Discover and read the best of Twitter Threads about #coreCPI

Most recents (14)

Today’s #CPI report for May showed another very firm depiction of where #inflation currently resides in the U.S., with #coreCPI (excluding volatile food and energy components) printing at 0.44% month-over-month and 5.33% year-over-year.

Meanwhile, #headlineCPI data printed 0.12% month-over-month and came in just above 4% year-over-year, with declines in #energy components and some food prices being offset by gains in #shelter and used cars and trucks.

Overall, headline #inflation does appear to be moderating at a faster pace and we believe that the trend in inflation (despite the firmness of core measures in today’s report) is broadly heading in the right direction, relative to the @federalreserve’s inflation target.

Today’s #CPI report continues to depict #inflation that is just too high for most people’s good, especially the @federalreserve’s.

In fact, the report showed that #inflation remains remarkably sticky, which doesn’t correspond to virtually any practical thinker’s timeline of when it might be expected to start to come down further.

These elevated levels of inflation continue to be remarkably high relative to the many months with which the #economy has now operated with persistently higher #InterestRates.

A week ago, after hearing #ChairPowell’s testimony before Congress, all eyes were set to be on today’s #inflation data, which presumably would help market participants better understand the #FOMC’s policy reaction at its March 22nd meeting.

What a difference a week makes these days! Of course, all eyes are still on today’s data, but now there are many other things we need to consider (such as #FinancialStability concerns), when judging the reaction function of the @federalreserve.

As we have long contended, #markets tend to be fairly myopic and lacking in patience, so having to focus on more than one news item at a time causes tremendous #uncertainty and thus greater market #volatility.

🐻♉️↗️↘️↔️⚠️🚩🔺🔻c 💰

Macro Review 2/26/23

🧵 1/8

If the #macro picture has been unclear, it has just come clearly into focus.

I am going to keep it simple this week -

crash risk is rising ⚠️🚩

Let’s dig into the market 🧮!

Macro Review 2/26/23

🧵 1/8

If the #macro picture has been unclear, it has just come clearly into focus.

I am going to keep it simple this week -

crash risk is rising ⚠️🚩

Let’s dig into the market 🧮!

2a/8

It’s all about the $USD 🎳

On 2/10, we got a confirmed buy signal in the USD along with sell signals in $SPX and $TLT

It’s all about the $USD 🎳

On 2/10, we got a confirmed buy signal in the USD along with sell signals in $SPX and $TLT

In the big picture, today’s #CPI data displays continued slow progress toward a lower y-o-y rate of #inflation, having come down from a cycle peak of 8.9% in June 2022 to the 6.4% reading today, at the headline level, which is the lowest 12-month inflation gain since Oct 2021.

That is clearly encouraging, and in a lot better place than we had become used to in the Fall, which was at the center of the disappointment for the @federalreserve. However, like bridges during periods of traffic, progress can come with some slowing along the way.

For three straight months we saw essentially flat readings for #CoreInflation (ex-shelter), for an average level of 0.08%, yet this month we saw it move up to 0.2%.

🐻♉️↗️↘️↔️⚠️🚩🔺🔻🧮 💰

Macro Review 🧵

01/15/2023

1/11

Core #CPI running at +3.1% SAAR confirmed #Goldilocks for Q422 and catalyzed a 🚀 in equities, metals, and hydrocarbons

#Core CPI - 3-month SAAR

Dec - 3.1%

Nov - 4.2%

Oct - 5.7%

Chart: #CoreCPI 5.7% 🔻

Macro Review 🧵

01/15/2023

1/11

Core #CPI running at +3.1% SAAR confirmed #Goldilocks for Q422 and catalyzed a 🚀 in equities, metals, and hydrocarbons

#Core CPI - 3-month SAAR

Dec - 3.1%

Nov - 4.2%

Oct - 5.7%

Chart: #CoreCPI 5.7% 🔻

1a/11

Despite all the recession talk - including my own, the @AtlantaFed #NowCast is projecting Q4 growth of +4.1%, an acceleration.

Growth 🔺 + Inflation 🔻 = #Quad1 #Goldilocks

Chart:

Despite all the recession talk - including my own, the @AtlantaFed #NowCast is projecting Q4 growth of +4.1%, an acceleration.

Growth 🔺 + Inflation 🔻 = #Quad1 #Goldilocks

Chart:

2/11

While #Quad1 #Goldilocks may be good for risk assets, it’s decidedly poor for the $USD, which continued ↘️ and took out the 50% retracement level of 102.12

Chart: $USD -1.64% (w) -9.94% 3M = T = Trend

While #Quad1 #Goldilocks may be good for risk assets, it’s decidedly poor for the $USD, which continued ↘️ and took out the 50% retracement level of 102.12

Chart: $USD -1.64% (w) -9.94% 3M = T = Trend

The November #CPI report is notable in part due to the fact that it displays the second consecutive month of more moderate price pressures, providing some signal that the underlying trend of #inflation is decelerating.

Turning to the data, #coreCPI (excluding volatile food and #energy components) came in at 0.2% month-over-month and rose 6.0% year-over-year.

Meanwhile, #headlineCPI data printed 0.1% month-over-month and came in at 7.1% year-over-year, with declines in #UsedCars, medical care and airline fares contributing to this result. Still, both #shelter costs and the food index rose significantly.

The headline #inflation data today moderated a bit on the back of falling #gasoline prices, but it’s still running at a worryingly high rate.

Over time, we think the slowdown in #economic growth, the continuation of the @federalreserve’s assertive #HikingCycle and the possibility of resolution with several persistent supply chain issues should influence broad #inflation lower.

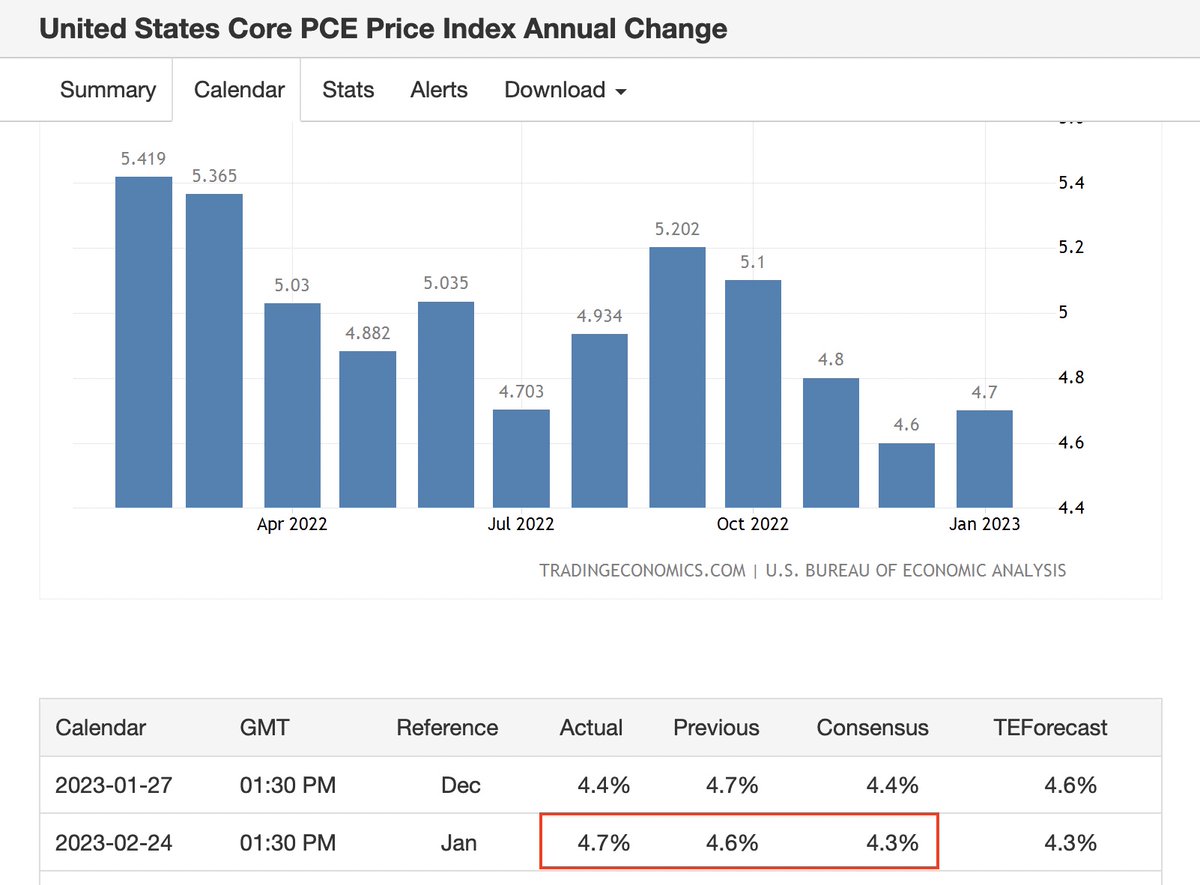

Still, while #CorePCE inflation (the #Fed’s favored measure) is likely to moderate in the coming months, it’ll still remain well-above the Fed’s 2% #inflation target.

Core #CPI (excluding those volatile #food and #energy components) came in at 0.6% month-over-month and rose 6.0% year-over-year.

Meanwhile, headline #CPI data printed at a very strong 1.0% month-over-month and came in at 8.6% year-over-year, spiking higher on #shelter, #gas and food costs.

These persistently outsized gains in #inflation are clearly having an impact on business and #ConsumerConfidence. Also, the #Fed’s favored measure of inflation, core #PCE, increased 0.34% in April, bringing the year-over-year figure for the measure to 4.9%, as of that month.

With respect to the data, #coreCPI (excluding volatile food and #energy components) came in at 0.6% month-over-month and at a high 6% year-over-year.

Meanwhile, headline #CPI data printed at a strong 0.6% month-over-month and came in at 7.5% year-over-year, the greatest increase over a 12-month period since February 1982.

Additionally, the @federalreserve’s favored measure of #inflation, #corePCE, increased 0.5% in December, bringing the year-over-year figure for the measure to 4.9%, as of that month.

Today’s #inflation report continued to reinforce the theme that gaudy #price gains are not standing in the way of demand.

It is a very rare time in history, in fact, most people operating in #markets haven’t seen this sort of demand outstripping supply in the real #economy in their careers, with some areas seemingly depicting a dynamic suggesting that “price is no object.”

Clearly, #inflation has been escalating for a number of months due to #shortages of supply in areas such as #housing, #commodities, semiconductors, new and used cars, etc., and those supply shortages are mostly still in place today.

With respect to today’s #inflation data, core #CPI (excluding volatile food and energy components) came in at 0.24% month-over-month and 4.04% year-over-year and was driven higher by strong increases in the #rent components, which have a tendency to be persistent.

Further, headline #CPI data printed at a solid 0.41% month-over-month and came in at 5.38% year-over-year.

Today’s robust #inflation data surprised in its strength and will likely persist in the short-run, and in some areas the intermediate-term, although we think that long-term the @federalreserve is largely correct in identifying real #economy price gains as mostly #transitory.

Much of today’s #inflation is due to reopening factors and supply constraints, but as #SupplyChains normalize from Covid-related shocks and #inventories rebuild, we expect much of the recent inflation will be transitory, with some stickiness in pricing pressure longer-run.

That may be especially the case where #inventory levels are harder to build up quickly and continued #demand from higher levels of #growth persist for at least the next year, or so.

CPI@ 4.59% in Dec Vs 6.93% in Nov'20;It is for first time in current fiscal that #CPI,below 6%

In Jan2021,CPI may be lower than RBI forecast of 5.8%,which is good news

#CoreCPI in Dec,5.65% Vs 5.84% MoM

Money market rates,lower than #ReverseRepo,implying low rates here to stay

In Jan2021,CPI may be lower than RBI forecast of 5.8%,which is good news

#CoreCPI in Dec,5.65% Vs 5.84% MoM

Money market rates,lower than #ReverseRepo,implying low rates here to stay

#FoodInflation 3.41% in Dec,Vs 9.43% in Nov

Vegetable Inflation@ -10.41% Vs 15.63%💪

Fuel&Light Inflation@ 2.99% Vs 1.90%

Housing Inflation@3.21% Vs 3.19%

Clothing&Footwear Inflation@ 3.49% Vs 3.30%

Cereal Inflation@0.98% Vs 2.32% (MoM)

Pulses Inflation@15.98% Vs 17.91%

Vegetable Inflation@ -10.41% Vs 15.63%💪

Fuel&Light Inflation@ 2.99% Vs 1.90%

Housing Inflation@3.21% Vs 3.19%

Clothing&Footwear Inflation@ 3.49% Vs 3.30%

Cereal Inflation@0.98% Vs 2.32% (MoM)

Pulses Inflation@15.98% Vs 17.91%