,

18 tweets,

6 min read

Read on Twitter

We know that financial crises come from innovations of short-term bank/bank-like debt that move outside of/more quickly than the regulatory regime. So, where might the next one come from? A case for the answer being right there in the name: #FinTech. An ongoing thread...

Many firms providing digital payment services have large cash balances attributable to their customers who have left money “in” the app for ease of use. This cash is often deposited in banks with interest accruing to the firm...

...This muddies the picture of short-term funding for bank regulators and provides an extra link in the chain that can leave the financial system vulnerable to runs. There are several possible mechanisms...

#FinTech --> #FinCrisis Mechanism #1: These apps are essentially acting as unregulated money market mutual funds. This carries the prospect of mass migration from uninsured deposits to insured ones during times of stress. Given post-crisis regs on FDIC/Treasury intervention (1/x)

...this is particularly a risk in the U.S. For example, @PayPal (inclusive of Venmo) has $22 billion in short-term funds due to customers. (2/x)

Per PayPal's 10-K, this money is "maintained in

interest and non-interest bearing bank deposits, time deposits, U.S. and foreign

government and agency securities, and corporate debt securities." This is maturity transformation in its purest form and vulnerable to runs. (3/x)

interest and non-interest bearing bank deposits, time deposits, U.S. and foreign

government and agency securities, and corporate debt securities." This is maturity transformation in its purest form and vulnerable to runs. (3/x)

This same risk is likely to exist in Facebook's latest "innovation":

#FinTech --> #FinCrisis Mechanism #2: Tech firms often rely on network effects--e.g. the large iPhone user base--to drive growth in their products. In this sense, there may be a lower hurdle to a coordinated bank run; the network itself provides the coordination mechanism. (1/x)

With the proliferation of "open banking" platforms, this risk is all the more potent as the platforms' value propositions rely on their intermediation. These firms have extra incentive to alert their users at the first sign of trouble. (2/x) h/t @TomHale_: ftalphaville.ft.com/2019/03/29/155…

Imagine an alert sent to all iPhone users or all users of a particular app urging them to transfer their balances away from bank/firm/fund X. Highly disruptive to allocations even if no effect on overall funding available. (3/x)

This risk is amplified in the case of apps that are inclusive of social and financial aspects—such as Venmo, WeChat in China, or other apps that include (encrypted) messaging functions (such as Facebook's new payments initiative). (4/x) @izakaminska

We saw this dynamic on full display during the Arab Spring ; no doubt a run on the financial system could be similarly coordinated. The threat from this transmission channel is only increasing in the age of fake news proliferation. (5/x)

The process of influencing social outcomes via falsification of online narratives (like we’ve seen in the U.S., India , and elsewhere) could easily be repurposed to instigate a digital run on a FinTech firm or group of firms... (6/x)

...either by corporate competitors or geopolitical rivals—and by extension, a run on the U.S. financial system. (7/7)

#FinTech --> #FinCrisis Mechanism #3: In the case of mobile payment/commerce apps, nominal customer account transaction balances—which, if held at a bank would be well-below deposit insurance caps—would now be aggregated at the tech firm level and deposited by the firm. (1/x)

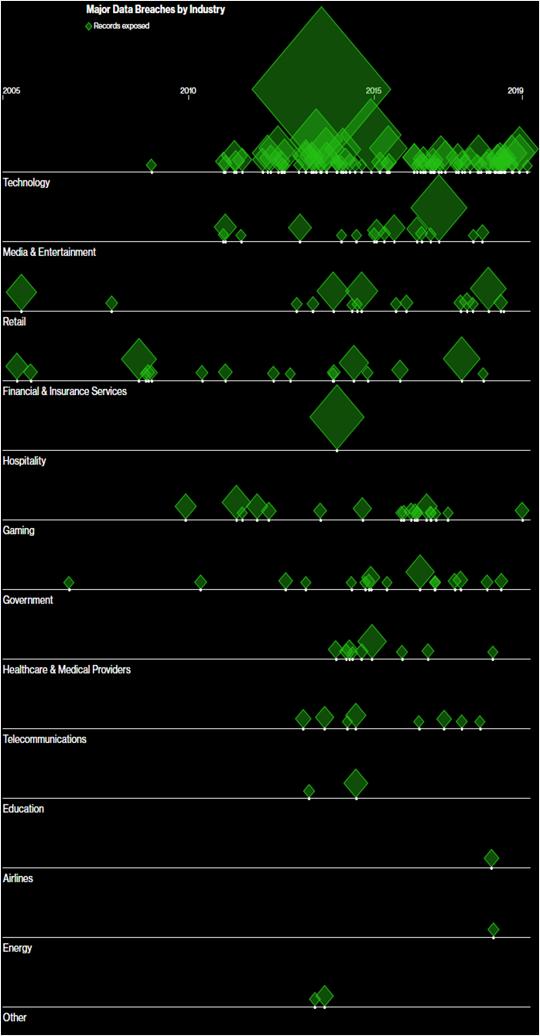

This opens financial system’s short-term funding to vulnerabilities in the tech sector. For instance, a data breach at a tech firm could cause customers to pull their funds, leading the tech firm to quickly draw down its short-term lending to the financial sector. (2/x)

The tech sector’s history is not flattering on this front... Via @business (3/x):

If the run on FinTech firms was substantial enough, there is also the risk of off-balance-sheet commitments such as lines of credit exacerbating the run on the financial system. This was the case during the last financial crisis, most notably w/ GE’s placed lines of credit. (4/4)