Macro investment research at https://t.co/hQqAza8GGP

Our total return index is at https://t.co/vta9eqevnU

The ETF WTBN tracks our Index.

biancoresearch.eth

122 subscribed

122 subscribed

122 subscribed

122 subscribed

2/6

2/6

2/6

2/6

2/8

2/8

2/5

2/5

2/4

2/4 2/4

2/4

2/4

2/4

2/9

2/9

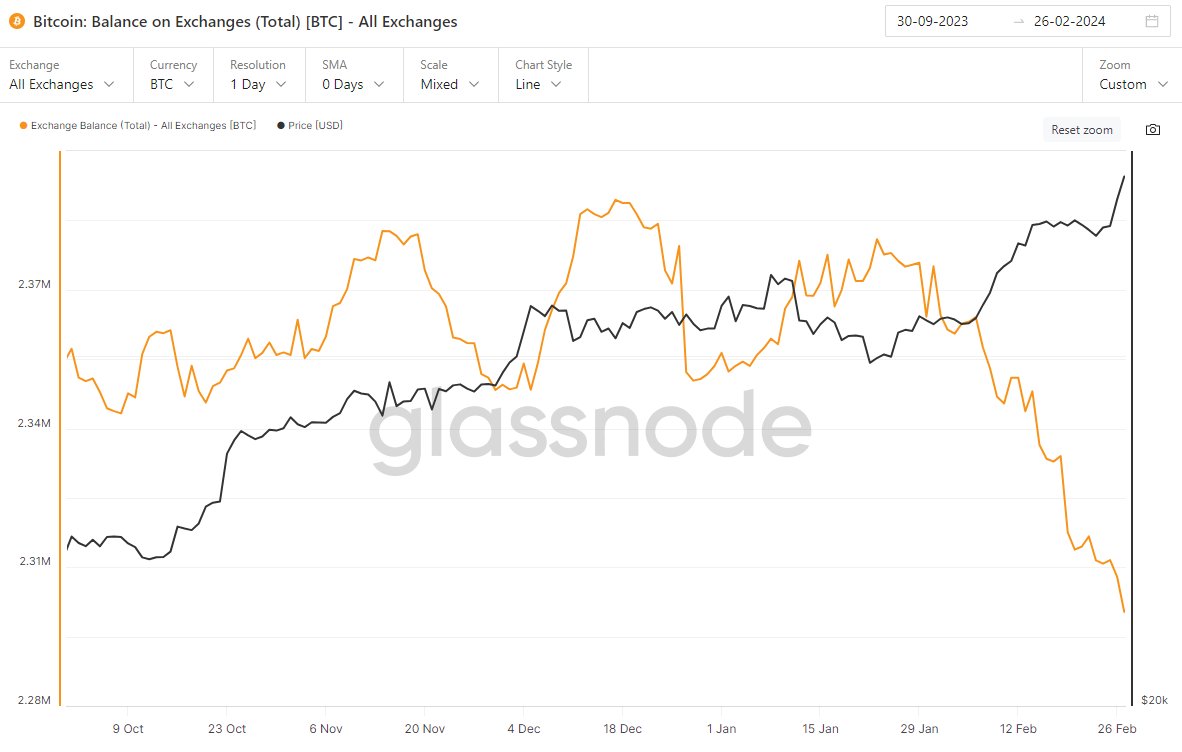

The black line is BTC's price (right scale)

The black line is BTC's price (right scale)

2/4

2/4

2/6

2/6

2/7

2/7