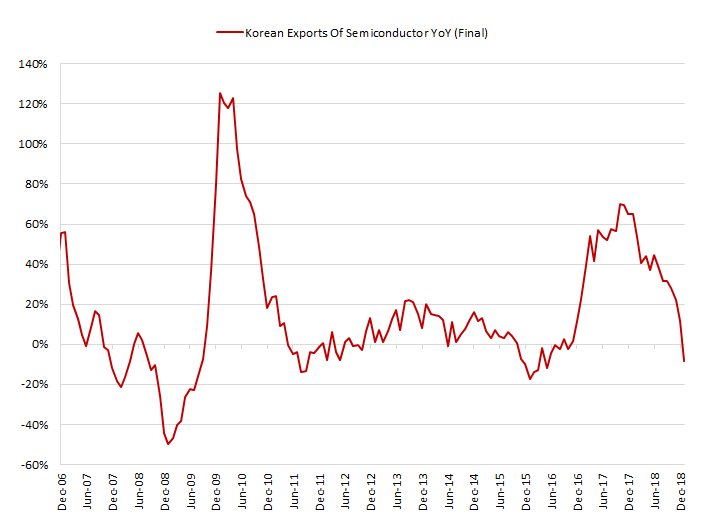

➡ It's coherent with macro data namely the sharp decline in Korean exports of semiconductor seen in Dec. (-8.3% YoY; largest contraction since Apr. 2016)

➡ It's coherent with macro data namely the sharp decline in Korean exports of semiconductor seen in Dec. (-8.3% YoY; largest contraction since Apr. 2016)

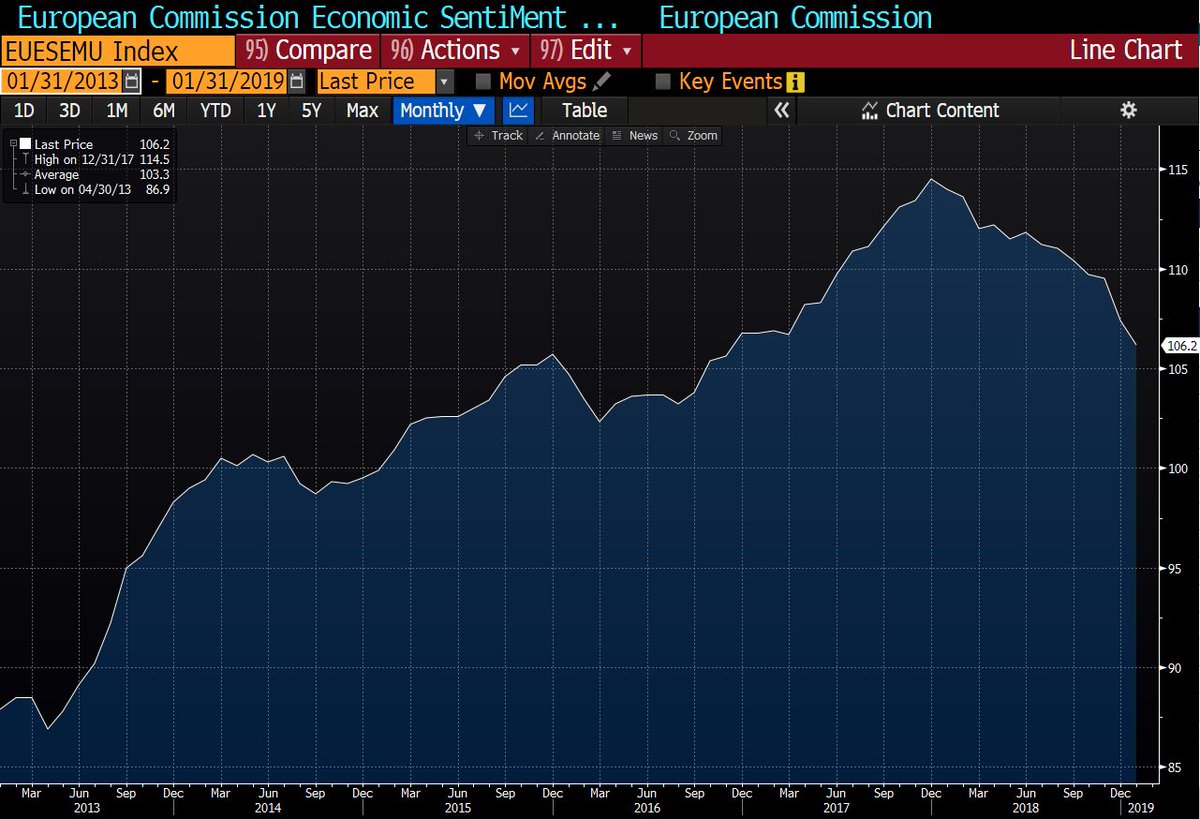

🇪🇺 #Eurozone DEC BUSINESS CLIMATE INDICATOR: 0.82 V 1.00E (lowest since Mar. 2017)

*Dec Economic Confidence: 107.3 v 108.2e (lowest since Dec. 2016; )

➡ Economic confidence slid for a 12th month in December ❗

*Dec Economic Confidence: 107.3 v 108.2e (lowest since Dec. 2016; )

➡ Economic confidence slid for a 12th month in December ❗

More charts ahead of the World Bank Global Economic Update:

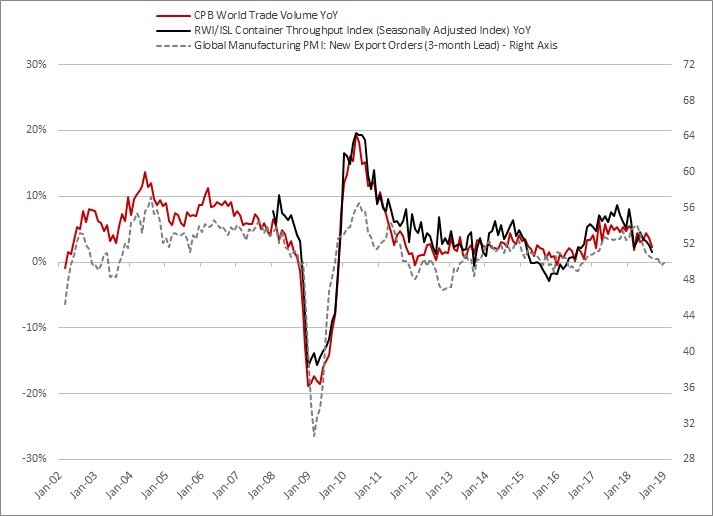

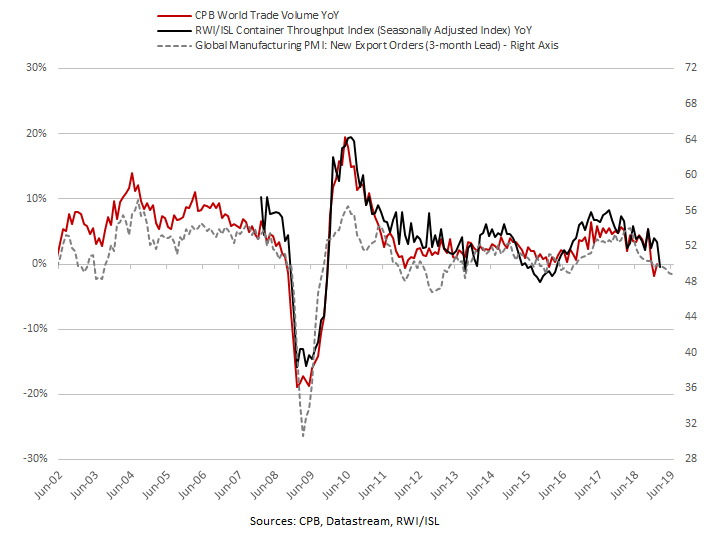

RWI/ISL Container Index rose only 1.3% YoY in Nov., down from +3.8% YoY in Oct.

*A part of the recent increase included a surge in empty containers being shipped back to Asia - Bloomberg

*Link: bloom.bg/2QXHMCQ

RWI/ISL Container Index rose only 1.3% YoY in Nov., down from +3.8% YoY in Oct.

*A part of the recent increase included a surge in empty containers being shipped back to Asia - Bloomberg

*Link: bloom.bg/2QXHMCQ

#Hongkong Air Freight Index fell 2.1% YoY in Nov. (largest drop since Mar. 2018), down from +2.8% YoY in Oct.

Harpex Weekly Shipping Index (4-week moving average) fell from +6.1% YoY in Mid-Nov. 2018 to +1.6% YoY in early Jan. 2019

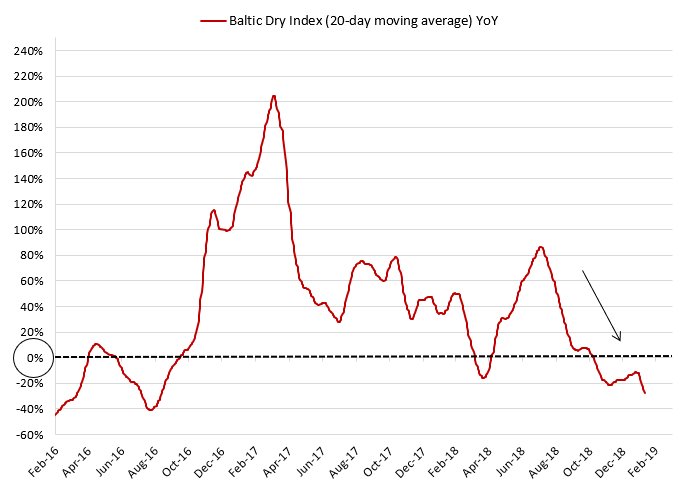

More and more figures suggest that the end of frontloading has led to a significant slowdown in global trade growth reflecting the real underlying trend.

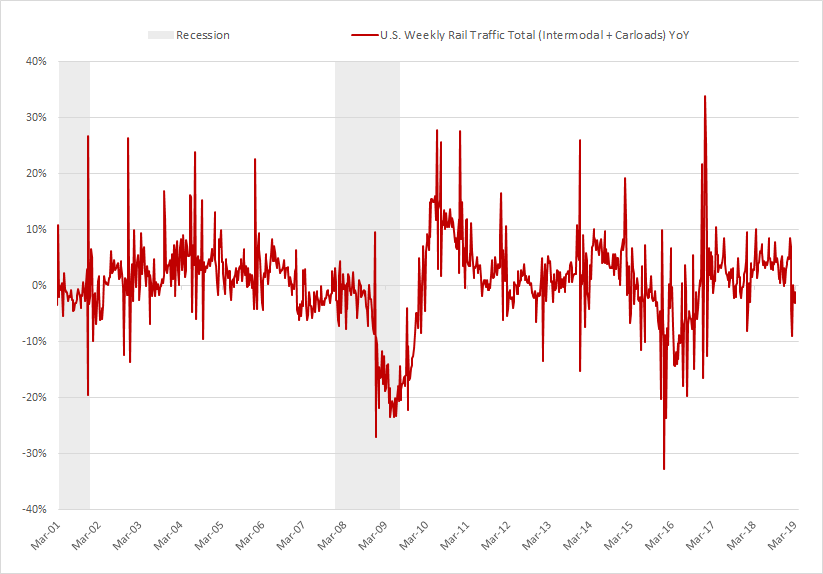

🇺🇸 🇨🇳 Imports at major US container ports are leveling off after retailers’ months-long rush to bring in Chinese merchandise before higher tariffs hit - NRF

*January is forecast at 1.75 million TEU, down 0.9 percent from January 2018 ❗

*Link: bit.ly/2CX4zWr

*January is forecast at 1.75 million TEU, down 0.9 percent from January 2018 ❗

*Link: bit.ly/2CX4zWr

🇨🇳#CHINA DEC. RETAIL PASSENGER VEHICLE SALES -19% ON YEAR: PCA - BBG

*CHINA 2018 RETAIL PASSENGER VEHICLE SALES FALL 6.0% ON YEAR

*CHINA CAR SALES HAVE FIRST ANNUAL DROP IN MORE THAN 2 DECADES

*CHINA 2018 RETAIL PASSENGER VEHICLE SALES FALL 6.0% ON YEAR

*CHINA CAR SALES HAVE FIRST ANNUAL DROP IN MORE THAN 2 DECADES

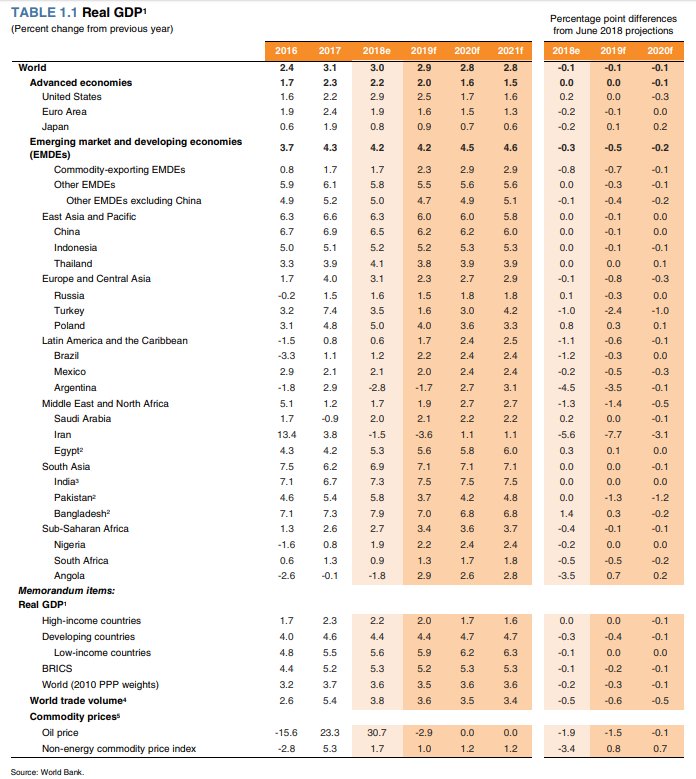

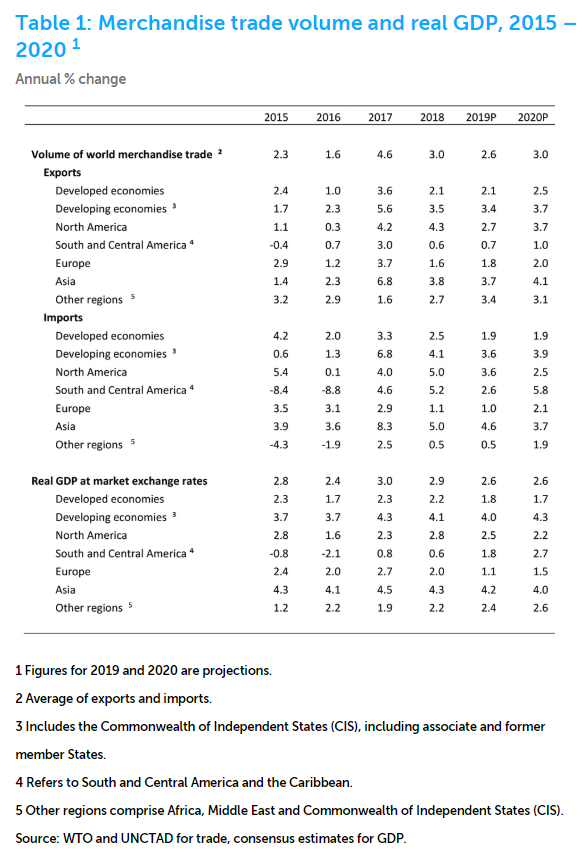

As I expected (bit.ly/2FjzdLn), the World Bank cut its 2019 forecasts for:

*Global GDP (PPP weights) from +3.8% to +3.5%

*World Trade Volume from +4.2% to +3.6%

*Link: bit.ly/1gIuEF3

➡ It still looks a bit optimistic especially for World Trade Volume growth.

*Global GDP (PPP weights) from +3.8% to +3.5%

*World Trade Volume from +4.2% to +3.6%

*Link: bit.ly/1gIuEF3

➡ It still looks a bit optimistic especially for World Trade Volume growth.

🇩🇪 German lighting and semiconductor specialist Osram Licht AG is facing “dark clouds on the horizon” in 2019 after the most recent quarter was worse than expected, CEO Olaf Berlien told German newspaper Augsburger Allgemeine.

uk.reuters.com/article/uk-ger…

uk.reuters.com/article/uk-ger…

🇬🇧 Jaguar Land Rover to make 'substantial' job cuts after #China, #diesel slump- source - Reuters

reuters.com/article/us-jag…

reuters.com/article/us-jag…

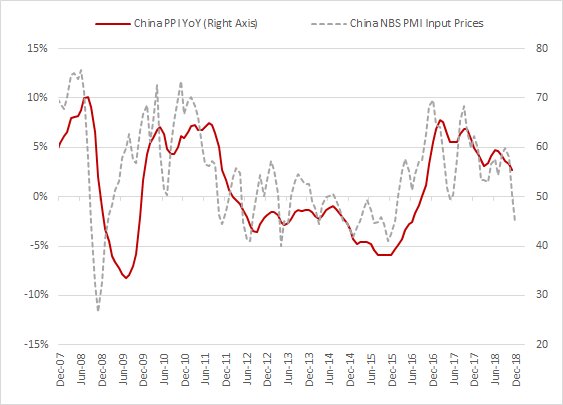

🇨🇳 #China’s factory inflation slowed sharply in December, continuing the slowdown for a sixth straight month to the weakest level since Sept. 2016.

*It adds concerns over corporate profitability.

*Dec. PPI Y/Y: 0.9% V 1.6%E

*It adds concerns over corporate profitability.

*Dec. PPI Y/Y: 0.9% V 1.6%E

🇪🇸 #SPAIN SEES 2.2% GROWTH IN 2019: CALVINO - BBG

*SPAIN ECONOMY PROBABLY GREW 2.6% IN 2018, CALVINO SAYS

*SPAIN CUTTING GROWTH ESTIMATE ON TIGHTER FISCAL STANCE: CALVINO

*SPAIN ECONOMY PROBABLY GREW 2.6% IN 2018, CALVINO SAYS

*SPAIN CUTTING GROWTH ESTIMATE ON TIGHTER FISCAL STANCE: CALVINO

🇪🇺 Looking ahead, the suggestion was made to revisit the contribution of targeted longer-term refinancing operations to the monetary policy stance. - #ECB MINUTES

*Link: bit.ly/2SHZsyW

*Link: bit.ly/2SHZsyW

🇨🇳 #CHINA TO SET LOWER GDP GROWTH TARGET OF 6%-6.5% IN 2019 - SOURCES - RTRS

🇨🇳 #CHINA MAY KEEP 2019 BUDGET DEFICIT TARGET BELOW 3% GDP: REUTERS

*CHINA TO KEEP CONSUMER INFLATION TARGET AT 3% IN 2019: REUTERS

*CHINA TO KEEP CONSUMER INFLATION TARGET AT 3% IN 2019: REUTERS

🇨🇳 #China plans to set a lower economic growth target of 6-6.5 percent in 2019 compared with last year’s target of “around” 6.5 percent, policy sources told Reuters, as Beijing gears up to cope with higher U.S. tariffs and weakening domestic demand.

uk.reuters.com/article/uk-chi…

uk.reuters.com/article/uk-chi…

🇺🇸 🇨🇳 U.S.-#China Speed Dating Isn’t Enough to Tame Global Headwinds - Bloomberg

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

🇪🇺 🇩🇪 #ECB'S NOWOTNY SAYS GERMANY LIKELY HAVE VERY LOW GROWTH RATE IN Q4

fxstreet.com/news/ecbs-nowo…

fxstreet.com/news/ecbs-nowo…

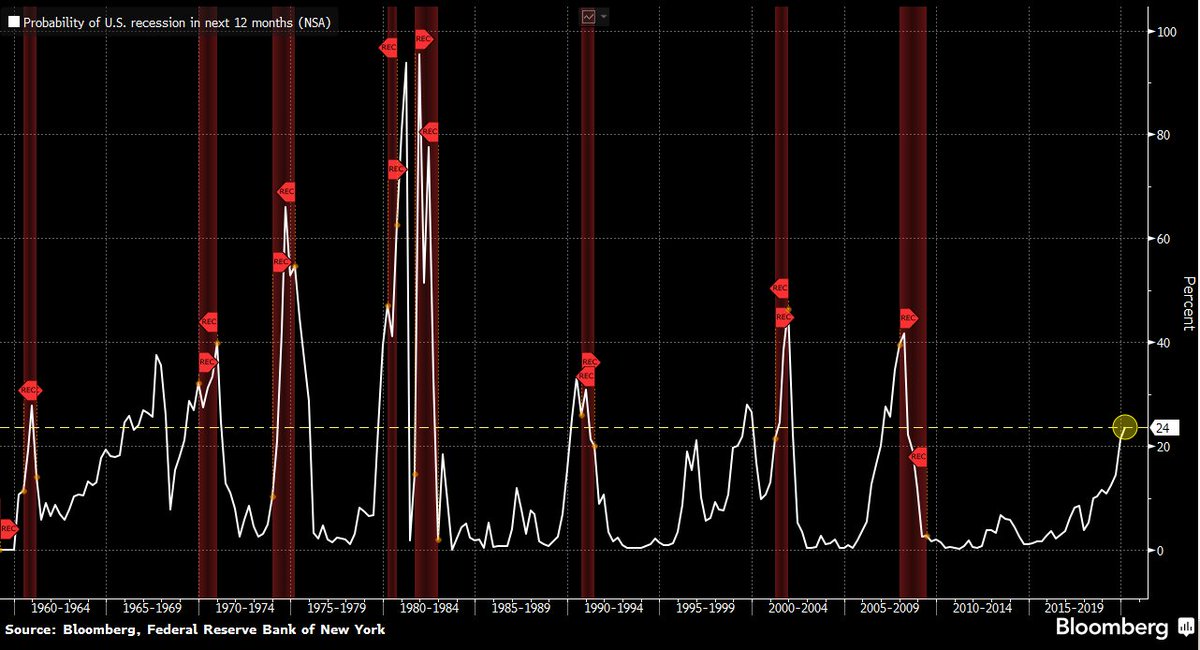

🇺🇸 Economists surveyed by Bloomberg over the past week see a median 25 percent chance of a slump in the next 12 months, up from 20 percent in the December survey and the highest in more than six years,

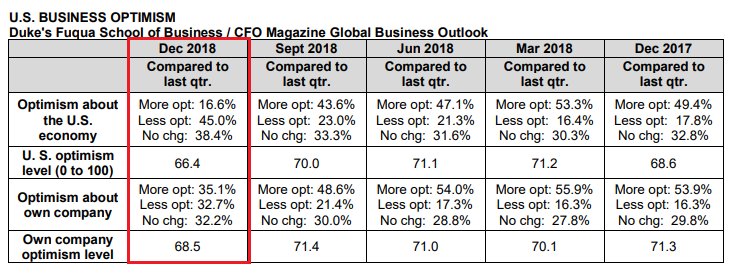

🇺🇸 Nearly half (48.6%) of U.S. CFOs believe that the U.S. will be in recession by the end of 2019, and 82% believe that a recession will have begun by the end of 2020, according to the Duke University/CFO Global Business Outlook.

*Link: bit.ly/2VNbFo0

*Link: bit.ly/2VNbFo0

🇺🇸 Several proxies also show that CAPEX expectations ⬇ further in December - Bloomberg

🇺🇸 🇨🇳 Another analysis (bit.ly/2D8msC1that) suggests the end of frontloading has led to a significant slowdown in global trade growth.

*Bloomberg link: bloom.bg/2Ayvw1h

*Bloomberg link: bloom.bg/2Ayvw1h

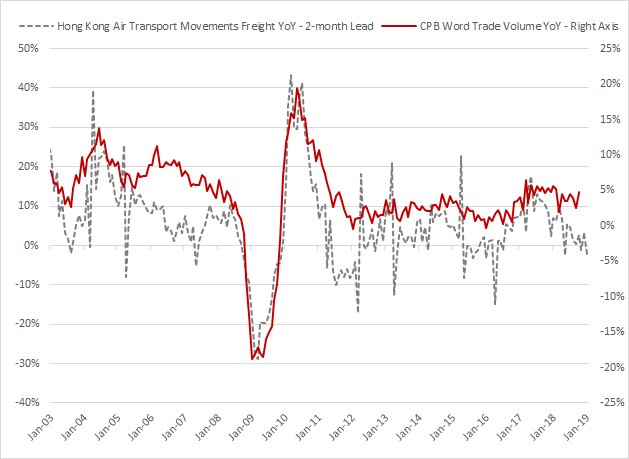

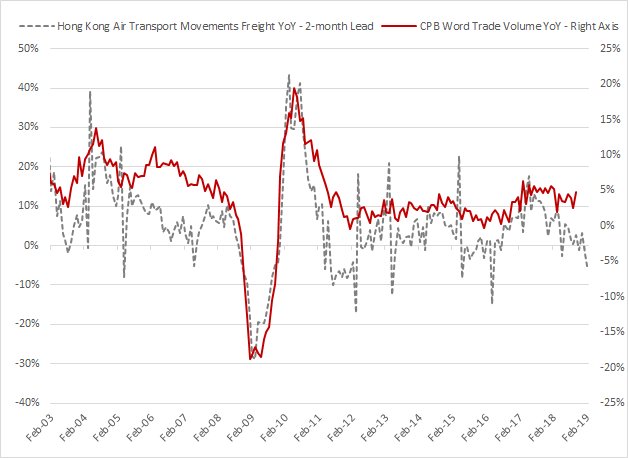

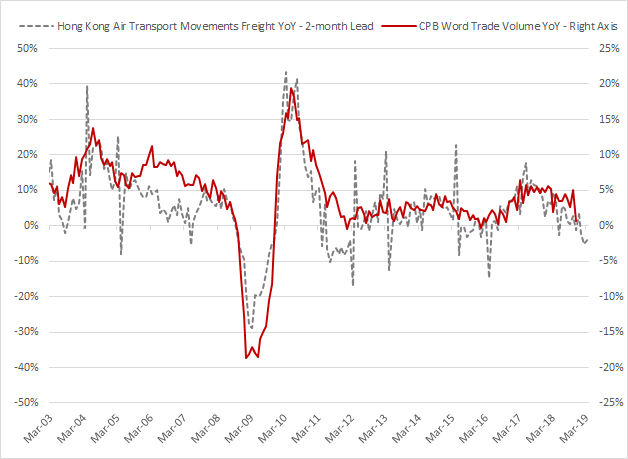

🇭🇰 Hong Kong Air Transport Movements (Freight) fell 5.2% YoY in Dec. (largest contraction since Feb. 2016) v -2.1% YoY in Nov.

*Link: bit.ly/2SvU16q

*Link: bit.ly/2SvU16q

As I expected:

🇨🇳 #CHINA DEC. IMPORTS -7.6% Y/Y IN DOLLAR TERMS; EST. +4.5%

*Largest contraction since July 2016.

🇨🇳 #CHINA DEC. IMPORTS -7.6% Y/Y IN DOLLAR TERMS; EST. +4.5%

*Largest contraction since July 2016.

🇨🇳#CHINA Dec Exports YoY: -4.4% v 2.0%e (largest ⬇ since Dec 2016)

➡ Frontloading appears to be fading

*Imports YoY: -7.6% v 4.5%e (largest ⬇ since July 2016)

➡ It reflects ⬇ exports, weaker domestic demand and ⬇ commodity prices

*Link: bloom.bg/2AMMPLY

➡ Frontloading appears to be fading

*Imports YoY: -7.6% v 4.5%e (largest ⬇ since July 2016)

➡ It reflects ⬇ exports, weaker domestic demand and ⬇ commodity prices

*Link: bloom.bg/2AMMPLY

As I already warned, more and more figures (bit.ly/2D7pkz5; bit.ly/2D8msC1) suggest that the end of frontloading has led to a significant slowdown in global trade growth reflecting the real (weak) underlying trend ❗

🇩🇪 #Germany automotive supplier Continental said its operating margin would fall this year, citing mounting pressure on the car industry which is struggling with a shift away from combustion engines towards electric cars - Reuters

*Link: uk.reuters.com/article/uk-con…

*Link: uk.reuters.com/article/uk-con…

🇪🇺 I think that economists and the #ECB remain too much optimistic about growth prospects.

*We'll see more ⬇ revisions in the coming weeks.

*We'll see more ⬇ revisions in the coming weeks.

As I expected:

🇪🇺 Eurozone Nov Industrial Production M/M: -1.7% v -1.5%e; Y/Y: -3.3% v -2.1%e

🇪🇺 Eurozone Nov Industrial Production M/M: -1.7% v -1.5%e; Y/Y: -3.3% v -2.1%e

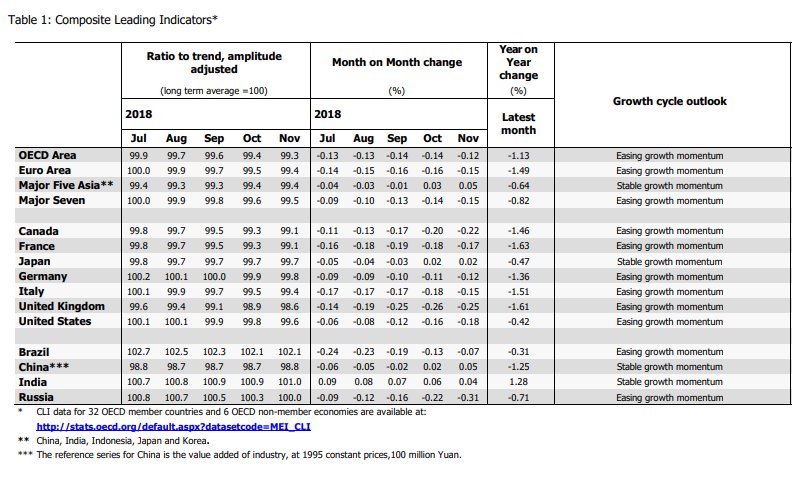

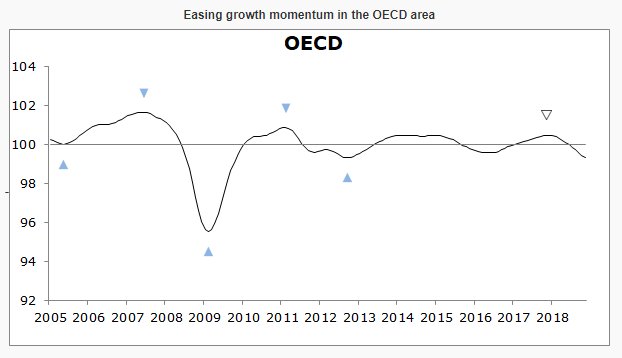

#OECD Nov. Leading Indicator: 99.3 v 99.4 prior

*Composite leading indicators, designed to anticipate turning points in economic activity relative to trend 6 to 9 months ahead, continue to point to ⬇ growth momentum.

*Link: bit.ly/2snBNZ6

*Composite leading indicators, designed to anticipate turning points in economic activity relative to trend 6 to 9 months ahead, continue to point to ⬇ growth momentum.

*Link: bit.ly/2snBNZ6

🇨🇳 #China | After officials noted that downward pressure increases and favored new fiscal, monetary and technical measures, we can fear that figures for Dec. and 4Q (IP, RS, FAI, GDP) will be disappointing next Monday.

🇩🇪 German Economy Probably Grew Slightly In 4Q18 - Stats Office – RTRS

➡ The limited rebound is lower than the consensus expected (+0.4%e for Bloomberg consensus) implying lower base effect for 2019.

➡ The limited rebound is lower than the consensus expected (+0.4%e for Bloomberg consensus) implying lower base effect for 2019.

🇩🇪 🇪🇺 It confirms my view (bit.ly/2RxxIAv; bit.ly/2RvY2Lu; bit.ly/2Mf58OE) that both the consensus and the #ECB need to adjust their expectations downward for 2019.

🇪🇺 #ECB DRAGHI: RECENT ECONOMIC DEVELOPMENTS WEAKER THAN EXPECTED - BBG

*DRAGHI: UNCERTAINTIES, ESPECIALLY GLOBAL RISKS, STILL PROMINENT

*DRAGHI: NO ROOM FOR COMPLACENCY, SIGNIFICANT STIMULUS NEEDED

*DRAGHI: UNCERTAINTIES, ESPECIALLY GLOBAL RISKS, STILL PROMINENT

*DRAGHI: NO ROOM FOR COMPLACENCY, SIGNIFICANT STIMULUS NEEDED

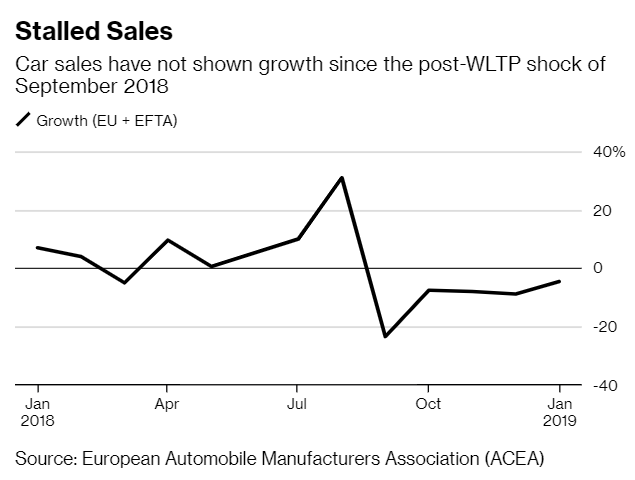

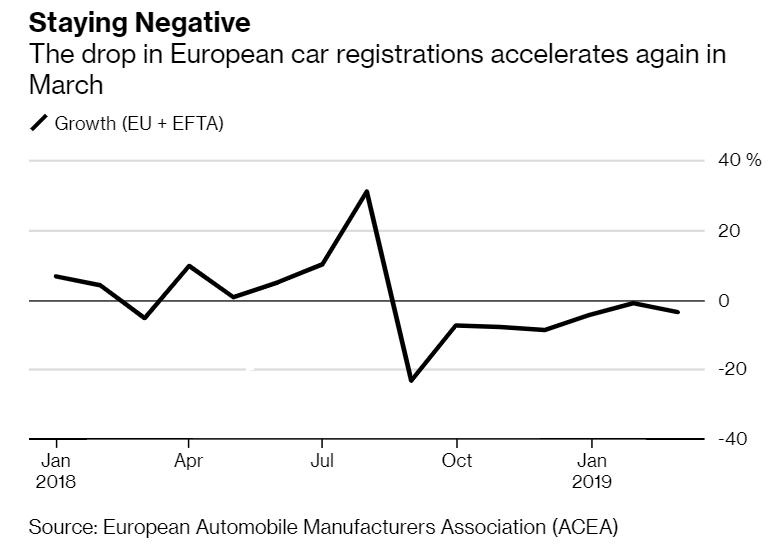

🇪🇺 *EUROPEAN DECEMBER CAR SALES DOWN 8.7% TO 1.04M UNITS: ACEA - BBG

*EUROPEAN 2018 CAR SALES DROP 0.04%, FIRST DECLINE SINCE 2013

*EUROPEAN 2018 CAR SALES DROP 0.04%, FIRST DECLINE SINCE 2013

🇯🇵 #Japan's November machinery orders stall in worrying sign over business spending - Reuters

reuters.com/article/us-jap…

reuters.com/article/us-jap…

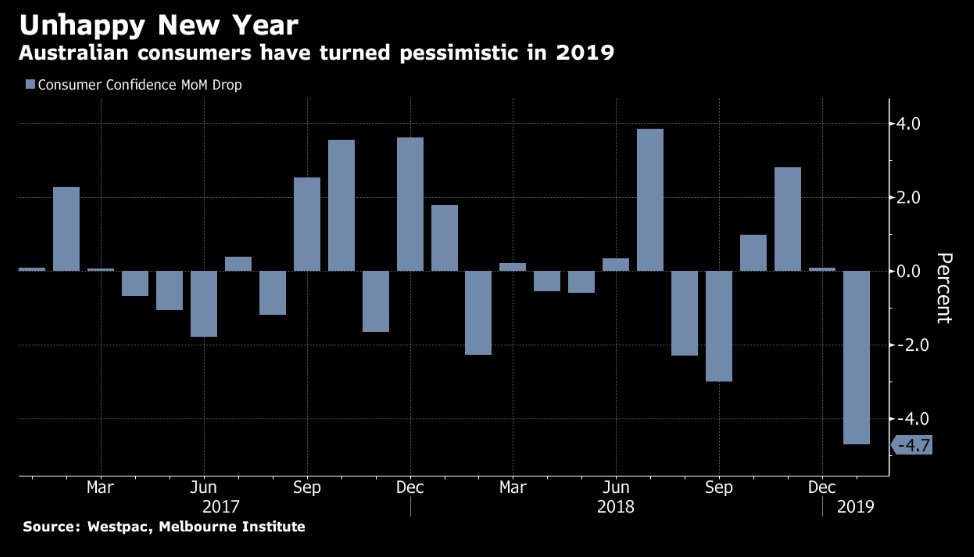

🇦🇺 #Australia | The Westpac Banking Corp.-Melbourne Institute Consumer Sentiment Index for January dropped 4.7% (biggest drop since September 2015) to 99.6 (lowest since Sept. 2017) amid pessimism over falling property prices (bit.ly/2FtW7Az) and economic growth.

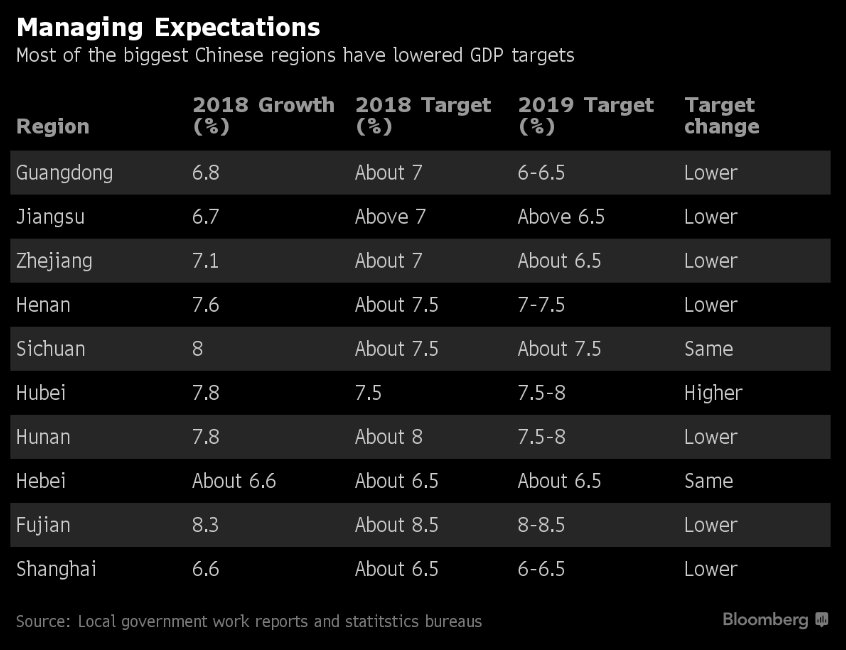

🇨🇳 SCMP reports that 8 out of the 12 provinces in #China that have published their annual growth targets have lowered their expectations.

*#Henan is now targeting GDP growth of 6.5% (⬇ from ~7.5%)

*#Beijing sees growth in the 6-6.5% range (⬇ from 6.5%)

beta.scmp.com/economy/china-…

*#Henan is now targeting GDP growth of 6.5% (⬇ from ~7.5%)

*#Beijing sees growth in the 6-6.5% range (⬇ from 6.5%)

beta.scmp.com/economy/china-…

🇬🇧 #Brexit | Credit Conditions Survey - 2018 Q4 - BOE

*Lenders reported that demand for secured lending for house purchase decreased significantly in Q4, and was expected to decrease further in Q1.

*Link: bit.ly/2TTnrvl

*Lenders reported that demand for secured lending for house purchase decreased significantly in Q4, and was expected to decrease further in Q1.

*Link: bit.ly/2TTnrvl

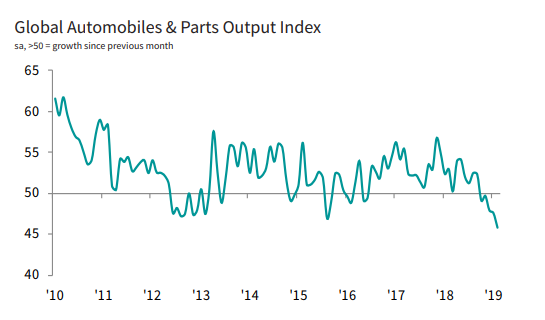

🇨🇳 #CHINA'S CAR-RELATED PRODUCTION FELL 30% YOY IN NOVEMBER: NIDEC - BBG

*As a reminder:

asia.nikkei.com/Business/Compa…

*As a reminder:

asia.nikkei.com/Business/Compa…

🇺🇸 The #governmentshutdown has also affected U.S. trade activity:

Several reports showed that "the protracted impasse threatens to add backups at US borders that would boost freight rates" - Business Times

businesstimes.com.sg/transport/us-s…

Several reports showed that "the protracted impasse threatens to add backups at US borders that would boost freight rates" - Business Times

businesstimes.com.sg/transport/us-s…

🇺🇸 A shortage of TSA staff has also created significant delays in airports, which even closed terminals - Telegraph

telegraph.co.uk/travel/news/us…

telegraph.co.uk/travel/news/us…

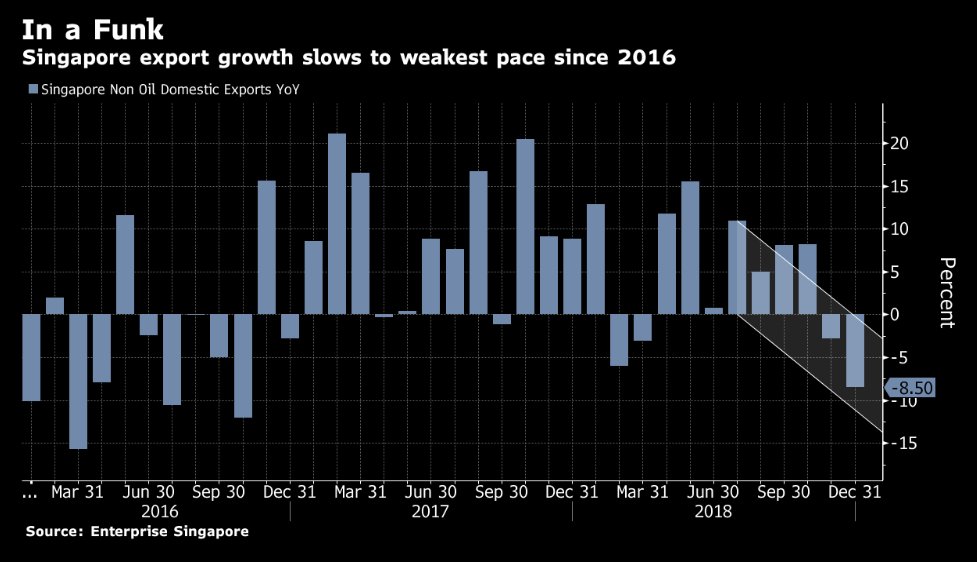

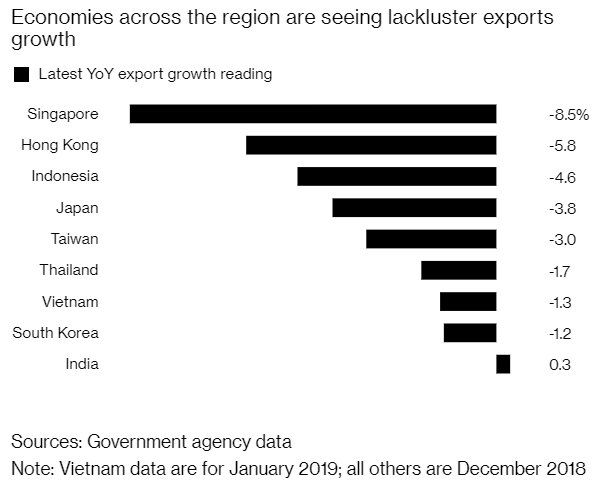

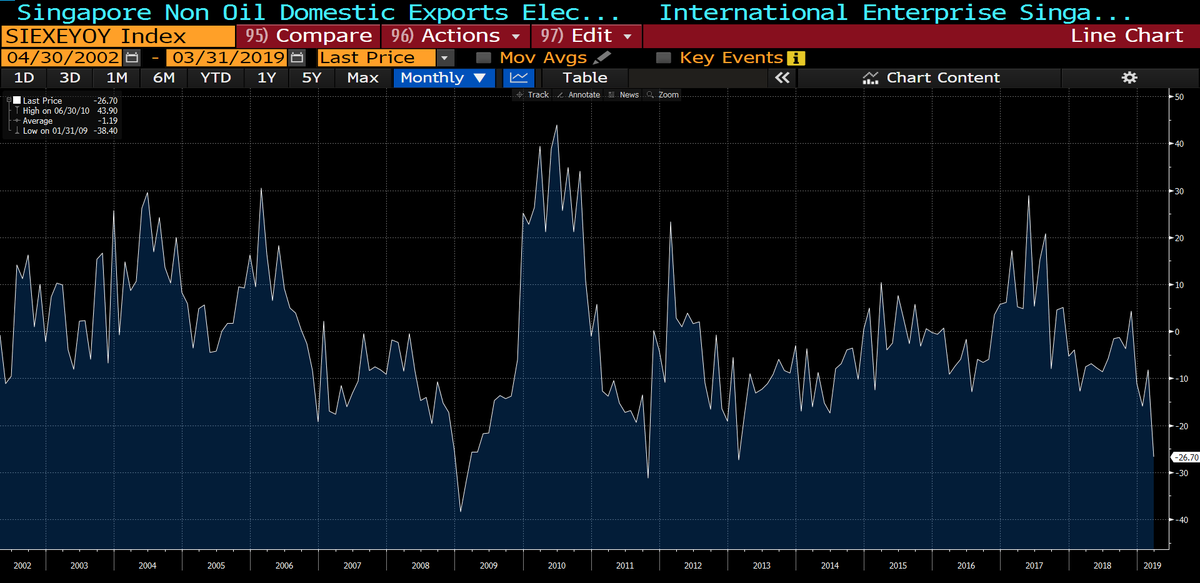

🇸🇬 #Singapore Dec Non-Oil Domestic Exports y/y: -8.5% v +2.0%e (largest ⬇ since October 2016)

- Electronic Exports y/y: -11.2% v 4.3% prior (largest ⬇ since Feb. 2018)

- Electronic Exports y/y: -11.2% v 4.3% prior (largest ⬇ since Feb. 2018)

‘Goldilocks Economy’ References Doomed as Global Storms Set In - Bloomberg

*Trade-war side effects and cyclical weakness are tangled up in ugly economic data that continues to pile up across the board

bloomberg.com/news/articles/…

*Trade-war side effects and cyclical weakness are tangled up in ugly economic data that continues to pile up across the board

bloomberg.com/news/articles/…

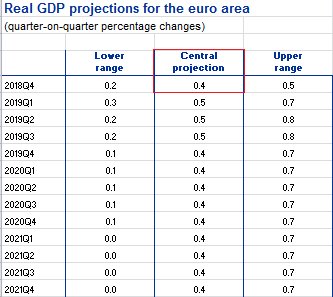

➡ The ECB should acknowledge the recent growth slowdown next week as the central bank expected 4Q18 GDP to reach 0.4% QoQ.

➡ In addition, it should also highlight that risks associated to its outlook are no longer "balanced".

*Link (French): bit.ly/2HitGat

➡ In addition, it should also highlight that risks associated to its outlook are no longer "balanced".

*Link (French): bit.ly/2HitGat

➡ The #ECB will also revise downward its GDP forecasts on March 7 (quarterly update).

➡ As I already noted (bit.ly/2U5xwWf), the consensus will keep adjusting ⬇ in the coming weeks.

➡ As I already noted (bit.ly/2U5xwWf), the consensus will keep adjusting ⬇ in the coming weeks.

🇺🇸 JAN PRELIMINARY UNIVERSITY OF MICHIGAN CONFIDENCE: 90.7 V 96.8E

- Current conditions: 110 v 116e

- Expectations: 78.3 v 86.5e

➡ The measures of current conditions and expectations both declined to the lowest since President Donald Trump's election in 2016.

- Current conditions: 110 v 116e

- Expectations: 78.3 v 86.5e

➡ The measures of current conditions and expectations both declined to the lowest since President Donald Trump's election in 2016.

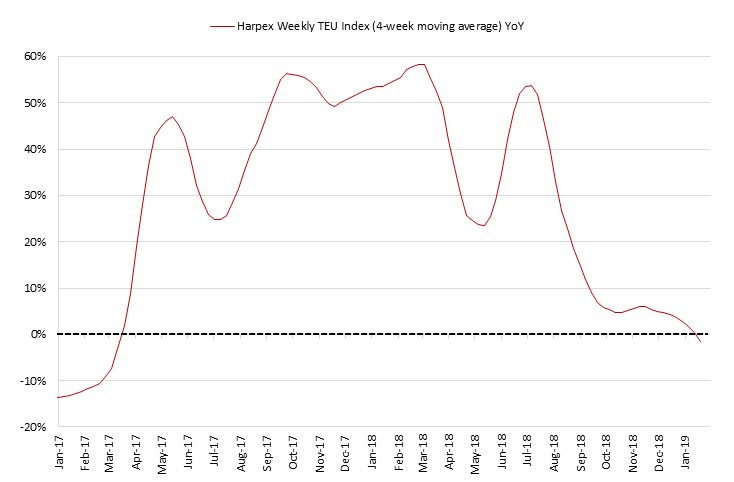

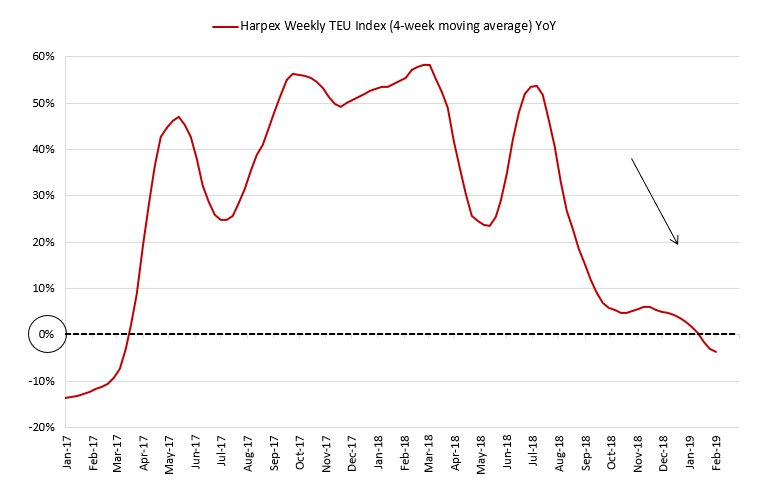

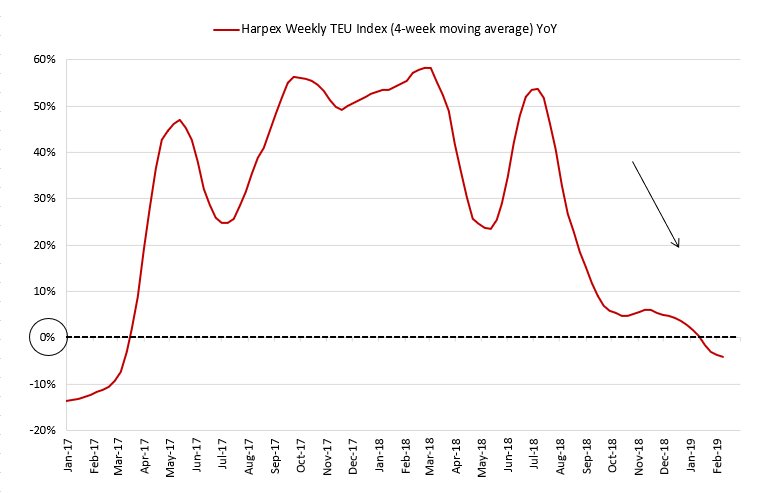

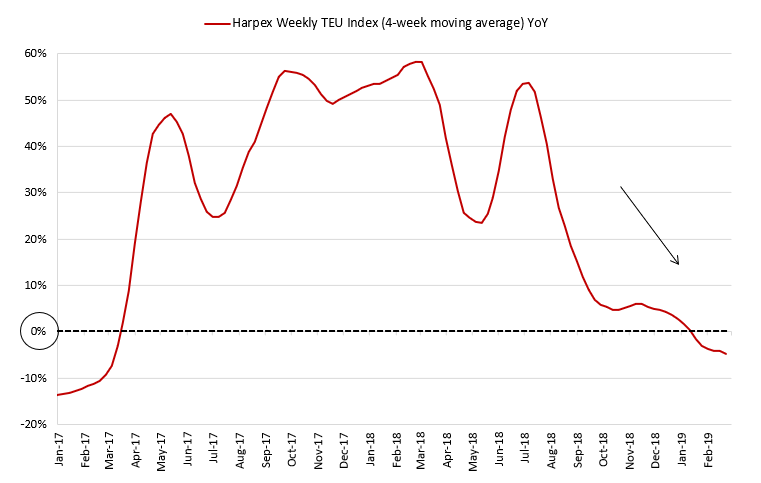

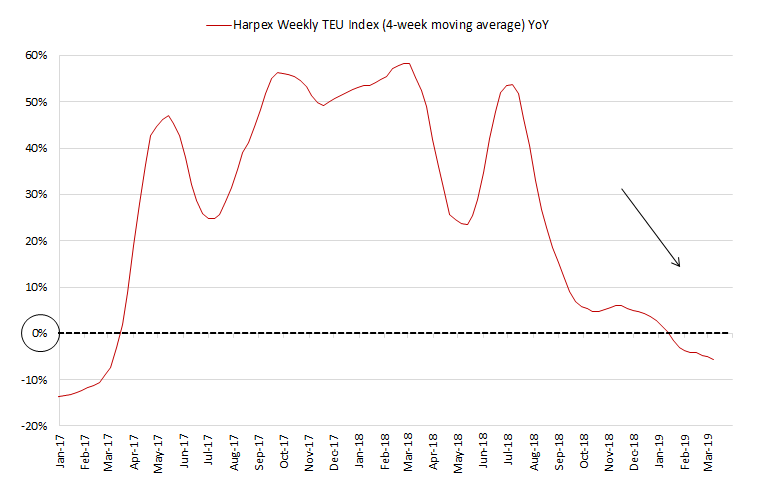

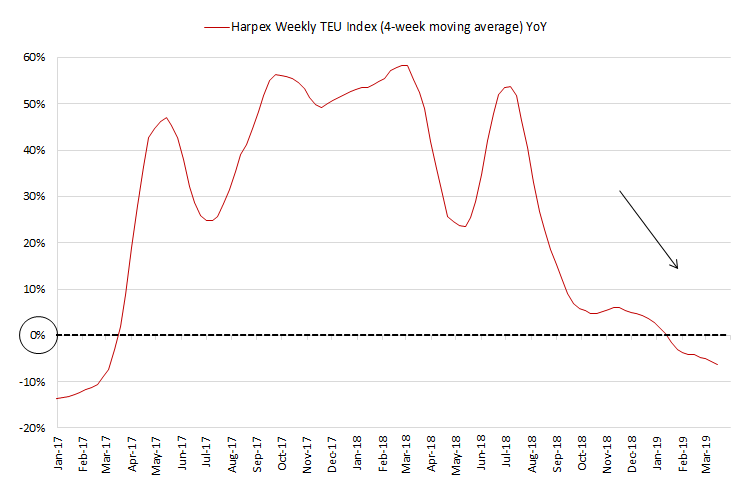

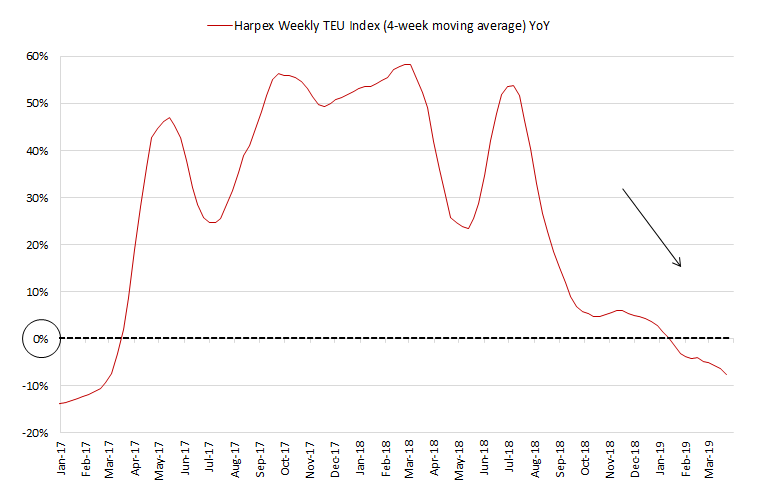

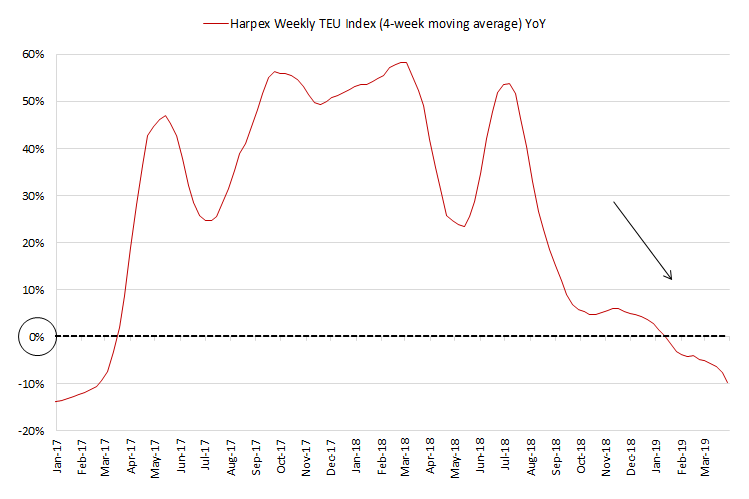

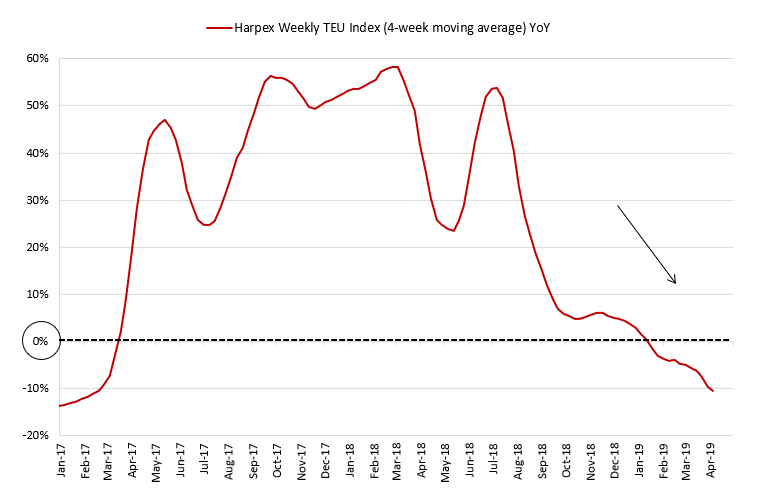

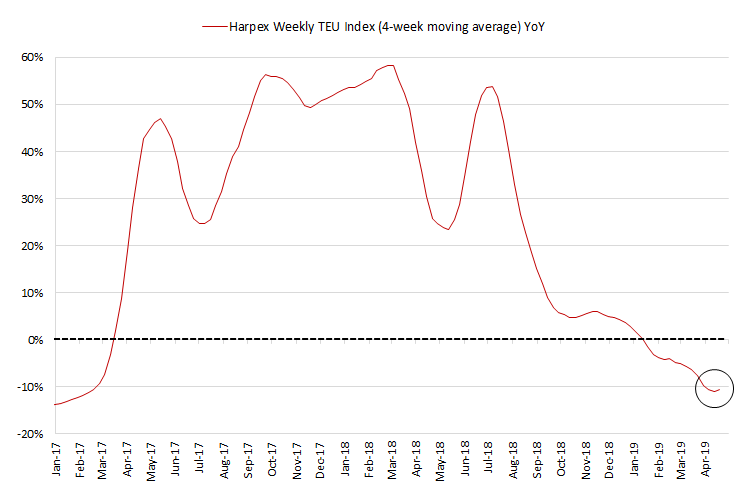

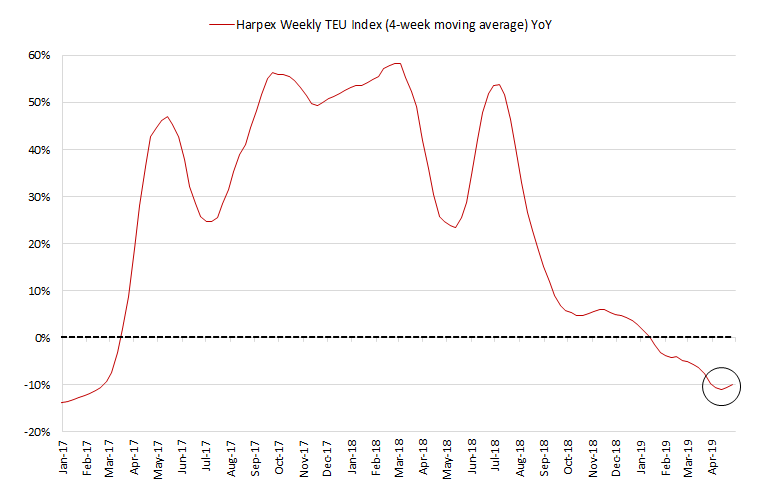

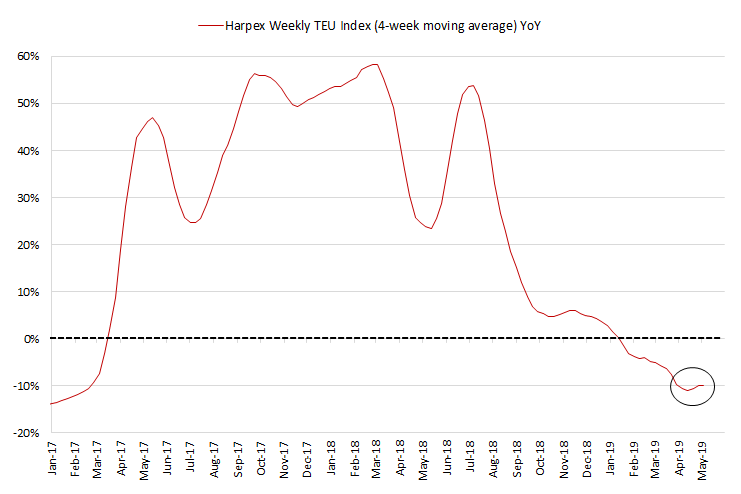

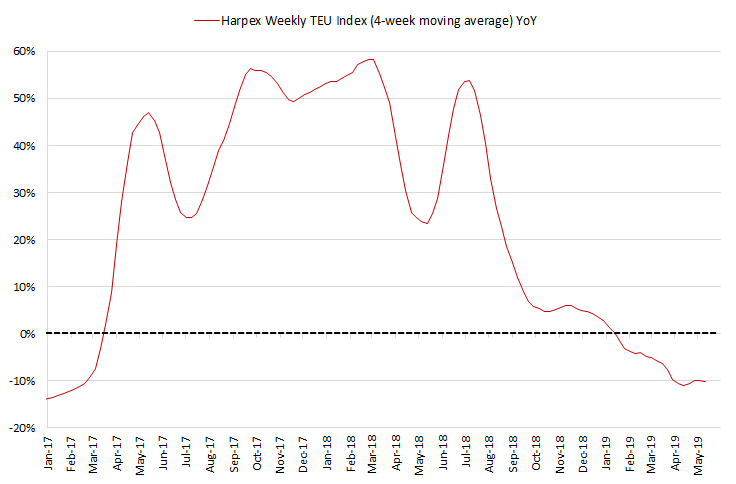

Today, the Harpex Weekly TEU index turned negative YoY for for the first time since March 2017.

*My other proxies also confirm that global trade growth has slowed sharply since Oct. 2018 (bit.ly/2GRnMgo)

*Data link: bit.ly/2AS2D0d

*My other proxies also confirm that global trade growth has slowed sharply since Oct. 2018 (bit.ly/2GRnMgo)

*Data link: bit.ly/2AS2D0d

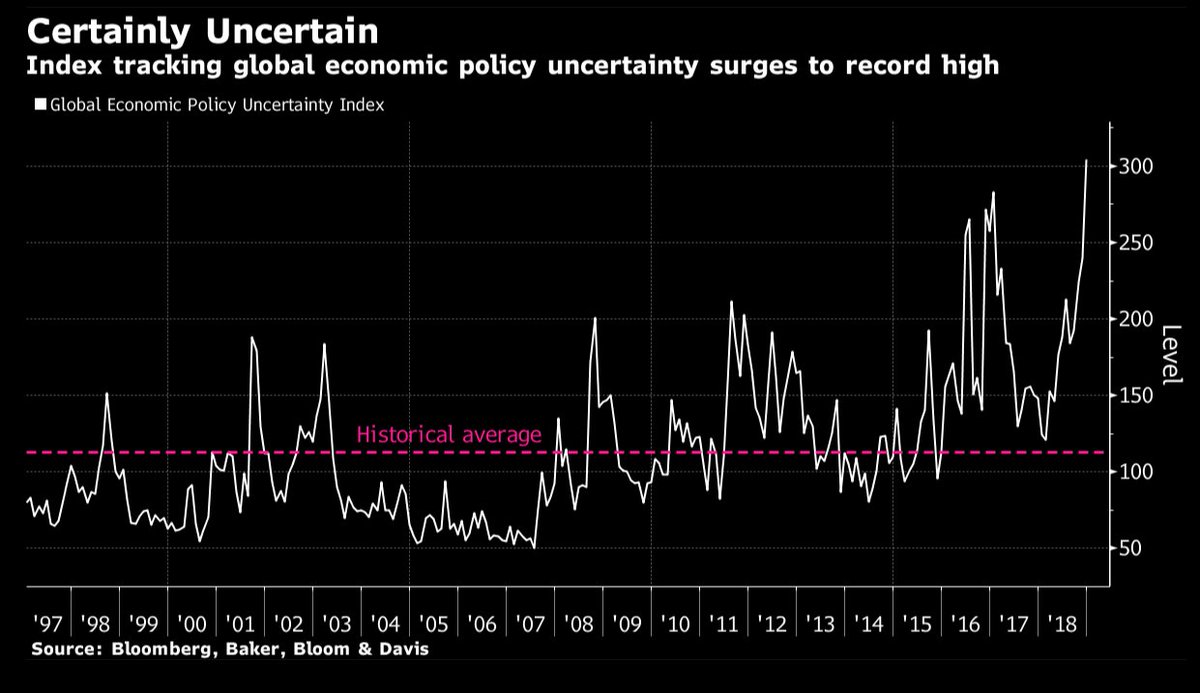

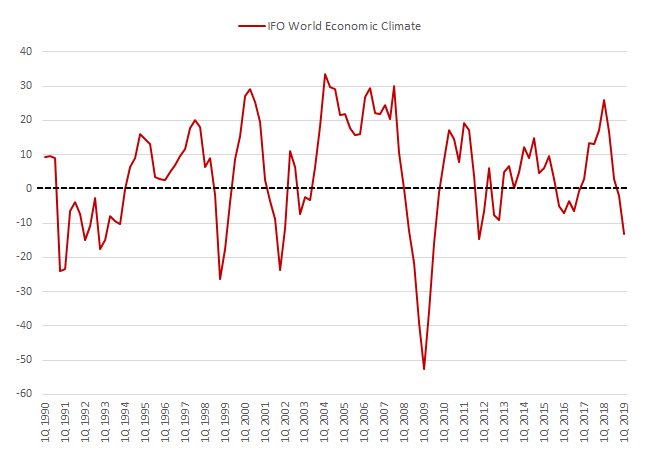

World Economy Wobbles on Eve of #Davos With Politics to Blame - Bloomberg

*Global Policy Uncertainty index reached a record high

*IMF will update its GDP forecasts on Monday.

*Link: bloom.bg/2sC3D3Y

*Global Policy Uncertainty index reached a record high

*IMF will update its GDP forecasts on Monday.

*Link: bloom.bg/2sC3D3Y

#IMF will update its GDP forecasts on Monday:

➡ I expect sharp downgrades for 2019 especially for Eurozone.

➡ As a reminder, IMF chief Lagarde already made a warning in early Dec.

*Link: bloom.bg/2T1rPZ9

➡ I expect sharp downgrades for 2019 especially for Eurozone.

➡ As a reminder, IMF chief Lagarde already made a warning in early Dec.

*Link: bloom.bg/2T1rPZ9

🇨🇳 #CHINA Q4 GDP Y/Y: 6.4% V 6.4%E (it matches the pace seen in 1Q09, lowest since QoQ data were recorded in 1992)

*Overall 2018 GDP Y/Y: 6.6% v 6.6%e (slowest since 1990)

*According to BBG, nominal GDP growth slowed to 8.1% YoY (down from 9.6% YoY in 3Q; weakest since 4Q16)

*Overall 2018 GDP Y/Y: 6.6% v 6.6%e (slowest since 1990)

*According to BBG, nominal GDP growth slowed to 8.1% YoY (down from 9.6% YoY in 3Q; weakest since 4Q16)

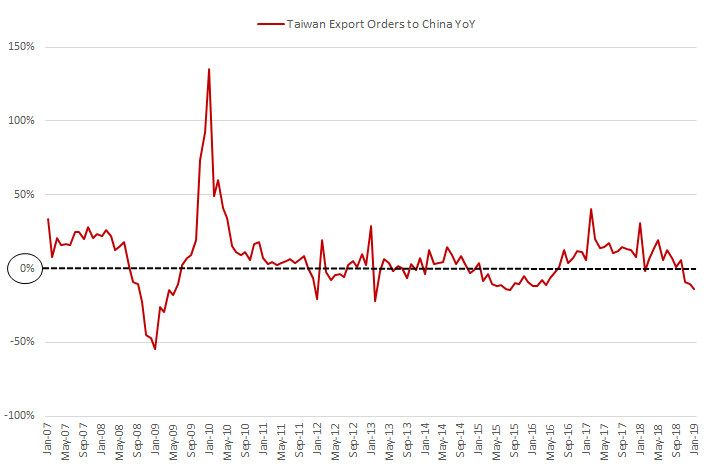

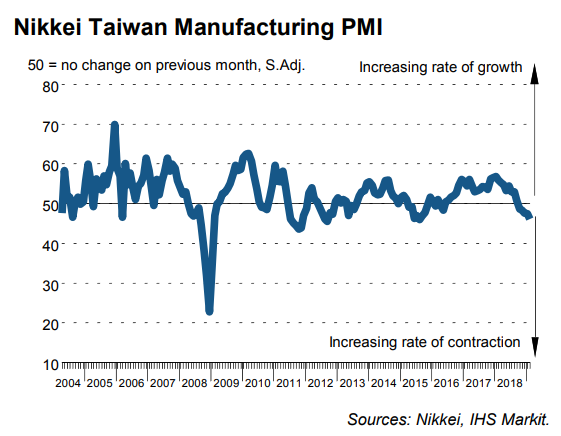

🇹🇼 #Taiwan Dec Export Orders Y/Y: -10.5% v -2.1% prior (largest ⬇ since April 2016)

*Exports to HK and Mainland Y/Y: -10.3% vs -8.9% prior

*Exports to Europe Y/Y: -28.1% vs -5.7% prior

*MOEA SEES JAN. EXPORT ORDERS FALLING 11.8%-14.1% Y/Y ❗

*Link; bit.ly/2AULZgm

*Exports to HK and Mainland Y/Y: -10.3% vs -8.9% prior

*Exports to Europe Y/Y: -28.1% vs -5.7% prior

*MOEA SEES JAN. EXPORT ORDERS FALLING 11.8%-14.1% Y/Y ❗

*Link; bit.ly/2AULZgm

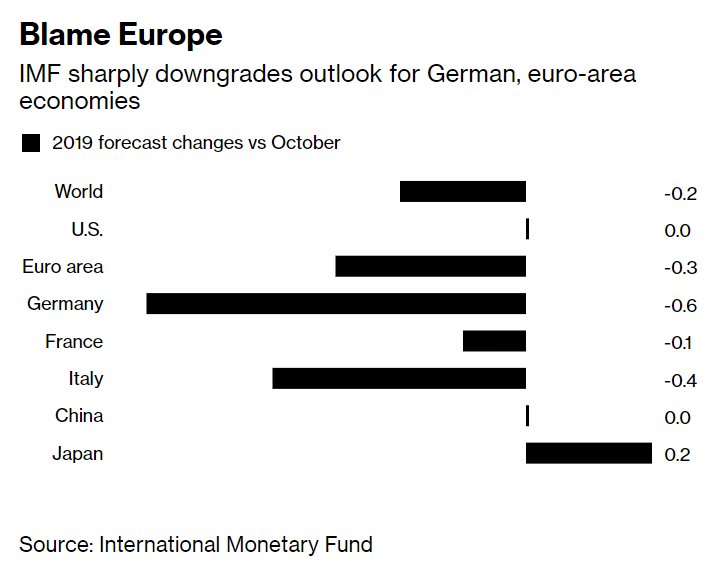

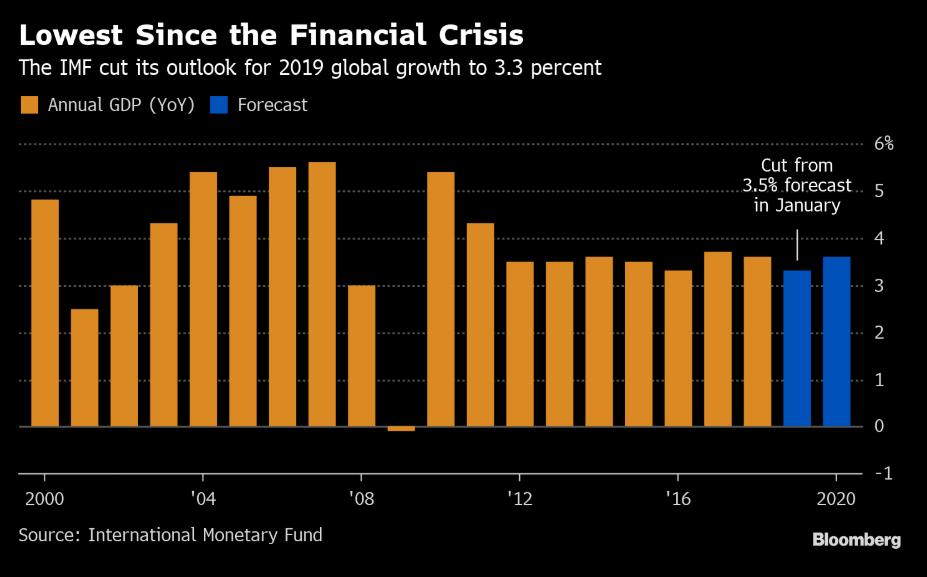

As expected (bit.ly/2FEPbRe), #IMF cut 2019 Wold GDP forecast for second time in three months to 3.5%.

*Link: bloom.bg/2R3yj7W

*Link: bloom.bg/2R3yj7W

PricewaterhouseCoopers released a survey showing 30 percent of business leaders expect the expansion to weaken, about six times the number of a year ago - Bloomberg

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

🇨🇳 Citing Xinhua, Bloomberg reported #China President Xi Jinping stressed the need to maintain political stability in an unusual meeting of top leaders -- a fresh sign the ruling party is growing concerned about the social implications of the slowing.

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

🇨🇳 #China state planner (NDRC) warns economic pressure will hit job market - Reuters

af.reuters.com/article/commod…

af.reuters.com/article/commod…

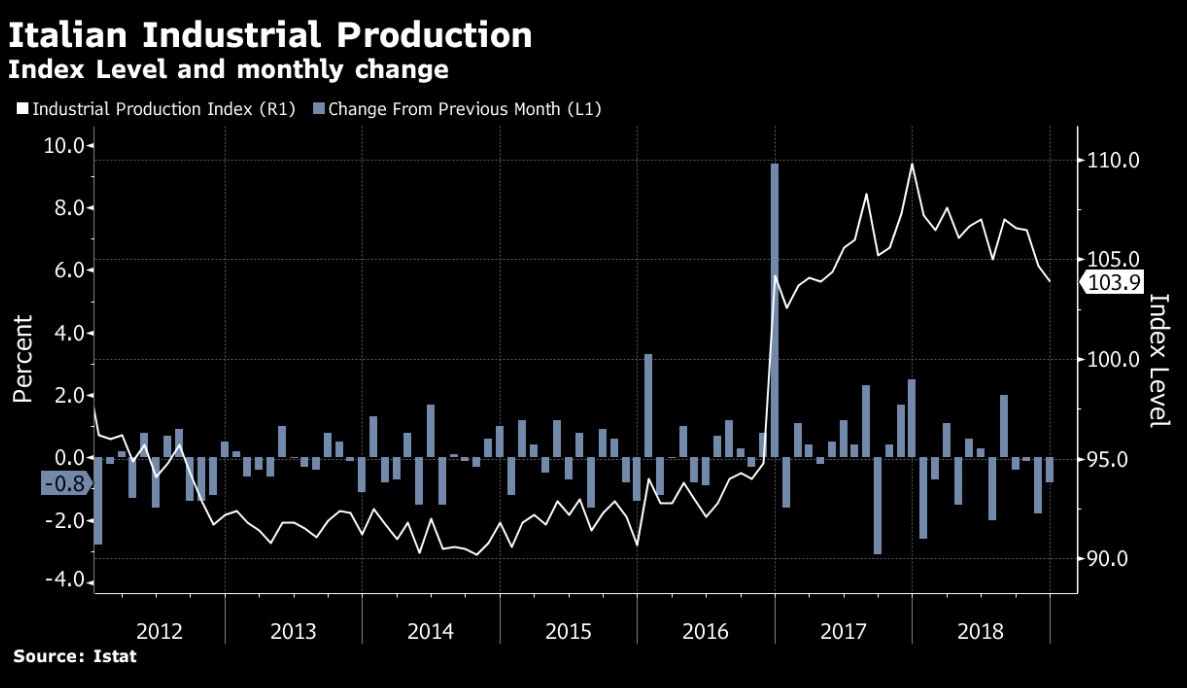

🇮🇹 #Italy | Carige needs 200 million euros of fresh capital: Il Sole 24 Ore citing study - Reuters

reuters.com/article/us-eur…

reuters.com/article/us-eur…

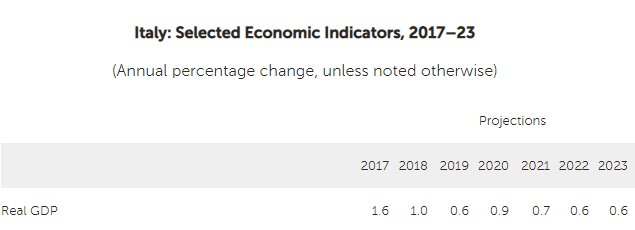

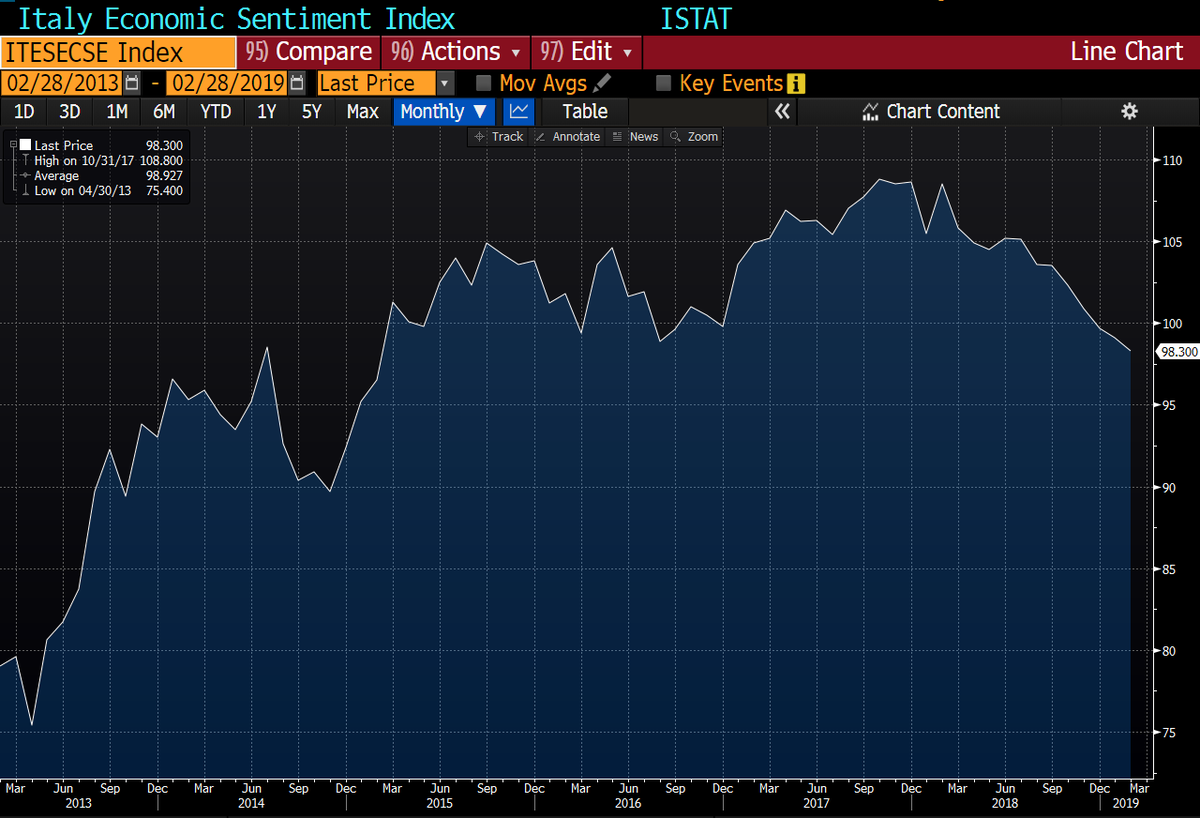

🇮🇹 After the BOI Friday (bit.ly/2T6Io5T), La Repubblica reports that the EU Commission will cut its 2019 growth forecast for #Italy to 0.6% or “slightly” below.

*In Nov. (bit.ly/2RX57Rk, I already warned that forecasts were optimistic.

uk.reuters.com/article/uk-ita…

*In Nov. (bit.ly/2RX57Rk, I already warned that forecasts were optimistic.

uk.reuters.com/article/uk-ita…

🇮🇹 #Italy 2019 GDP | The EU Commission potential downgrade from +1.2% to +0.6% or “slightly” below suggests that 4Q18 GDP would remain negative and therefore the country was in technical recession in 2H18.

➡ First 4Q18 GDP estimate will be released on Jan. 31

➡ First 4Q18 GDP estimate will be released on Jan. 31

🇰🇷 #SouthKorea | Trade data for the first 20 days of Jan. showed:

*a 14.6% YoY ⬇ in total exports (largest ⬇ since September 2016; vs +1.0% in Dec.)

*a 9.5% YoY ⬇ in total imports (largest ⬇ since September 2016; vs +2.2% in Dec.)

*Link: bit.ly/2FNR3X0

*a 14.6% YoY ⬇ in total exports (largest ⬇ since September 2016; vs +1.0% in Dec.)

*a 9.5% YoY ⬇ in total imports (largest ⬇ since September 2016; vs +2.2% in Dec.)

*Link: bit.ly/2FNR3X0

🇰🇷 🇨🇳 #SouthKorea | Trade data for the first 20 days of Jan. showed:

*a 22.5% YoY ⬇ in exports to #China (largest ⬇ since Jan. 2009 vs -14.2% in Dec.)

*a 28.8 YoY ⬇ in semiconductor exports (vs -9.8% in Dec.)

*Link: bit.ly/2FNR3X0

*a 22.5% YoY ⬇ in exports to #China (largest ⬇ since Jan. 2009 vs -14.2% in Dec.)

*a 28.8 YoY ⬇ in semiconductor exports (vs -9.8% in Dec.)

*Link: bit.ly/2FNR3X0

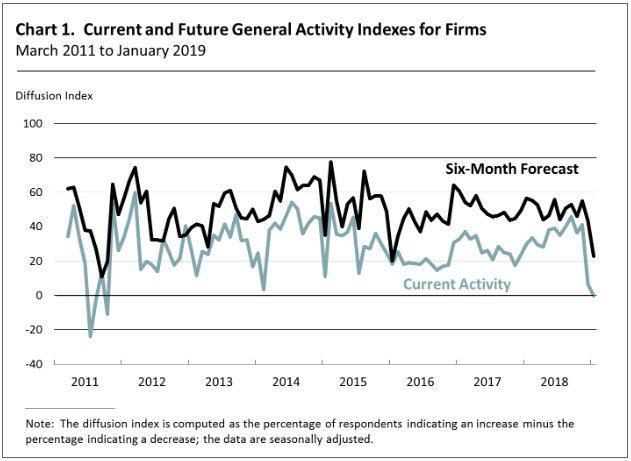

🇺🇸 Philadelphia #Fed Non-manufacturing Business Outlook Survey:

*The diffusion index for current general activity at the firm level fell from a revised reading of 6.4 in December to -0.2 in January (1st negative reading since October 2011)

*Link: bit.ly/2T9KiCQ

*The diffusion index for current general activity at the firm level fell from a revised reading of 6.4 in December to -0.2 in January (1st negative reading since October 2011)

*Link: bit.ly/2T9KiCQ

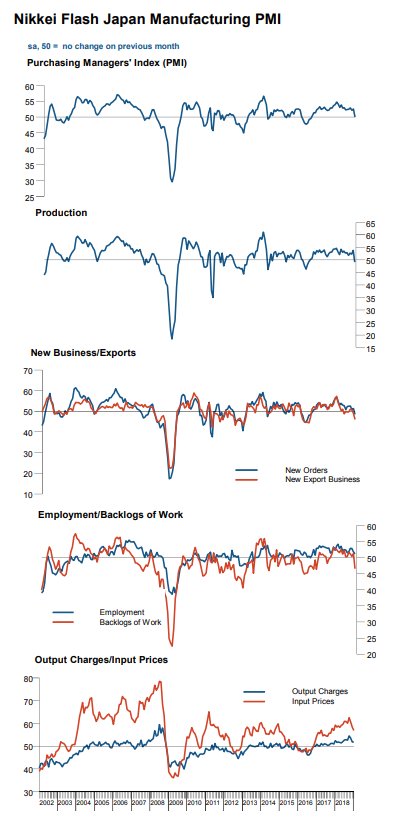

🇯🇵 #JAPAN JAN PRELIM MANUFACTURING PMI: 50.0 V 52.6 PRIOR (weakest reading since August 2016)

*Production ⬇ for first time since July 2016 (49.2 vs 54.0 prior)

*New export orders ⬇ at fastest pace since July 2016 ❗

*Link: bit.ly/2FKxsb1

*Production ⬇ for first time since July 2016 (49.2 vs 54.0 prior)

*New export orders ⬇ at fastest pace since July 2016 ❗

*Link: bit.ly/2FKxsb1

🇩🇪 #GERMANY JAN PRELIMINARY MANUFACTURING PMI: 49.9 V 51.5E (1st contraction in 49 months)

*Services PMI: 53.1 v 52.1e (66th month of expansion)

*Composite PMI: 52.1 v 51.9e (2-month high)

*New export orders ⬇ at an accelerated rate ❗

*Link: bit.ly/2CHNNJw

*Services PMI: 53.1 v 52.1e (66th month of expansion)

*Composite PMI: 52.1 v 51.9e (2-month high)

*New export orders ⬇ at an accelerated rate ❗

*Link: bit.ly/2CHNNJw

🇪🇺 EUROZONE JAN PRELIMINARY MANUFACTURING PMI: 50.5 V 51.4E (67-month low)

*Services PMI: 50.8 v 51.5e (65-month low)

*Composite PMI: 50.7 v 51.4e (66-month low)

*Link: bit.ly/2RLFVBl

*Services PMI: 50.8 v 51.5e (65-month low)

*Composite PMI: 50.7 v 51.4e (66-month low)

*Link: bit.ly/2RLFVBl